McCloud Remedy Calculator (AFPS 15)

Compare your legacy scheme and AFPS 15 benefits for the McCloud remedy period (1 April 2015 to 31 March 2022) to weigh up your choice.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 15 (20/40 early leaver)

How this is worked out

AFPS 15 is CARE: 1/47th of pay each year, revalued by earnings while you serve. Enter your current pensionable pay. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the McCloud Remedy estimate is worked out

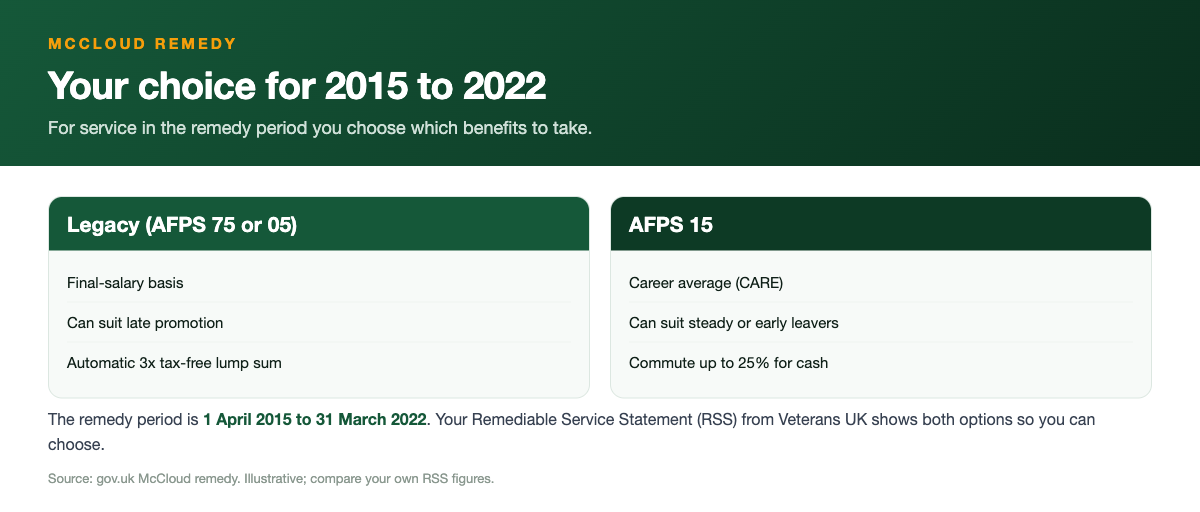

The McCloud remedy covers service between 1 April 2015 and 31 March 2022. For that period eligible members can choose between their legacy scheme (AFPS 75 or 05) and AFPS 15.

This comparison estimates the benefits each option would give so you can see which is likely to be better for you. The binding figures arrive in your official Remediable Service Statement.

What the McCloud remedy actually changes

When the armed forces moved everyone onto AFPS 15 in 2015, older members were given transitional protection that let them stay in their legacy scheme, AFPS 75 or AFPS 05, for longer. The courts found that protecting older members this way was age discrimination against younger members who were forced straight into AFPS 15. The fix, known as the McCloud remedy, puts the affected years back on a level footing by giving you a choice of which scheme covers that window.

The window that matters is the remedy period: 1 April 2015 to 31 March 2022. For service inside those dates, eligible members can choose whether the benefits are worked out under their legacy scheme (AFPS 75 or AFPS 05) or under AFPS 15. From 1 April 2022 onward, the choice ends and everyone who is still serving builds AFPS 15 going forward. So the remedy is not about your whole career, it is about getting the best of two scheme designs for one seven year block.

This calculator exists to put numbers on that block. It compares what the remedy years are worth under your legacy final salary terms against what the same years are worth as AFPS 15 career average benefits, so you can see the gap before you make a binding decision. Treat every figure here as an illustrative estimate. The only binding numbers come from your own Remediable Service Statement and an official forecast from Veterans UK.

Who is in scope and who is not

You are in scope for a McCloud choice if you had qualifying service during the remedy period and you were a member of a legacy scheme (AFPS 75 or AFPS 05) before April 2015, or had service that links to one. In practice this captures most regulars and many reservists who were serving across 2015. If you joined for the first time on or after 1 April 2015, you were always an AFPS 15 member and there is no legacy alternative to compare, so the remedy choice does not apply to you.

It also helps to be clear about what is not on the table. The choice only ever covers the 2015 to 2022 remedy period. Service before 1 April 2015 stays in whatever legacy scheme you were in, and service from 1 April 2022 is AFPS 15 for everyone. You cannot mix and match year by year inside the remedy period either. You pick one scheme to cover the whole block, and that decision applies to all the benefits flowing from those years, including any survivor and lump sum entitlements.

