Reserves & FTRS Pension Calculator

Work out the pension and EDP built up from Reserve Forces or FTRS service under AFPS 15.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 15 (20/40 early leaver)

How this is worked out

AFPS 15 is CARE: 1/47th of pay each year, revalued by earnings while you serve. Enter your current pensionable pay. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Reserves estimate is worked out

Your Reserves pension follows the Armed Forces Pension Scheme that applied while you served. Pick the scheme that matches when you joined, most careers touch more than one.

AFPS 75 is a final-salary scheme. Your pension is a share of representative pay for your rank, building to a maximum of 48.5% over a full career, 34 years for officers, 37 for other ranks, with an automatic tax-free lump sum of three times the annual pension.

AFPS 05 is also final-salary, building 1/70th of your final pensionable pay for each year served, up to about 57% of pay. It pays an automatic tax-free lump sum of three times your pension and can include an Early Departure Payment if you leave early with enough service.

AFPS 15 is a Career Average Revalued Earnings (CARE) scheme. It adds 1/47th of your current pensionable pay each year, revalued for inflation, rather than using a final salary. There is no automatic lump sum, so you can commute up to 25% of your pension for tax-free cash at a fixed rate of £12 per £1 of yearly pension given up.

How Reserve and FTRS service builds your pension

Since 1 April 2015 there is one armed forces pension scheme for almost everyone in uniform, and that includes the Reserves and Full Time Reserve Service. AFPS 15 is a Career Average Revalued Earnings scheme, usually shortened to CARE. The old picture, where Reserve service sat outside the main pension arrangements, has gone. If you are a mobilised reservist, a Group A or Group B member of the Reserve Forces who is paid for your service, or serving on an FTRS commitment, you are building an AFPS 15 pension in exactly the same way a Regular does. The calculator on this page works on that basis, so the figure you see is built on the same 1/47th accrual the MOD applies to everyone in the scheme.

The principle behind CARE is simple once you have seen it. Each scheme year runs from 1 April to 31 March. For every year you are paid, the scheme takes 1/47th of your pensionable earnings for that year and banks it as a slice of pension. Those slices are added together over your service, and each one is revalued every year so it keeps its value rather than withering with inflation. There is no final salary involved, so a Reserve or FTRS career with varying pay across the years still produces a fair pension, because every year is counted on its own terms rather than being measured against a single final figure.

Two thresholds matter at the start. You need at least 2 years of paid qualifying service before you have earned a pension at all, and your accrual begins from your first day of paid service with no maximum number of years. For reservists whose paid service comes in bursts, mobilisations, bounty-earning training years and FTRS periods, those paid days and years are what count towards the 2 year test and towards your pension pot. Days you are not paid for do not build pension, which is the single biggest difference between a Reserve record and a continuous Regular one.

