AFPS 15 Pension Calculator

Estimate your AFPS 15 pension on the Career Average (CARE) basis, see how much you can commute for tax-free cash, and check your Early Departure Payment. Updated for the 2026 increase (3.8%).

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 15 (20/40 early leaver)

How this is worked out

AFPS 15 is CARE: 1/47th of pay each year, revalued by earnings while you serve. Enter your current pensionable pay. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

AFPS 15 at a glance

How an AFPS 15 pension is calculated

AFPS 15 is a Career Average Revalued Earnings (CARE) scheme. Every scheme year, which runs from 1 April to 31 March, the MOD takes your pensionable earnings for that year, divides them by 47, and adds the result to a running total often called your pension pot. Do that for every year you serve and you have built a pension. There is no rank multiplier and no secret formula. It is steady, year on year banking of 1/47th of what you were paid, and the longer you serve the bigger the pot grows.

Pensionable earnings here means your basic pay plus the pay elements that count towards pension, such as recruitment and retention pay where it applies. It does not normally include allowances that are paid to cover a cost rather than reward the job. If you are unsure exactly what counts in your case, your pay statement and your annual benefit statement will show the pensionable figure the scheme is actually using.

While you serve, the whole pot is revalued each year so it keeps its value rather than being frozen at the cash amount you earned a decade ago. Once you leave or start drawing the pension, it rises with prices, measured by the Consumer Prices Index. That two stage approach, earnings linked growth while serving and price linked growth afterwards, is the heart of how a career average scheme protects you.

Because the in service revaluation broadly tracks earnings, you do not need to dig out a true career average of every year's salary to get a sound estimate. Entering your current pensionable payworks well, because each past year's slice has been kept roughly in line with today's pay levels. The shorthand the calculator uses is simple: current pensionable pay multiplied by years served, divided by 47. It then applies the latest annual increase so the figure reflects this year's uprating.

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI). For an official figure request a forecast from Veterans UK. See how we calculate for the full method.

CARE versus final salary, and why it changed

If you served before April 2015 you will have heard pensions talked about in final salary terms. The old AFPS 75 and AFPS 05 schemes worked out your pension from your rank and pay near the end of your career, then multiplied by your years of service. That rewarded a steep climb late on, because the high pay at the finish was applied to all of your earlier service.

A career average scheme works differently. Each year stands on its own. The pay you earned as a junior rank builds pension at that year's level, the pay you earn as a senior rank builds pension at that year's level, and the scheme adds them up. Nobody's final year is stretched back across a whole career. For a steady earner the two methods can land in a similar place. For someone who is promoted hard and fast at the very end, final salary tended to be more generous; for someone whose pay was strong throughout, or who has a long flat period, career average can hold up well because every good year counts in full.

The headline reason for the move was fairness and cost across the whole public sector. Final salary schemes quietly favoured high flyers and were expensive to fund. Career average ties the benefit to what you actually earned each year, which is easier to predict and spreads the value more evenly across ranks. Whatever your view of the change, the practical point is the same: with AFPS 15 it is your full record of pensionable pay, year by year, that matters, not just your pay on the day you hang up your boots.

If you have service in both, it is worth seeing the two methods set side by side on the same career, because the gap between them is what the McCloud choice turns on: final salary versus CARE works through where each one wins.