One more group to flag: you still need at least two years of qualifying service to have earned a pension at all. If your total service falls short of that, the remedy choice is academic because there is no pension to shape. Most people reading this will be well past that threshold, but it is worth checking before you spend time weighing options.

Legacy final salary versus AFPS 15 for the remedy years

The two options are built on completely different engines, which is why the comparison is worth doing properly. AFPS 75 and AFPS 05 are final salary schemes: the pension for your remedy years is tied to your pay near the end of your career, not your pay back in 2015 to 2022. AFPS 05 builds 1/70th of final pensionable pay for each year, up to a maximum of about 57 percent over a full career, and pays an automatic tax free lump sum of three times the annual pension. AFPS 75 builds toward up to 48.5 percent of final pay over a full career and also carries an automatic lump sum of three times the pension.

AFPS 15 works differently. It is a Career Average Revalued Earnings, or CARE, scheme. Each year it banks 1/47th of that year's pensionable pay into a pot, and the pot is revalued every year to keep its value up while you serve. There is no automatic lump sum under AFPS 15, although you can commute up to 25 percent of the pension for tax free cash at a fixed rate of about 12 to 1, meaning roughly 12 pounds of lump sum for every 1 pound of annual pension you give up.

Which design wins for your remedy years depends heavily on your career shape. If your pay rose sharply after the remedy period, for example through promotion, the final salary link in AFPS 75 or AFPS 05 can make those years worth noticeably more, because they are valued against your higher later pay. If your pay was relatively flat, or you left soon after the remedy period, the AFPS 15 CARE figures can look more competitive. There is no single right answer, which is exactly why a member by member comparison matters.

Your Remediable Service Statement is the source of truth

The official document that drives your decision is the Remediable Service Statement, usually shortened to RSS. It sets out, in pounds, what your remedy period service is worth under your legacy scheme and what it is worth under AFPS 15, so you can compare like for like. This calculator is designed to give you a feel for the shape and size of that gap in advance, but the RSS figures are the ones that count when you commit.

Read the RSS alongside this tool rather than instead of it. Use the calculator to understand why the two columns differ, to test what happens if your final pay ends up higher or lower than you expect, and to sanity check that the official numbers move in the direction you would predict. If the RSS and your own estimate point in wildly different directions, that is a signal to ask Veterans UK to talk you through the figures before you choose.

Keep in mind that the RSS reflects assumptions about your future, such as when you leave and what your pay is at that point. Because the legacy option is a final salary calculation, its value is not fixed until your pay is fixed. That is one reason the decision for many people is taken at the point benefits become payable rather than years earlier, which we cover next.

Immediate choice versus deferred choice

There are two moments at which a McCloud choice can be made, and it matters which one applies to you. If you have already retired and your pension is in payment, or you are at the point of claiming, you make an immediate choice: you decide now, with most of the relevant facts known, which scheme covers your remedy years. For these members the decision is concrete because final pay and leaving date are settled, so the figures in your statement are close to final.

If you are still serving and years away from drawing benefits, you fall into the deferred choice group. You do not have to decide today. Instead you make the election when your benefits actually become payable, by which time your final pay and exit date are known and the comparison is no longer a guess. This is sensible, because the legacy option is a final salary calculation whose value depends on pay you have not yet earned. Locking in a choice too early could mean choosing on the basis of figures that later change.

The practical takeaway: serving members should treat this calculator as a planning aid, not a one time decision tool. Run it again as your career develops, especially after a promotion or a pay change, because the balance between the legacy and AFPS 15 figures can shift. The actual election is something you confirm later, with your RSS in hand and, ideally, advice that reflects your full circumstances.

Tax and the Annual Allowance angle

The McCloud choice is not only about which scheme pays the bigger pension. It can also change the tax position of the remedy years, because the amount of pension you are treated as building in a given year feeds into the pensions Annual Allowance. The Annual Allowance is the limit on how much pension growth can be added in a tax year before a tax charge can apply, and a final salary scheme and a CARE scheme can produce very different growth figures for the same period.

When the remedy reworks your past years, it can change the growth recorded for those years, which in turn can change whether an Annual Allowance charge was due, too high, or too low at the time. The remedy framework includes a process to put this right, so that members are not left out of pocket or unexpectedly liable purely because of a scheme they did not choose to be in. You handle any change through HMRC's Calculate your public service pension adjustment service rather than Self Assessment, and if a charge is due you can ask the scheme to settle it through Scheme Pays: because Remediable Service Statements were delayed, the mandatory Scheme Pays deadline for remedy cases has been extended to 6 July 2027. If you ever paid an Annual Allowance charge during or near the remedy period, this is an area to raise specifically.