The 1/47th accrual and how revaluation protects it

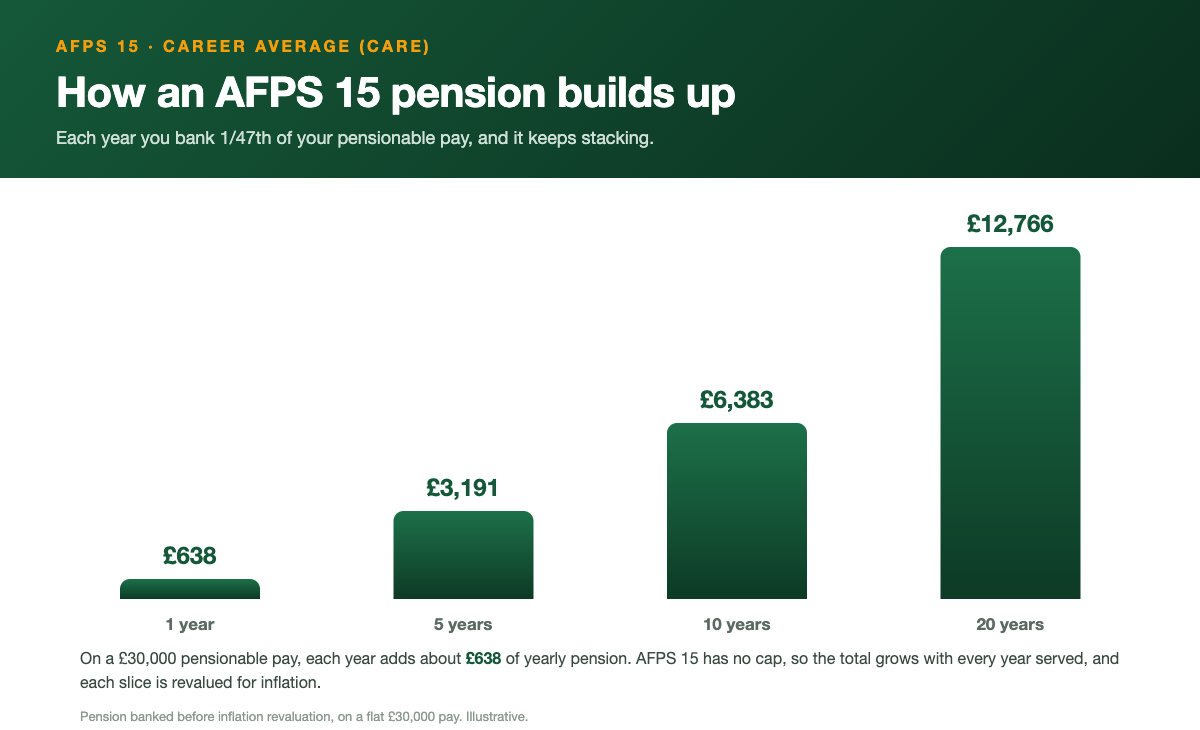

The accrual rate of 1/47th is the heart of AFPS 15, and it is the same whether you serve as a Regular, a reservist or on FTRS. Take your pensionable earnings for a scheme year, divide by 47, and that is the pension you have earned that year. On illustrative round numbers, pensionable earnings of £47,000 in a year would add £1,000 of pension for that year. The next year stands on its own and adds its own slice based on that year's earnings. Over a working life those annual slices add up, and because there is no cap on years, longer paid service simply means more slices.

Revaluation is what stops those slices losing value over a long career. While you are still serving, each banked slice is increased every year in line with earnings growth, so a pension you earned years ago does not fall behind the cost of living or behind today's pay. The official scheme example shows the mechanism: a Year 1 pot of £1,000, after a 2% in-service uplift the following year, becomes £1,020 before the new year's £1,010 slice is added, giving £2,030 across two years. Once you leave and the pension is deferred, or once it is in payment, the yearly increase switches to the Consumer Prices Index instead of earnings.

This is why the calculator asks for your current pensionable pay rather than a true year-by-year history that almost nobody could supply. Because in-service revaluation keeps each past year broadly in step with current earnings, multiplying your current pensionable pay by your paid years and dividing by 47 gives a sound estimate of the whole pot. The shorthand the scheme explainers use, and the one this tool applies, is annual pension is roughly current pensionable pay times years divided by 47. For a reservist, the honest part of that sum is the years figure, because only your paid Reserve and FTRS service counts, not the calendar time since you attested.

Who this affects: Reserves, FTRS and the mobilised

There is no separate reservist scheme to worry about. Members of the Reserve Forces who are paid, those serving on Full Time Reserve Service commitments, and Regulars all accrue in AFPS 15. That means a Reserve officer, a Reserve other rank, an FTRS member and a mobilised reservist are all building pension on the identical 1/47th basis. What differs between them is not the rate but the amount of paid service and the level of pensionable earnings each one racks up, and those two things drive the size of the pot.

If you joined or rejoined from 1 April 2015 your Reserve or FTRS service has always been in AFPS 15. If you had earlier service that fell under a legacy scheme, the McCloud remedy may apply to you. The remedy period runs from 1 April 2015 to 31 March 2022, and members who were affected get to choose legacy or AFPS 15 benefits for that window through a Remediable Service Statement. From 1 April 2022 every serving member, Regular and Reserve alike, builds AFPS 15 only. Reservists with a mixed history should treat this page as covering the AFPS 15 part of their record and check their statement for the rest.

FTRS deserves a specific word because it sits between the Reserve and Regular worlds. While you are on an FTRS commitment you are paid and you accrue AFPS 15 in the normal way, and that paid service counts towards qualifying service and, where eligible, towards Early Departure Payment service tests. The key habit for anyone moving between Reserve, FTRS and Regular states is to keep your own record of paid days and periods, because your pension reflects what you were actually paid for, not the labels on your service over the years.

