Armed forces pension commutation explained

Commutation means giving up part of your annual pension in exchange for a larger tax-free lump sum on the day you draw your benefits. It matters most on AFPS 15, which has no automatic lump sum, but it also applies as resettlement commutation on the older AFPS 75 and AFPS 05 schemes. The choice is permanent, so it pays to understand exactly what you are trading before you sign.

Key takeaways

- Commutation swaps guaranteed yearly pension for a one-off tax-free lump sum, and the decision cannot be reversed.

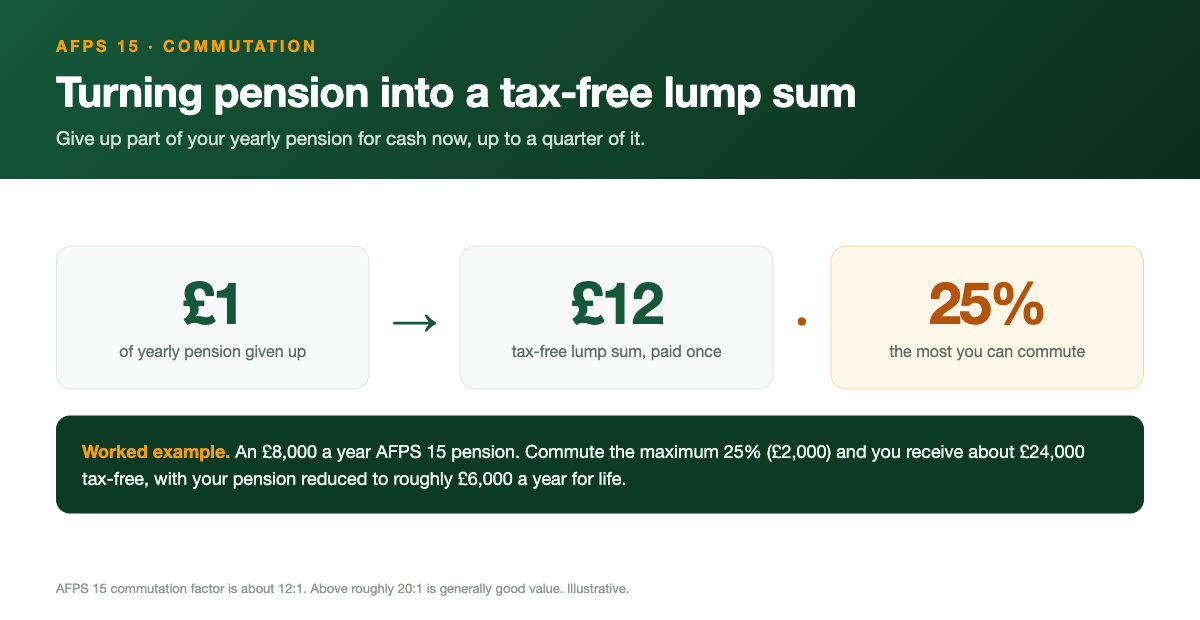

- On AFPS 15 you can commute up to 25% of your pension at a fixed rate of about 12:1, roughly 12 pounds of cash for every 1 pound of yearly pension given up.

- GAD (the Government Actuary's Department) publishes the commutation factors; a factor above roughly 20:1 is generally considered good value.

- AFPS 75 and AFPS 05 already pay an automatic tax-free lump sum of 3 times the annual pension; resettlement commutation is a separate option on top.

- You give up income that rises with inflation each year, so the longer you expect to draw your pension, the less attractive commuting becomes.

- Because the choice is irreversible, regulated advice is worth taking, and an official forecast comes from Veterans UK, not from estimates like ours.

What commutation actually is

Commutation is the act of turning some of your future pension income into cash today. You tell the scheme you want to give up a slice of your annual pension, and in return it hands you a tax-free lump sum when your pension comes into payment. The pension you keep is then permanently smaller for life, but you have a larger sum at the start.

Be clear about what it is not. Commutation is not a loan, and it is not a separate pot the scheme has been holding for you. Every pound of lump sum comes directly out of the pension you would otherwise have received, year after year, for as long as you live. You are exchanging guaranteed, inflation-linked income for life in return for capital now.

How the GAD commutation factor works

The amount of lump sum each pound of surrendered pension buys is set by a commutation factor. These factors are published by the Government Actuary's Department, known as GAD, which does the sums for public service pensions. A factor is simply a multiplier: a factor of 12:1 means every 1 pound of yearly pension you give up turns into 12 pounds of tax-free cash.

On the legacy schemes the factors are age-banded, so the exact figure depends on your age in years and months when you take the benefit, and a younger member generally sees a higher factor because the scheme expects to pay them for longer, all of which is set out in the published commutation factors tables. AFPS 15 is much simpler: its rate is fixed scheme-wide at about 12:1 regardless of age. That makes the sum easy to work out, but it is not especially generous, because a factor above roughly 20:1 is generally good value and 12:1 sits well below that.

The 25% cap and the 12-to-1 rate on AFPS 15

AFPS 15 is a career average (CARE) scheme, and unlike the older schemes it pays no automatic lump sum at all. If you want tax-free cash on leaving, the only way to create it is to commute, so doing nothing means you receive no lump sum whatsoever. That makes the decision far more central on AFPS 15 than on the legacy schemes.

Two figures govern how much you can take. The rate is fixed at about 12:1, so each 1 pound of annual pension you surrender produces about 12 pounds of lump sum, and there is a cap of no more than 25% of your pension that you cannot push past however much you want the money up front.

