Armed Forces Officer Pension Calculator

Estimate an officer's armed forces pension and lump sum across AFPS 75, 05 and 15, based on rank and final pensionable pay.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Officer estimate is worked out

Your officer pension follows the Armed Forces Pension Scheme that applied while you served. Pick the scheme that matches when you joined, most careers touch more than one.

AFPS 75 is a final-salary scheme. Your pension is a share of representative pay for your rank, building to a maximum of 48.5% over a full career, 34 years for officers, 37 for other ranks, with an automatic tax-free lump sum of three times the annual pension.

AFPS 05 is also final-salary, building 1/70th of your final pensionable pay for each year served, up to about 57% of pay. It pays an automatic tax-free lump sum of three times your pension and can include an Early Departure Payment if you leave early with enough service.

AFPS 15 is a Career Average Revalued Earnings (CARE) scheme. It adds 1/47th of your current pensionable pay each year, revalued for inflation, rather than using a final salary. There is no automatic lump sum, so you can commute up to 25% of your pension for tax-free cash at a fixed rate of £12 per £1 of yearly pension given up.

How an officer pension builds across the three schemes

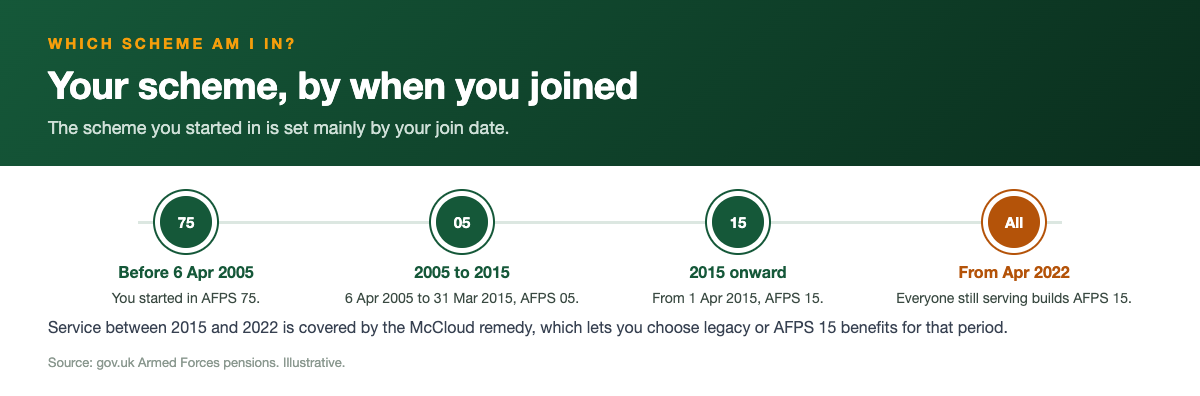

An officer's armed forces pension is not one pot built one way. It depends on when you were commissioned and which scheme you were in, because the rules changed twice. If you joined between 1 April 1975 and 5 April 2005 you started on AFPS 75. If you were commissioned between 6 April 2005 and 31 March 2015 you started on AFPS 05. Anyone joining from 1 April 2015 went straight onto AFPS 15, and from 1 April 2022 every serving officer builds AFPS 15 regardless of when they joined.

The three schemes use very different maths. AFPS 75 and AFPS 05 are final-salary schemes, so your pension is shaped by your pay near the end of service and how long you served. AFPS 15 is a Career Average Revalued Earnings (CARE) scheme, which banks a slice of pay every single year and revalues it for inflation, so the whole career counts rather than just the final years. Many serving officers now hold a mix: legacy benefits from before 2022 sitting alongside a growing AFPS 15 pot.

This calculator estimates each scheme separately so you can see how rank, pay and length of service feed the result. It is a planning tool, not an official forecast. Only Veterans UK can give you a binding figure, using form 12 if you are still serving or form 14 for a preserved pension. Treat every number here as an estimate to sense-check your thinking, not a promise of what will land in your account.

Rank, representative pay and the officer accrual point

On AFPS 75 the pension for officers up to and including OF-6 (so up to Brigadier or equivalent) is not based on the exact salary you happened to be on. It is based on the representative rate of pay for your final pensionable rank and your length of reckonable service. Two officers who retire in the same rank with the same service normally receive the same pension, whatever small pay differences sat between them. Only officers at OF-7 and above (Major General and above, or equivalent) have AFPS 75 worked on their final pensionable earnings instead.