This is genuinely technical territory and it is where general guidance stops being enough. We are an independent education site and we do not provide regulated financial or tax advice. If your pension growth was anywhere near the Annual Allowance in those years, or you have a large legacy pension, get the figures checked by a qualified adviser and use the official process before you finalise your election. The calculator deliberately does not estimate tax charges, because they depend on personal allowances and income that vary from member to member.

How to weigh the two options sensibly

Start with the headline question: does your career bend the comparison toward final salary or toward CARE? Final salary links the remedy years to your pay at the end. So if you have been promoted since 2015, or expect to be before you leave, the legacy option tends to gain value because those years ride on your higher later pay. A flatter pay history, or an early exit shortly after the remedy period, tends to favour AFPS 15, whose value for those years was banked and revalued as you went.

Then layer in the shape of the benefits, not just the size. AFPS 75 and AFPS 05 hand you an automatic tax free lump sum of three times the pension, which some people value highly for clearing a mortgage or settling on resettlement. AFPS 15 gives no automatic lump sum but lets you commute up to a quarter of the pension at about 12 to 1 if you want cash. The pension ages differ too: AFPS 75 and AFPS 05 both have a normal pension age of 55, while AFPS 15 has a normal pension age of 60. Leave before those ages and the payment date moves out, to 60 or 65 for a preserved AFPS 75 pension, 65 for a preserved AFPS 05 pension, and your State Pension age for a deferred AFPS 15 pension, so when the money starts is part of the decision, not an afterthought.

Finally, think about certainty and survivors. A bigger headline pension is not automatically the right pick if it comes with a later start date that does not suit your plans, or if the lump sum structure does not match what you need at the point of leaving. Look at the whole package each option produces for your remedy years, including survivor benefits, and weigh it against your own timeline. When the two columns are close, the non monetary factors, such as when the pension is payable, often decide it.

An illustrative worked example

Here is an illustrative example to show the mechanics, using only the standard scheme figures and round numbers. Imagine a soldier with pensionable pay of 47,000 pounds who is comparing how a single year of remedy period service is valued. Under AFPS 05 final salary terms, one year builds 1/70th of pay, which is 47,000 divided by 70, about 671 pounds of annual pension for that year, and because AFPS 05 pays an automatic lump sum, that pension also carries three times its value as tax free cash.

Under AFPS 15, that same year banks 1/47th of pay, which is 47,000 divided by 47, exactly 1,000 pounds added to the CARE pot for that year, revalued each year thereafter. On these figures the AFPS 15 accrual for the single year looks larger, but that is only half the story. The AFPS 05 figure is pegged to final pay, so if this member is later promoted and their final pensionable pay rises well above 47,000, the legacy value for that year rises with it, while the AFPS 15 figure for that year was set against the pay actually earned and then revalued.

That is the whole tension in one example. The CARE scheme often shows a stronger raw accrual rate, while the final salary scheme can overtake it for members whose pay climbs after the remedy period, plus it brings an automatic lump sum and different pension ages. Multiply this across up to seven remedy years and you can see why the gap is rarely obvious by eye. These figures are illustrative only and use the headline scheme rates. Your real numbers will come from your Remediable Service Statement and an official forecast.

How to check your own position and what to do next

Use this calculator first to get a feel for the size and direction of the gap between your legacy and AFPS 15 benefits for the remedy years. Enter your current details, look at how the two scheme designs treat the same service, and test a higher and a lower final pay so you can see how sensitive the legacy option is to your pay at exit. That gives you an informed starting point rather than a blank page.

Next, get the official numbers. Request or read your Remediable Service Statement, which lays out the legacy and AFPS 15 values side by side, and for a binding forecast contact Veterans UK using form 12 if you are still serving or form 14 if your pension is preserved. Those are the authoritative sources. We are an independent site and not affiliated with the MOD, Veterans UK or JPAC, and nothing here is regulated financial advice.

Finally, if the decision is close, the numbers are large, or there is any Annual Allowance history in those years, take qualified advice before you elect. The choice can have a real and lasting effect on your retirement income, so it is worth getting right. Most serving members will confirm their election later, at the point benefits become payable, so there is usually time to plan properly rather than rush. Use the tool to stay oriented, and let the official statement and a professional confirm the call.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Read the McCloud remedy guide

What the 2015 to 2022 remedy means for your legacy vs AFPS 15 choice.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.