Armed Forces Pension Divorce Calculator

Estimate the value of an armed forces pension for a pension sharing order on divorce, and understand how AFPS benefits are split.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Pension on Divorce estimate is worked out

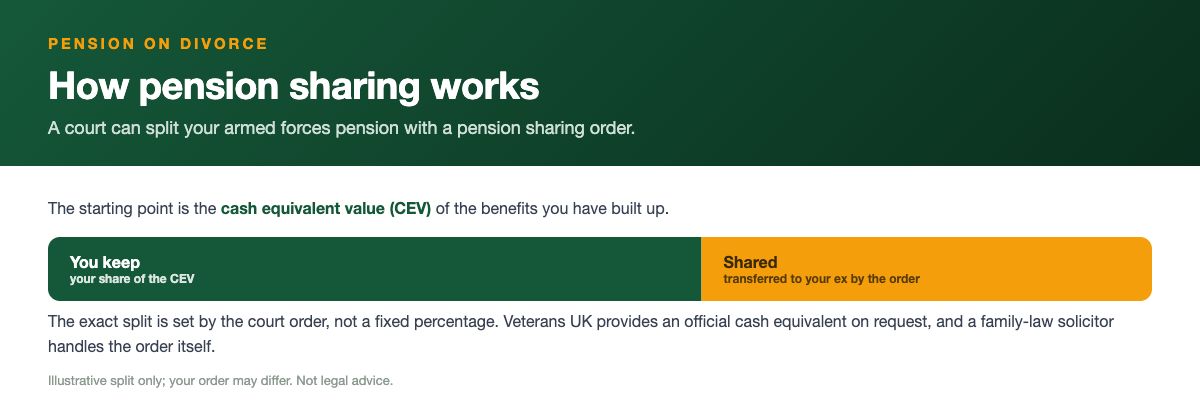

On divorce, the courts can make a pension sharing orderthat transfers part of one spouse's armed forces pension to the other. The starting point is the cash equivalent value of the benefits built up.

This estimate helps you understand the scale of the pension before formal valuations. Veterans UK provide an official cash equivalent on request, and a family-law solicitor handles the order itself.

How divorce affects an armed forces pension

When a marriage or civil partnership ends, the armed forces pension is treated as a financial asset that the court can divide, in the same way as a house, savings, or investments. For many serving personnel and veterans it is the single largest asset they own, often worth more than the family home, so it cannot simply be ignored when a settlement is worked out. That surprises a lot of people, because a pension does not feel like money in the bank, but the courts in England, Wales, Scotland, and Northern Ireland all have powers to take it into account. The key point is that the whole value built up under AFPS 75, AFPS 05, or AFPS 15 is on the table, not just the slice earned during the marriage, although how much of it is shared is a matter for negotiation and the court.

This calculator gives you an early, rough estimate of what an armed forces pension is broadly worth and how a share of it might look. It is a starting point for understanding your position before you instruct solicitors, not a formal valuation and not financial advice. The figures it produces are illustrative and based on the published scheme rules and constants on this site. They will not match, to the penny, the official cash equivalent value that Veterans UK will provide later in the process. Treat the estimate as a way to frame sensible questions, so you walk into your first legal meeting already understanding the shape of the asset rather than hearing about it cold.

One thing worth saying up front: divorce does not automatically split a pension. Nothing happens to the pension at all unless a court order specifically directs it, or unless the parties agree to offset its value against other assets. A serving member can continue to build AFPS 15 benefits throughout the process, and a veteran already drawing a pension keeps receiving it, until and unless an order takes effect. Understanding that the pension is divided only by a deliberate legal step, and only in the way the order specifies, is the foundation for everything else on this page.

What a pension sharing order is

A pension sharing order is the main tool the courts use to divide a pension on divorce. It works by transferring a fixed percentage of the member's pension value to the former spouse, who then holds it in their own right. The percentage is set by the court or agreed between the parties, and it is applied to the cash equivalent value of the pension at a particular date. For example, an order might direct that 30% of the member's AFPS value is moved across to the ex partner. Once it takes effect, the member's own pension is permanently reduced by that share, and the former spouse gains a separate, independent entitlement.

Under the armed forces schemes, the former spouse usually becomes a pension credit member of the scheme. In plain terms, they get their own pot inside the AFPS arrangement, separate from the serving member or veteran, with its own rules about when it can be drawn. This is a clean break for the pension itself: after the share is implemented, the two pensions go their separate ways and neither party's later choices affect the other. That independence is exactly why a pension sharing order is so often preferred over older approaches, because it lets both people move on without a financial thread tying them together for decades.