The 1/47 build up and annual revaluation

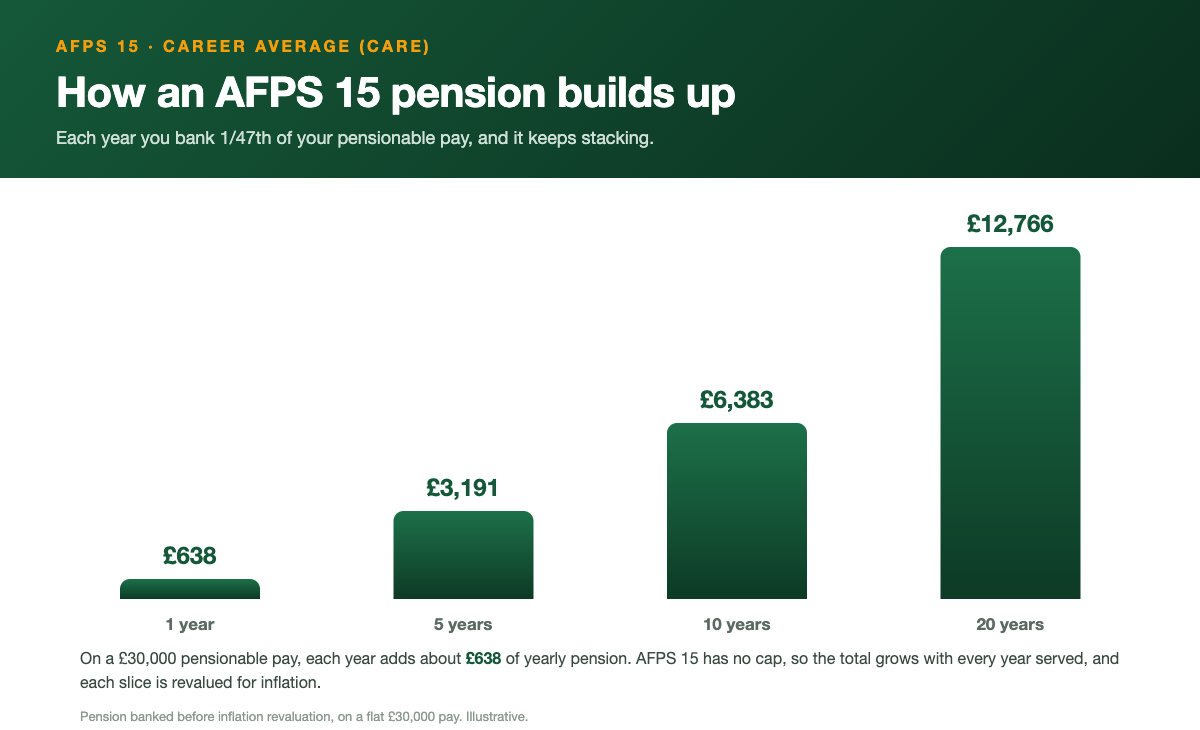

The accrual rate is the engine of the scheme, so it is worth being precise. Each year you bank 1/47thof that year's pensionable pay. As a rough feel, 1/47th is a little over 2 percent, so every year of service adds a touch more than 2 percent of your pay to your annual pension. Across a full career that compounds into a meaningful income for life.

Revaluation is what stops those yearly slices going stale. While you are still serving, the running total is increased each year to keep pace with earnings, so the pension you built early in your career does not wither against later pay. After you leave, or once the pension is in payment, the increases switch to prices through CPI. The official scheme guidance gives a clean illustration of the serving stage. The numbers below are taken from that guidance to show the mechanism, not to predict your own pension.

Illustrative, scheme guidance figures. Year 1, earnings of £47,000 divided by 47 add £1,000 to the pot. Year 2, earnings of £47,500 divided by 47 add £1,010. With a 2 percent revaluation on the first year, the pot becomes £1,000 plus £20 plus £1,010, which is £2,030. The pattern repeats every year you serve.

Two things follow from this. First, there is no cap on the number of years you can build, so a long career keeps adding value rather than hitting a ceiling. Second, you need at least two years of qualifying service to earn a pension at all; serve less than that and different rules apply to what you take away. Pension begins building from your first day of paid service, so the clock starts early even if the qualifying gate sits at two years.

Are you in AFPS 15?

For practical purposes, if you are serving today you are building your pension in AFPS 15. From 1 April 2022 all serving members accrue in this scheme, whatever they were in before. Anyone who joined the Armed Forces on or after 1 April 2015 has always been in AFPS 15. That means the active scheme is the same for the whole force, from a recently attested recruit to a long serving Warrant Officer.

What differs between people is the history. If you served before April 2015 you will also hold benefits in AFPS 75 or AFPS 05. Those are not lost. Pension built up in an older scheme before you moved across is protected and paid under that scheme's own rules, including its own pension age and its automatic lump sum. So a typical mid career member ends up with two entitlements running side by side: a legacy slice and an AFPS 15 slice. The calculator on this page estimates the AFPS 15 part; use the AFPS 75 and AFPS 05 tools for the legacy part.

You accrue in AFPS 15 if

- You joined the Armed Forces on or after 1 April 2015.

- You were serving on 1 April 2022. Everyone moved to AFPS 15 then.

- You are a Regular or Reserve member with at least two years' qualifying service.

You also have legacy benefits if

- You served before 1 April 2015 in AFPS 75 or AFPS 05.