This matters for how you read the calculator. We do not hold the MOD's rank-by-rank representative pay tables, so the tool uses the pay you enter as a proxy for that representative rate and says so on screen. To get the closest AFPS 75 estimate, enter the representative pay for the rank you expect to hold at the end, not necessarily your current taxable salary. If you are not sure of the representative figure for your rank, your unit HR or pay staff can point you to the current pay tables.

Accrual on AFPS 75 starts later for officers than for other ranks. Reckonable service for an officer is counted from age 21, whereas other ranks count from age 18. That three-year difference is one reason an officer's AFPS 75 maximum is reached after 34 years of reckonable service rather than the 37 years used for other ranks. AFPS 05 and AFPS 15 do not use representative pay at all: AFPS 05 uses your actual final pensionable pay, and AFPS 15 uses the pensionable earnings banked each year.

The 34-year full career on AFPS 75

On AFPS 75 an officer's pension builds towards a maximum of 48.5% of representative pay over a full career of 34 years of reckonable service. In this calculator the build-up is treated as even across those years, so each year adds roughly 1.426% of pay (48.5% divided by 34). At 17 years you would be around the halfway mark, near 24% of pay, and at the full 34 years you reach the 48.5% ceiling. Serving beyond 34 years does not push an officer's AFPS 75 pension above 48.5%.

AFPS 75 also pays an automatic tax-free lump sum of three times the annual pension. So an officer at the 48.5% maximum receives a pension worth just under half of representative pay, plus a one-off lump sum equal to three years of that pension, paid free of income tax. There is nothing to claim or commute to get this lump sum on AFPS 75; it comes automatically with the pension.

AFPS 75 has its own early-payment route called the Immediate Pension. For an officer this is payable on leaving Regular Service after 16 years of service from age 21, provided at least 5 years were served as an officer. That gives a pension and lump sum in hand at the point of leaving rather than waiting to pension age. If you leave without reaching the Immediate Pension point, your AFPS 75 benefits are preserved and paid from 60 for service before 6 April 2006 or from 65 for service after that. AFPS 75 has no Early Departure Payment; the Immediate Pension is its equivalent.

A worked example for an officer (illustrative)

Here is an illustrative example using only the figures this site is built on. Take an officer with representative pay of 70,000 pounds and a full 34 years of reckonable service on AFPS 75. The pension is 48.5% of 70,000, which is 33,950 pounds a year. The automatic tax-free lump sum is three times that, so 101,850 pounds. This is a worked illustration to show the method, not a quote for any individual, and your representative pay rate will differ.

Now compare the same officer on AFPS 05 with 34 years of service and final pensionable pay of 70,000 pounds. AFPS 05 accrues 1/70th of final pay per year, so 34 divided by 70 gives a fraction of about 0.486, producing a pension of roughly 34,000 pounds a year, again with an automatic lump sum of three times the pension. AFPS 05 keeps building beyond this towards its own ceiling of 57% of final pay, reached at 40 years, so a longer-serving officer on AFPS 05 can end up with a larger final-salary pension than on AFPS 75.

On AFPS 15 the same officer with 34 years and current pensionable pay of 70,000 pounds banks roughly 1/47th of pay each year. As a simplified estimate that is 70,000 multiplied by 34 and divided by 47, giving about 50,600 pounds a year. AFPS 15 pays no automatic lump sum, so to get tax-free cash you commute pension at a fixed 12 pounds of lump sum for every 1 pound of annual pension given up, up to 25% of your pension. These three numbers are not added together for one person; they show how the same career produces different shaped results under each scheme.

How late promotion changes the picture

For an officer on AFPS 75 or AFPS 05, a promotion late in your career can have an outsized effect, because both are final-salary schemes. On AFPS 75 the pension is anchored to the representative pay of your final pensionable rank, so moving up a rank shortly before you leave lifts the pay rate that the whole 48.5% calculation is applied to. On AFPS 05 the pension is a fraction of your final pensionable pay, so a late pay rise raises the base figure that every year of the 1/70th accrual is measured against. In both cases your years of service do not change, but the pay they are multiplied by does.

