Medical Discharge & Ill-Health Pension Calculator

Estimate your armed forces ill-health pension following a medical discharge. Your tier and service shape the enhanced pension and lump sum.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Medical Discharge estimate is worked out

A medical discharge can give an enhanced ill-health pension. The amount depends on the tier your condition is assessed at and on the service you have completed.

Higher tiers add notional extra service to boost the pension and lump sum. This estimate is a guide only, and your formal award comes from Veterans UK after a medical assessment.

What a medical discharge pension actually is

A medical discharge is when the service decides you can no longer do your job because of a permanent or long-term medical condition, and you are released before you would otherwise have left. When that happens the Armed Forces Pension Scheme has its own ill-health provisions that sit separately from the ordinary rules. The point of these provisions is straightforward: you did not choose to leave early, so the scheme does not simply hand you the small pension your short service would normally buy. Instead it can pay an enhanced pension, sometimes with a tax-free lump sum, and it can pay it immediately rather than making you wait until your normal pension age.

Which scheme you are in decides the detail. If your service runs from before April 2015 you may have benefits in AFPS 75 or AFPS 05, the older final-salary schemes, and from 1 April 2022 everyone still serving builds AFPS 15, the career-average scheme. Most people being medically discharged today have a mix: a legacy slice and an AFPS 15 slice, with the McCloud remedy deciding how the 1 April 2015 to 31 March 2022 period is treated. The ill-health rules apply across all of them, but the size of the award and the way it is worked out differ by scheme.

The headline thing to understand is that an ill-health award is not the same as an injury compensation payment. The pension recognises the career you have lost. A separate scheme deals with the injury or illness itself: the Armed Forces Compensation Scheme for service on or after 6 April 2005, or the War Pension Scheme for service before that date. The two can be paid together, and we explain the difference further down, because people often confuse them and end up expecting one figure when two quite different things are in play. Use this calculator to get a feel for the size of the pension at each tier and how enhanced service changes it, but treat every figure as an illustrative estimate; the only binding number is the one Veterans UK works out from your record.

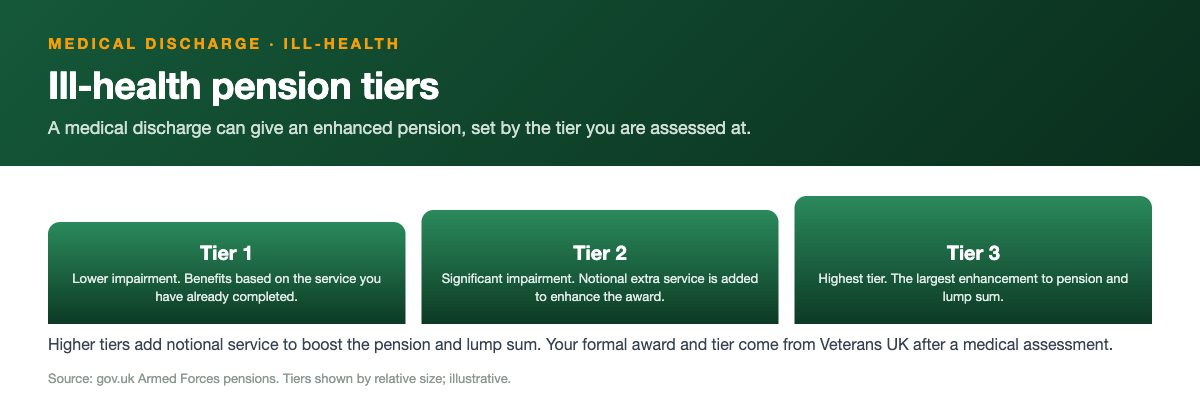

The three-tier system explained

Ill-health benefits are split into tiers, and the tier is the single most important figure in the whole calculation because it decides whether you get a pension at all, whether it is enhanced, and whether it is paid now. In broad terms there are three tiers. The lowest tier is for members whose ability to do paid work generally is least affected; the middle and top tiers are for those whose capacity for any future employment is more seriously and more permanently reduced. The worse and more permanent the impact on your ability to earn a living, the higher the tier and the more generous the award.

At the lowest tier a member is usually treated much like any other early leaver: you keep the pension you have actually built up, preserved until your scheme's preserved pension age, rather than receiving an enhanced immediate payment. The middle tier typically brings an immediate pension based on the service you have genuinely completed, paid straight away rather than deferred. The top tier is where the real enhancement happens, because the scheme credits you with extra notional service on top of what you served, on the basis that your condition has cut your career short and removed your chance to build the pension you otherwise would have.

Because the tier drives everything, the calculator lets you model each one so you can see the gap between them. That gap is often large, which is exactly why the tiering decision is so heavily evidenced and so often the thing members query. If you think your tier is wrong, that is the number to challenge first, not the arithmetic that follows from it. Tiers are decided on medical grounds, not on rank or trade, so two people on the same pay and length of service can land at different tiers because their conditions affect their future capacity for work differently.

Enhanced service and how the top tier boosts your pension

The most valuable feature of a higher-tier ill-health award is enhanced service, sometimes called notional service. The scheme adds extra years to your reckonable service that you never actually served, then works the pension out on the larger figure. The logic is fair: a medical discharge has taken away the rest of your career, so the scheme partly puts back the pension you would have earned had you been able to carry on.

How that enhancement feeds through depends on the scheme. In a final-salary scheme like AFPS 05, more years simply means a bigger fraction of your final pensionable pay, because the pension is your pay multiplied by your years and divided by 70, up to the scheme maximum of 57 per cent. Add enhanced years and the fraction climbs. In the career-average AFPS 15 scheme the pension is built from 1/47th of pensionable pay banked each year, so enhanced service works by crediting additional accrual on top of the pot you have already built, lifting the deferred pension on which the ill-health benefit and any survivor benefit are based.