- Those benefits are protected and paid when originally expected.

- The McCloud remedy lets you choose legacy or AFPS 15 for the remedy period.

AFPS 15 and the McCloud remedy

When the schemes changed in 2015, older members were given transitional protection and kept in their legacy scheme for a time, while younger members moved straight to AFPS 15. The courts found that treating members differently by age was unlawful. The fix is known as the McCloud remedy, and it is the reason everyone was moved into AFPS 15 from April 2022 and the reason there is a choice to be made about the years in between.

The remedy period covers service from 1 April 2015 to 31 March 2022. For that window, eligible members get a choice of benefits, legacy or AFPS 15, made at the point the pension becomes payable rather than now. The idea is that nobody is forced to take the less valuable option for those years simply because of how old they were in 2015. For most people the sensible moment to decide is when the numbers are clear, near the point of claiming, so you can compare the two on real figures rather than guesses.

What this means for your estimate is straightforward. The years before April 2015 are pure legacy scheme. The years from April 2022 onward are pure AFPS 15. The remedy period is the part where a choice applies later. If you only ever served inside AFPS 15, none of this affects you and the calculator covers your whole pension. If you straddle the change, treat the AFPS 15 figure here as one part of a bigger picture and read the dedicated remedy guidance before making any decision.

The figures for that choice do not come from a calculator. They arrive on your remediable service statement, the official document that sets the legacy and AFPS 15 benefits for the remedy period against each other so you can compare them on your own record.

Affected by the remedy?

See how the legacy and AFPS 15 choice works for service between 2015 and 2022.

AFPS 15 pension at common service lengths

Based on £45,000 of current pensionable pay. The annual pension is shown before any commutation; the last column shows the maximum tax-free lump sum if you commute the full 25%.

| Years of service | Annual pension | Monthly | Max lump (25% commuted) |

|---|---|---|---|

| 16 years | £15,319 | £1,277 | £45,957 |

| 20 years | £19,149 | £1,596 | £57,447 |

| 25 years | £23,936 | £1,995 | £71,809 |

| 30 years | £28,723 | £2,394 | £86,170 |

| 35 years | £33,511 | £2,793 | £100,532 |

Commuting the full 25% reduces the annual pension to 75% of the figure shown. Use the calculator for your exact split.

Building up an AFPS 15 pension over a career

It helps to walk one career through, slowly, so the 1/47th rhythm makes sense. The figures below are illustrative and use the same flat £45,000 of pensionable pay as the table above, so you can see the shape clearly. Real careers see pay rise, and revaluation keeps the early years honest, but holding pay steady makes the build up obvious.

Think of a member, call him a Corporal moving up to Sergeant and beyond, who serves a full engagement. After 16 years the banked pension is about £15,319 a year, roughly £1,277 a month. Reach the 20 year mark and it is about £19,149 a year, near £1,596 a month. That 20 year figure matters for a second reason, because it is also the point where the Early Departure Payment can open if you are at least 40, which we come to below.

Keep going and the pot keeps growing in a straight line on these flat numbers. By 25 years the annual pension is about £23,936, by 30 years about £28,723, and by a long 35 year career about £33,511 a year, close to £2,793 a month. Each extra year is adding a little over 2 percent of pay, which is why the line climbs so evenly. There is no maximum, so unlike the legacy schemes you are not working towards a cap.

None of those figures include an automatic lump sum, because AFPS 15 does not pay one. If you wanted tax free cash you would commute part of the pension, which trims the annual income in return for a one off sum. The next section explains exactly how that trade works, and the calculator lets you slide the commutation amount up and down to see both numbers move together for your own pay and service.

Lump sum & commutation

This is where AFPS 15 surprises people who served under the old schemes. AFPS 15 pays no automatic lump sum. AFPS 75 and AFPS 05 handed you a tax free lump worth three times your pension without you doing anything. AFPS 15 does not. If you want tax free cash, you have to create it yourself by commuting.

Commuting means giving up part of your annual pension in exchange for a one off tax free sum. The rate is fixed and scheme wide: £12 of lump sum for every £1 of yearly pension you surrender, often written as a factor of about 12 to 1. You can commute up to 25 percent of your pension, which is the HMRC limit on tax free cash and sits inside the wider lump sum allowance that caps tax-free cash across all your pensions. The arithmetic is plain. Decide the slice of pension to give up, multiply it by 12, and that is your lump sum; your remaining pension is what is left after the slice is removed.