AFPS 15 behaves very differently. Because it is a CARE scheme that banks 1/47th of each year's actual pensionable earnings, a late promotion only improves the years you serve at the higher rate. It does not retrospectively lift the slices you already banked at lower ranks, although every banked slice is revalued for inflation while you serve. So a late promotion is worth most on the legacy final-salary schemes and worth less, though still positive, on AFPS 15.

This is one reason officers with mixed service should not assume their whole pension behaves the same way. Legacy benefits earned before the 2022 move to AFPS 15 are linked to your final pay or rank at the point you actually leave, not frozen at the 2015 or 2022 transition. A promotion in your last posting can therefore still lift the legacy slice of your pension even though you stopped actively building it years earlier.

Tax treatment of an officer's pension and lump sum

The automatic lump sums on AFPS 75 and AFPS 05, each three times the annual pension, are paid free of income tax. The tax-free lump sum you create on AFPS 15 by commuting pension at the 12:1 rate is also tax-free, within the HMRC limit that caps the lump sum at 25% of the overall value of your pension benefits. The Early Departure Payment lump sum, where it applies, is tax-free too.

The annual pension itself is taxable income. Once it is in payment it is taxed like any other pension under PAYE, and it counts towards your total income for the year alongside any salary, second career earnings or the State Pension. An officer's pension can be large enough to use up a meaningful part of your personal allowance, so it is worth thinking about how it stacks with other income rather than looking at it in isolation.

Pensions in payment and preserved pensions are uprated each year in line with CPI to protect their value against inflation. The increase applied from April 2026 is 3.8%. On AFPS 75 the pension is held flat until age 55 and then increased, with all the inflation since you left applied at that point, which is a quirk officers leaving young should plan around. This site does not give regulated financial or tax advice; for your own position speak to a qualified adviser.

How to check your own figure

Start by being honest about which scheme or schemes you are in. Note the date you were commissioned, whether you had transitional protection, and whether any of your service falls in the McCloud remedy period of 1 April 2015 to 31 March 2022. If it does, you will receive a Remediable Service Statement that lets you choose legacy (AFPS 75 or AFPS 05) or AFPS 15 benefits for that window, and that choice changes the numbers.

Then gather the right pay figure for each scheme. For AFPS 75 use the representative pay for the rank you expect to finish in. For AFPS 05 use your final pensionable pay. For AFPS 15 use your current pensionable pay, which works as a sound proxy because each past year is revalued in line with earnings while you serve. Enter your years of reckonable or qualifying service and your expected leaving age so the tool can test whether early-payment routes apply.

Finally, get the official numbers. A forecast from Veterans UK is the only figure that carries weight: request form 12 while you are still serving or form 14 once you hold a preserved pension. Use this calculator to understand roughly what you are entitled to and to ask better questions, then confirm the detail with Veterans UK and, if the decision is significant, a regulated financial adviser. This is an independent education site and is not affiliated with the MOD, Veterans UK or JPAC.

Common mistakes officers make

The most common error is assuming a single percentage applies to your whole career. An officer who served across the 2015 or 2022 transitions has legacy benefits and an AFPS 15 pot built on different rules, and lumping them together gives a misleading total. Estimate each scheme on its own terms and only then think about the combined picture.

A second mistake is entering the wrong pay figure. People often type their gross taxable salary into the AFPS 75 box when the scheme actually uses representative pay for the rank for officers up to OF-6. Others enter a career-average guess into AFPS 15 when the tool is designed to take current pensionable pay. Using the wrong input for the scheme can throw the estimate out by thousands.

A third trap is ignoring eligibility conditions for the early-payment routes. The AFPS 75 Immediate Pension for officers needs 16 years from age 21 with at least 5 years as an officer; EDP 05 needs broadly 18 years and age 40; EDP 15 needs broadly 20 years and age 40. Below those points you hold a preserved pension paid later, not an immediate income, so check the conditions before you plan around early money.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Not sure which scheme you're in?

Find out whether you're on AFPS 75, 05 or 15 and how each builds up.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.