Combining Reserve, FTRS and Regular service

Because there is one scheme, paid service in different capacities can sit together in the same AFPS 15 pot rather than fragmenting into separate small pensions. A person who serves as a Regular, leaves, then returns as a reservist or on FTRS is adding more 1/47th slices to the same career-average pot, provided the service is paid and pensionable. This is a real advantage of the single scheme: time does not have to be wasted just because your relationship with the forces changed shape.

Where it gets more involved is the boundary between AFPS 15 and the legacy schemes. Any pension you built up in AFPS 75 or AFPS 05 before moving into AFPS 15 is protected as an accrued right and is paid on its own terms when it falls due, linked to the rules and pay position that applied when you left that service. It does not magically convert into CARE slices. So a long-serving member can end up with a legacy element and an AFPS 15 element, and a reservist who has dipped in and out can have AFPS 15 service spread across several paid periods.

The calculator on this page models the AFPS 15 part. If you have legacy service as well, estimate that separately using the AFPS 75 or AFPS 05 calculator and add the results together for a fuller picture. The one thing not to do is double count: a given period of paid service belongs to one scheme, and after the remedy choices are settled your Remediable Service Statement is the document that tells you exactly which years sit where.

Early Departure Payment for early leavers

Early Departure Payment, or EDP, is the bridge for people who leave with substantial service but before pension age, and it can matter to FTRS members and long-serving reservists as much as to Regulars. Under AFPS 15 the qualifying point is broadly 20 years of service and age 40, often called the 20/40 point. If you reach it, you receive a tax-free lump sum plus a taxable monthly income that runs until pension age, at which point your deferred pension itself comes into payment.

The figures the scheme uses are concrete. The EDP 15 lump sum is 2.25 times your deferred pension. The monthly income starts at 34% of the deferred pension at the 20/40 point, and it grows by 0.85% of the deferred pension for every whole year you serve beyond 20 years. The income is paid flat until age 55 and then picks up Consumer Prices Index increases. EDP is not a separate pot you have saved, it is an early-access arrangement built on top of the pension you have already earned, so a bigger deferred pension means a bigger EDP in proportion.

For reservists the practical sticking point is almost always the service test rather than the rules. Twenty years of paid, qualifying service is a high bar to clear on Reserve or intermittent FTRS service alone, so EDP tends to be most relevant where Reserve or FTRS time joins onto a substantial Regular career in the same AFPS 15 pot. If you are nowhere near the 20/40 point when you leave, you will instead hold a deferred AFPS 15 pension that you claim later rather than an EDP, and that is the normal outcome for most short and medium Reserve engagements.

A worked example (illustrative)

Here is an illustrative example using only the scheme figures above, to show how the sum is built rather than to forecast any real person's benefits. Imagine a member with 10 years of paid AFPS 15 service and current pensionable earnings of £47,000. Using the scheme shorthand of pay times years divided by 47, the estimated annual pension is £47,000 times 10 divided by 47, which is £10,000 a year. That is the deferred pension the calculator would show before any commutation, and it would later rise with the Consumer Prices Index once deferred or in payment.

AFPS 15 pays no automatic lump sum, so any tax-free cash comes from commutation, giving up part of your annual pension in exchange for a one-off sum. The rate is fixed at about £12 of lump sum for every £1 of yearly pension surrendered, and you can commute up to 25% of your pension. On our illustrative £10,000 pension, commuting the full 25% means giving up £2,500 of annual pension to receive a tax-free lump sum of £2,500 times 12, which is £30,000, leaving a reduced pension of £7,500 a year. The reduction is permanent, so this is a genuine trade, not free money.

Now suppose that same member had reached the 20/40 point, with 20 years of paid service and a deferred pension worked out the same way. The EDP lump sum would be 2.25 times that deferred pension, and the EDP monthly income would start at 34% of the deferred pension, growing by 0.85% of it for each year served beyond 20. These numbers move directly with the size of the deferred pension, which is why getting your paid years right is the single most important input. Treat every figure here as a rounded illustration, not a quote, and use the calculator above with your own pay and paid years.

How the tax works

The headline points on tax are worth keeping straight, because they shape what actually lands in your bank account. Your AFPS 15 pension in payment is taxable as income in the normal way, through PAYE, just like a salary. The contributions side is handled for you while you serve, so your accrual builds without you needing to claim anything back each year. What you see in the calculator is a gross pension figure, before income tax, so the spending money is lower once tax is applied at your marginal rate in retirement.