The catch is that the reduction is permanent. You are not borrowing against next year, you are lowering your guaranteed income for the rest of your life in return for cash today. On the £45,000 example, commuting the full quarter at 20 years turns roughly £19,149 of annual pension into about £14,362 a year plus a lump sum near £57,447. Whether that is a good deal depends on how long you expect to draw the pension, your tax position, and what the cash is for. For some it clears a mortgage or funds a clean break into civvy street; for others the lifetime income is worth more than the lump. There is no single right answer, which is exactly why it is offered as a choice rather than done for you.

Is it worth commuting?

Weigh the tax-free cash against the income you give up over retirement.

Early Departure Payment (EDP 15)

The normal pension age for AFPS 15 is 60, and if you leave before then the deferred pension is paid at your State Pension age, which is a long wait for someone leaving the forces in their forties. The Early Departure Payment is the bridge across that gap. It is not the pension itself; it is a separate income and lump sum that keeps money coming in between leaving service and the day the pension proper begins.

To qualify you must leave at age 40 or over, and before 60, with at least 20 years of qualifying service. That combination is known as the 20/40 point. Meet it and the EDP pays two things. First, a tax free lump sum of 2.25 times your preserved pension. Second, a monthly income worth 34 percent of that pension at the 20 year mark, increased by 0.85 percent of the pension for every extra year you served beyond 20. So the longer you stay past 20, the larger the EDP income grows.

On the £45,000 illustration, a member leaving at the 20/40 point has a preserved pension of about £19,149. That gives an EDP lump sum near £43,085 and a monthly EDP income of roughly £543. Serve to 30 years and the preserved pension of about £28,723 lifts the income fraction to 42.5 percent, an EDP income near £1,017 a month plus a larger lump. The EDP income is flat until age 55, then it is uplifted for the inflation since you left and rises with CPI after that. When you finally reach your pension age, the EDP income stops and your actual AFPS 15 pension takes over.

Work out your EDP

See your EDP lump sum and monthly income for leaving before pension age.

When you can actually draw an AFPS 15 pension

The headline rule has two halves: normal pension age is 60, and a deferred pension is paid at your State Pension age. Serve to 60 and your AFPS 15 pension is paid in full straight away. Leave before 60, as most people do, and it waits until your State Pension age, when it is paid on top of the State Pension itself. That deferred age is a real change from the legacy schemes, where a preserved pension arrived at a fixed 60 or 65, and it is why planning around AFPS 15 means knowing your own State Pension age rather than assuming a round figure.

If you leave before 60 with at least two years of service, you do not lose the pension; it becomes a deferred pension that is held for you and paid when you reach your State Pension age. In the meantime it is revalued so it keeps its value. You can choose to bring a deferred pension into payment early, from age 55, but if you do it is permanently reduced to reflect the extra years it will be paid for. That early access reduction is the trade for getting the money sooner.

Put the pieces together and a typical early leaver's timeline looks like this. You leave at, say, 42 after a 22 year career. If you have hit the 20/40 point, the EDP income and lump tide you over. The preserved pension sits and revalues in the background. When you reach your State Pension age, the EDP stops and the AFPS 15 pension begins, rising with CPI thereafter for the rest of your life. Knowing which payment is active at which age is the key to planning your transition.

What to do next

A good plan starts with knowing the numbers, then checking them against the official record. Here is a sensible order of work for an AFPS 15 member.

Get your bearings

- Run the calculator above with your current pensionable pay and your years of service for an AFPS 15 estimate.

- Read your annual benefit statement, which shows the pensionable pay and figures the scheme is actually using for you.

- Note your State Pension age, because that is when a deferred AFPS 15 pension is paid if you leave before the normal pension age of 60.

Then go deeper

Frequently asked questions

How is an AFPS 15 pension calculated?

Does AFPS 15 pay a tax-free lump sum?

When can I take my AFPS 15 pension?

What is EDP 15 and who qualifies?

Am I in AFPS 15?

How much is an AFPS 15 pension worth after 20 years?

Why does my old pension still feel like final salary?

What stops my early pension years losing value before I retire?

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · AFPS 15 scheme guidance · GAD factors · Veterans UK · Forces Pension Society. Independent and not affiliated with the MOD or Veterans UK.