Pension sharing is not the only option. The court can also use pension attachment, sometimes called earmarking, where a slice of the pension is paid to the former spouse only when the member starts drawing it, or offsetting, where the member keeps the whole pension but gives up other assets such as a larger share of the house to balance things out. Each route has trade-offs around timing, certainty, and tax, and the right choice depends on the couple's wider finances. This calculator focuses on the sharing route because it is the most common way an armed forces pension is split, but you should know the alternatives exist.

The cash equivalent transfer value (CETV)

At the centre of any pension division is the cash equivalent transfer value, usually shortened to CETV or simply the cash equivalent. It is a single capital figure that represents what the pension is worth today, expressed as a lump sum, even though the benefit is actually a stream of income payable for life from pension age. The court uses this figure to understand the size of the asset and to set the percentage in a pension sharing order. For armed forces personnel, the official CETV is calculated by Veterans UK using factors set by the Government Actuary's Department, and it reflects the specific scheme you are in, your service, your age, and your normal pension age.

It helps to understand why an AFPS cash equivalent can look large. A defined benefit pension such as AFPS 75, AFPS 05, or AFPS 15 promises a guaranteed, inflation linked income for the rest of your life, plus benefits for survivors, and replacing that promise on the open market would be very expensive. So the capital value behind even a modest looking annual pension is often substantial. That is why the pension frequently dwarfs the other assets in a service divorce, and why getting an accurate cash equivalent matters so much. A small percentage error on a large number is a large amount of money in real terms.

Our calculator estimates the broad value of the pension using the scheme accrual rules: for AFPS 05 that is 1/70th of final pay for each year up to a maximum of 57%, with an automatic tax-free lump sum of 3 times the annual pension; for AFPS 15 it is 1/47th of pensionable pay banked each year and revalued for inflation. From there you can see the rough scale of the benefit a share would be taken from. What the calculator cannot do is reproduce the exact GAD factors, your precise service record, or any McCloud remedy adjustments, so the formal CETV from Veterans UK is the figure the court will actually rely on.

How the AFPS benefits are actually split

When a pension sharing order is implemented, the scheme administrator applies the ordered percentage to the cash equivalent and creates a pension credit for the former spouse. The member's benefits are then reduced by a corresponding pension debit, which is recorded against their record and carried forward to retirement. So if an order shares 40% of the value, the member keeps a pension built on the remaining 60%, and the former spouse holds the 40% as their own pension credit. Both halves are revalued and increased over time under the scheme rules, so neither is frozen at the divorce date.

The split applies to the core pension benefits, and in the final salary schemes that includes the automatic tax-free lump sum that comes with them. Under AFPS 75 and AFPS 05 the pension carries an automatic lump sum of 3 times the annual pension, so when the pension value is shared, that lump sum value is part of what is being divided. AFPS 15 has no automatic lump sum, although a member can commute up to 25% of the pension to a lump sum at the fixed rate of about 12 to 1, and the underlying pension value is what the cash equivalent captures. The order works on the capital value, so the mechanics differ between schemes even though the principle is the same.

Survivor and dependant benefits are handled within this framework too. Once a couple are divorced, an ex spouse is no longer entitled to the scheme's automatic widow, widower, or surviving partner pension, because that protection is tied to the relationship. The pension sharing order is the mechanism that gives the former spouse a secure entitlement of their own to replace what they lose on divorce. This is one of the strongest reasons to formalise the position with an order rather than relying on an informal understanding, because an informal arrangement gives the former spouse no protected right to anything at all.

The legal process, step by step

The process usually begins once divorce proceedings are under way and both parties are required to disclose their finances. The serving member or veteran requests a cash equivalent value from Veterans UK, and both sides set out all of their assets on the standard financial disclosure form used by the court. The pension cash equivalent goes onto that form alongside everything else, and it is at this stage that the true scale of an armed forces pension usually becomes clear. Getting the request in early matters, because the cash equivalent can take time to produce and the rest of the negotiation often waits on it.

Once the values are known, the parties, with their solicitors and often a pensions actuary, work out a fair division of all the assets together, not the pension in isolation. They might agree a pension sharing percentage, or decide to offset the pension against the house, or use a mix. If they reach agreement, it is written into a consent order and sent to the court for approval. If they cannot agree, the court decides, and in heavier cases a specialist pensions report, known as a pension on divorce expert report, is commissioned to advise on a fair split. The aim throughout is fairness across the whole financial picture, balancing income in retirement against capital needed now.

After the court makes a pension sharing order, it does not take effect immediately. There is an implementation period during which the scheme administrator puts the share into place, sets up the former spouse's pension credit, and applies the debit to the member's record. Only at the end of that period is the division final and the clean break for the pension complete. The timescales in Scotland differ in some respects from England, Wales, and Northern Ireland, particularly around how much of the pension is treated as matrimonial, which is another reason to take advice that fits the jurisdiction you are divorcing in.