Lump sums are treated more kindly. A lump sum you create by commuting AFPS 15 pension is tax-free within the HMRC limits, which is the main reason members consider commutation despite the permanent reduction to the yearly pension. The EDP lump sum of 2.25 times the deferred pension is also a tax-free one-off payment. The EDP monthly income, by contrast, is taxable as it is paid, so when you budget for the years between leaving and pension age, work on the after-tax value of that income rather than the gross figure.

Two cautions for anyone with a fuller financial picture. Very large pension benefits can run into HMRC allowances, and people with several pensions or other income can find a tax bill they did not expect, so professional advice is sensible once the numbers get big. This site gives estimates and general education, not regulated financial advice, and we are not able to tell you the tax outcome for your exact circumstances. For that, speak to a suitably qualified adviser and use your own tax position.

How to check your own figure

This calculator gives you a quick, honest estimate, but it is not an official forecast and it cannot see your service record. The figures here rest on the 1/47th accrual and the scheme shorthand of current pay times paid years divided by 47, which is a sound approximation but a simplification. Treat the result as a sanity check and a planning aid, the kind of number you would want before a conversation about your future, not a guarantee of what you will be paid.

For a figure you can rely on, get an official forecast from Veterans UK. Serving members request it using form 12, and those with a preserved or deferred pension use form 14. That forecast is based on your actual recorded service and pay, so it will reflect your real paid Reserve, FTRS and Regular periods rather than an estimate. If you served across the McCloud remedy period of 1 April 2015 to 31 March 2022, your Remediable Service Statement is the document that shows your legacy and AFPS 15 positions side by side so you can compare them.

Before you ask for any forecast, do a little admin of your own. Check that your paid service is recorded correctly, especially mobilisations and FTRS commitments, because gaps or missing periods are the most common reason an estimate and a forecast disagree. Note your current pensionable pay, add up your paid years as honestly as you can, and keep any pension paperwork together. The better your inputs, the closer the estimate above will be to the official number when it arrives.

Common mistakes and next steps

The mistake that catches reservists most often is counting calendar time instead of paid time. The pension is built from paid, pensionable service, so the years that count are the ones you were actually paid for, not the span between attestation and discharge. A reservist with a 15 year relationship with the forces but only a handful of fully paid years will have a much smaller pot than the calendar suggests, and being realistic about paid years is the difference between a useful estimate and a disappointing surprise.

Other frequent errors are assuming there is an automatic lump sum, there is not under AFPS 15, you create one by commuting, and assuming EDP is easy to reach on Reserve service alone, when the 20/40 service test is demanding. Some members also forget that legacy AFPS 75 or AFPS 05 service is separate and protected, and try to fold it into one CARE figure. Keep the schemes apart, estimate each on its own calculator, and add the results rather than blending them.

As next steps, start with the calculator above using your current pensionable pay and your honest count of paid years, and try the commutation slider to see the trade between a smaller pension and a tax-free lump sum. Then request an official forecast from Veterans UK using form 12 if you are serving or form 14 if your pension is preserved. If McCloud applies to you, read your Remediable Service Statement carefully before you make any choice. And if the numbers are large or your affairs are complicated, get regulated financial advice, because this site offers estimates and education, not a personal recommendation. We are an independent site and are not affiliated with the MOD, Veterans UK or JPAC.

Reserve service before April 2015: the Milroy case

Everything above concerns AFPS 15, which has covered paid Reserve and FTRS service since 1 April 2015. Service before that date is a live legal question rather than a settled one, and it is worth knowing where it stands.

In August 2024 an employment tribunal found that the MOD had treated Major Charles Milroy less favourably as a part time worker by denying him access to AFPS 75 and its successor schemes, and by calculating his daily rate of pay by dividing a regular's annual salary by 365.25, which failed to reflect the days regulars are not working. The Employment Appeal Tribunal refused the MOD's appeal on all four grounds on 29 January 2026.

If it stands, the decision points towards non mobilised reserve service before 1 April 2015 having been pensionable under AFPS 75 or AFPS 05, subject to the two year qualifying period, and towards the 365.25 divisor having been wrong.

This is not settled. The MOD has taken the case to the Court of Session, which hears it on 8 October 2026, so no reservist should assume an entitlement or a payment. This calculator therefore covers AFPS 15 service only and does not estimate pre 2015 reserve service. Our news post on the Milroy reservists' pension ruling tracks the case.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Not sure which scheme you're in?

Find out whether you're on AFPS 75, 05 or 15 and how each builds up.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.