The mechanics work in three steps: decide what percentage to give up, up to the 25% ceiling; multiply the pension you surrender by 12 to get the lump sum; then subtract that surrendered amount from your starting pension to find the reduced pension you keep, which is what rises each year with inflation. The 25% limit is set by HMRC against the capitalised value of your benefits, so your official Veterans UK forecast will confirm the precise maximum.

A worked example with the maths

Here is an illustrative example, and you can run the same arithmetic on your own pension with the commutation calculator. The figures are made up to keep the arithmetic clean; your own pension will differ, and only your Veterans UK forecast is authoritative. Suppose a member has an annual AFPS 15 pension of 10,000 pounds and decides to commute the full 25% allowed.

Giving up 25% of a 10,000 pound pension means surrendering 2,500 pounds of yearly income. At the fixed rate of about 12:1, that 2,500 pounds is multiplied by 12 to produce a tax-free lump sum of 30,000 pounds, and the pension that remains in payment is 10,000 minus 2,500, which is 7,500 pounds a year. So the trade is a 30,000 pound tax-free sum now in exchange for 2,500 pounds a year less, every year, for the rest of the member's life.

On a rough cash basis, 30,000 divided by 2,500 is 12, so the lump sum is worth about twelve years of the income you gave up before you even count the lost inflation rises. Because pensions in payment rise with inflation, for example by 3.8% from April 2026 under CPI, the income you surrendered would have grown each year, so the longer you live the more it adds up.

Resettlement commutation on AFPS 75 and AFPS 05

The older schemes work differently because they are final-salary schemes and already pay an automatic tax-free lump sum of 3 times your annual pension. That lump sum is built in: you do not have to ask for it or give anything up, and it arrives alongside your pension as standard. For many members on AFPS 75 or AFPS 05, it is all the tax-free cash they ever take, and the armed forces pension lump sum guide sets out how that automatic payment is worked out.

On top of that, the legacy schemes allow resettlement commutation, a separate option to draw extra cash by surrendering more pension, using its own age-banded GAD factor table rather than the fixed AFPS 15 rate. There is an important catch: in some re-employment cases it can be repayable, so if you go back into qualifying service the scheme may want some of it back. Because the figures rest on age-banded tables and your own circumstances, a general calculator cannot model it precisely, so get the exact numbers from Veterans UK.

Tax treatment and the Lump Sum Allowance

The headline news is good: the lump sum from standard commutation is paid tax-free. That is one of the main reasons commutation is attractive, because converting taxable pension income into tax-free capital can look efficient on paper, especially for someone who expects to be a higher-rate taxpayer in retirement.

There is a ceiling to be aware of, called the Lump Sum Allowance, which is the total tax-free lump sum you can take across all your pensions over your lifetime. For most members a commuted lump sum sits comfortably within it, but very large sums, or large sums combined with other pension benefits, can interact with the allowance and lose their tax-free status above the limit. If you have benefits from more than one scheme or significant private savings, this is exactly the kind of thing a regulated adviser should check before you commit.

How to judge whether a factor is good value

The single most useful number is the commutation factor itself, because it tells you how many pounds of cash you get for each pound of pension surrendered, and the higher the factor, the better the deal. As a broad benchmark, a factor above roughly 20:1 is generally considered good value, while the fixed AFPS 15 rate of about 12:1 is markedly less generous.

A simple sanity check is to ask how many years of the surrendered income the lump sum represents: a 12:1 factor means the cash equals about twelve years of the pension you gave up, before the inflation rises you also forfeit. If you expect to draw your pension for far longer than that, which most healthy people leaving in their forties or fifties will, the maths increasingly favours keeping the income. A shorter life expectancy moves the balance toward cash, and a clear use such as clearing a mortgage carries real value, whereas commuting just to leave money in a savings account rarely beats a guaranteed, index-linked income, which is the heart of whether it is worth commuting your pension.

Common mistakes to avoid

The most common mistake is treating commutation as free money rather than a swap. The lump sum is not a bonus the scheme is handing over; it is your own future pension, paid early and at a fixed rate. Forgetting that it comes straight out of guaranteed lifetime income is how people commute more than they need and regret the smaller pension years later.

A second mistake is ignoring the inflation link, because the pension you give up would have risen with CPI every year, so surrendering it costs you not just the current amount but every future uplift on it. Other frequent slips include commuting the maximum 25% by default without asking whether you need that much, overlooking that resettlement commutation can be repayable if you rejoin, and assuming the lump sum is always tax-free. Commutation is permanent, so take the figures from your official Veterans UK forecast, ideally checked by a regulated adviser, before you commit.

How to decide

Start with whether you genuinely need a lump sum at all. If you have a clear, valuable use for the cash, such as clearing a mortgage, paying down expensive debt, or funding retraining or a business on resettlement, commutation can be a sensible way to fund it. If you have no concrete need and the money would simply sit in the bank, keeping the guaranteed, inflation-linked income is usually the stronger choice, and on AFPS 75 or AFPS 05 inverse commutation can turn part of the automatic lump sum into extra income instead.

If you do decide to commute, commute only what you need rather than the maximum out of habit, because the AFPS 15 rate of about 12:1 is below the 20:1 level generally regarded as good value, so every extra pound you surrender is a relatively poor trade. Above all, get the real numbers and proper advice before you sign. We are an independent education site and not affiliated with the MOD or Veterans UK, and everything here is an estimate rather than regulated financial advice, so an official forecast from Veterans UK and a regulated adviser who knows the armed forces schemes are well worth the effort.

See your own numbers

Get your pension, lump sum and EDP in seconds.

Frequently asked questions

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk · GAD factors · Veterans UK · Forces Pension Society · MoneyHelper.