A worked example (illustrative only)

Here is an illustrative example to show the mechanics, using only the figures published on this site. Imagine a veteran in AFPS 05 with a preserved annual pension worth around 12,000 pounds a year, which carries an automatic tax-free lump sum of 3 times that pension, so 36,000 pounds, under the scheme's standard 3 times rule. The capital value behind that guaranteed, inflation linked income for life is what the cash equivalent would capture, and it would be considerably more than the annual figure suggests because it represents decades of future payments. This example is for illustration of the method only and is not a real valuation.

Suppose the court approves a pension sharing order of 30%. The scheme would create a pension credit for the former spouse worth 30% of the cash equivalent, and apply a matching 30% debit to the veteran's record. In rough terms the veteran's own pension would then be built on the remaining 70% of the value, reducing the income they eventually draw, while the former spouse holds their 30% credit as an independent pension to draw under the scheme rules. Both portions continue to be revalued and increased over time, so the shares move with inflation rather than standing still.

The numbers above are deliberately round and the percentage is just an illustration. Your real position depends on your exact scheme, your length of service, your normal pension age, whether you are affected by the McCloud remedy for service between 1 April 2015 and 31 March 2022, and the GAD factors in force when the cash equivalent is calculated. Use the calculator to get a feel for the scale of your own benefit, then rely on the official cash equivalent and proper legal and actuarial advice for the figures that actually go before the court.

What this estimate gives you versus a formal Veterans UK valuation

It is important to be clear about what this tool is and is not. The calculator produces an estimate based on the published AFPS accrual rules and the constants on this site. It is a free, fast way to understand the rough size of the pension and how a percentage share would look, so you can have an informed conversation with your solicitor. It is not regulated financial advice, it is not a legal valuation, and it is not affiliated with the Ministry of Defence, Veterans UK, or JPAC. We are an independent education site, and the numbers here are for orientation, not for filing with a court.

The figure the court relies on is the official cash equivalent from Veterans UK. That valuation uses your individual service record, your exact dates, your scheme membership, your normal pension age, and the current Government Actuary's Department factors, none of which a public calculator can fully reproduce. Serving members request their pension forecast and cash equivalent using the appropriate Veterans UK form, and preserved members do the same for a deferred pension. Always get that official figure before you agree anything, because it is the number with authority behind it.

Think of it like this: our estimate tells you whether you are dealing with tens of thousands or hundreds of thousands of pounds, and helps you spot if something looks badly out of line. The Veterans UK valuation gives you the precise, court ready figure. You need both, in that order. Starting with the estimate means you arrive at the formal stage already understanding the asset, which makes the whole process faster and cheaper, and reduces the risk of being talked into a settlement that does not reflect what the pension is really worth.

Common mistakes, tax, and next steps

The most common and costly mistake is leaving the pension out of the settlement altogether, or swapping it away too cheaply for the house. People understandably want to keep the family home, but giving up a large, guaranteed, inflation linked pension to do so can leave one party comfortable now and poor in retirement. Another frequent error is using an out of date or guessed pension value rather than the official cash equivalent, and a third is failing to get a consent order at all, relying instead on a handshake agreement that gives the former spouse no protected entitlement and can unravel years later. In a marriage where one partner deployed and moved repeatedly while the other built the home life, the pension often represents shared effort, and treating it as solely the serving member's can be deeply unfair.

On tax, the headline points are straightforward but worth knowing. A pension sharing order itself does not trigger an immediate tax charge; it moves pension value across, and each party is then taxed in the normal way on the pension income they eventually receive, as income at their own rate when it is paid. The automatic tax-free lump sums under AFPS 75 and AFPS 05 keep their tax-free status within the usual HMRC rules. Where a settlement uses offsetting instead, you are trading a pension against assets that may carry their own tax treatment, such as capital gains on a property, so the comparison is rarely like for like. This is exactly the kind of judgement where professional advice earns its fee.

As for next steps: use the calculator to size up the pension, then request your official cash equivalent from Veterans UK so you have a figure with authority. Take legal advice from a family solicitor who understands armed forces pensions, and in anything other than a simple case, get a pensions actuary or pension on divorce expert involved, because the right split is rarely a straight 50/50 of the headline number. The Forces Pension Society and similar bodies can also help you understand your scheme. The cost of good advice is small against the size of the asset, and getting the division right is one of the most important financial decisions you will make around leaving service or retirement.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Armed forces pension on divorce

Pension sharing orders, the cash equivalent value, and how AFPS is split.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.