This is why two members with identical real service can end up with very different pensions: the one placed in the top tier gets the enhancement, the one in a lower tier does not. The enhancement can be worth more than the pension your actual service bought, which is why the tier decision matters so much more than most people realise when they first read their paperwork. The precise number of enhanced years is fixed by the scheme rules and your circumstances and can only be confirmed by Veterans UK, so treat the on-screen enhancement as an illustration of the shape of the boost rather than a quoted entitlement.

The lump sum and what is tax-free

Whether you receive a lump sum, and how big it is, depends on the scheme the benefit is paid from. In the final-salary schemes a lump sum comes automatically. AFPS 75 and AFPS 05 both pay a tax-free lump sum of three times the annual pension, so a higher pension, including one lifted by enhanced service, also produces a bigger lump sum. You do not have to do anything to trigger it; it is built into the award.

AFPS 15 is different. The career-average scheme pays no automatic lump sum at all. If you want tax-free cash from an AFPS 15 ill-health pension you create it by commuting, that is by giving up some annual pension in exchange for a one-off sum. The fixed rate is 12 to 1, so every 1 pound of yearly pension you surrender buys 12 pounds of lump sum, and HMRC caps how much you can commute at 25 per cent of the pension value. That is a permanent trade: the income you give up does not come back, so think hard before commuting an ill-health pension you may rely on for decades.

Lump sums paid under these schemes are tax-free, which is one of the genuine advantages of the system, while the ongoing pension is taxable income in the normal way once it is in payment. If your award spans more than one scheme, you can end up with an automatic lump sum from the legacy part and a separate commutation decision on the AFPS 15 part, and the calculator keeps these apart so you can see where each pound is coming from.

How Veterans UK assesses your tier

The tier is a medical judgement, not a sum you can do yourself, and it is made on the evidence in your service medical record and the reports prepared around your discharge. Veterans UK, which administers the scheme on behalf of the Ministry of Defence, looks at how your condition affects your capacity for employment, how permanent it is, and how far it limits the work you could reasonably be expected to do in future. The more severe and the more lasting the effect on your ability to earn, the higher the tier.

It helps to understand that this assessment is about future earning capacity, not about how unpleasant or painful a condition is day to day. A condition can be genuinely debilitating yet still place you at a lower tier if the assessors conclude you could still undertake some form of paid work. That can feel harsh, and it is one of the most common sources of dispute, which is exactly why getting full, accurate medical evidence in front of the assessors before the decision is made is so important.

If you disagree with the tier you are given, there is a route to challenge it, and the tier is almost always the right thing to challenge because it changes everything downstream. The figures this calculator produces are only ever as good as the tier you select, so the assessment is the real battleground, not the arithmetic. This site is independent and cannot assess your tier; for your tier and your actual award you need an official forecast from Veterans UK, requested on form 12 if you are still serving or form 14 if your pension is already preserved.

Ill-health pension versus Armed Forces Compensation Scheme

This is the distinction that trips most people up, so it is worth being clear. The ill-health pension is part of your pension scheme. It is paid because your career ended early and it is worked out from your pay, your service and your tier. The Armed Forces Compensation Scheme, the AFCS, is a completely separate scheme that pays for the injury or illness itself where that was caused or made worse by service, regardless of how long you served.

Because they do different jobs, they can be paid at the same time, and for many medically discharged people both are in play. The AFCS can pay a tax-free lump sum for the injury and, for more serious cases, an ongoing Guaranteed Income Payment. None of that is calculated here, and none of it changes the way your ill-health pension is worked out. They are assessed on different criteria by different processes, so a strong AFCS claim does not automatically mean a high pension tier, and a high tier does not guarantee a large AFCS award.

Keeping the two apart matters when you are working out what you will actually have to live on. Your ill-health pension is taxable income; an AFCS Guaranteed Income Payment is tax-free. Adding the wrong figures together, or assuming one number covers both, is a frequent and expensive mistake. This calculator deals only with the pension side, so if you are pursuing an AFCS claim, treat it as a separate exercise with its own evidence and its own timetable.

A worked example (illustrative)

Here is an illustrative example using only the scheme figures, to show how the pieces fit. It is not a quote. Take a member in AFPS 05 with final pensionable pay of 30,000 pounds who has actually served 16 years, and who is placed in a tier that pays an immediate pension on completed service. The pension is 30,000 multiplied by 16, divided by 70, which is about 6,857 pounds a year. The automatic tax-free lump sum is three times that, about 20,571 pounds. That is the award based on real service alone.

Now suppose the same member is placed in the top tier and the scheme enhances their service, so the pension is worked out as if they had served longer. If enhancement lifted the reckonable figure used in the sum to, say, 24 years, the pension would be 30,000 multiplied by 24, divided by 70, which is about 10,286 pounds a year, with a lump sum of three times that, about 30,857 pounds. The exact number of enhanced years is set by the scheme rules and is not something you choose, so treat the 24 here purely as an illustration of how the enhancement lifts the figures.

The point of the comparison is the size of the jump. Moving up a tier did not just add a little; it added roughly half as much pension again and a matching increase in the lump sum, all from the same pay and the same real service. For an AFPS 15 member the mechanics differ, because there is no automatic lump sum and the pension is built from 1/47th of pay each year plus any enhanced accrual, but the principle is identical: a higher tier with enhancement produces a materially larger pension than completed service alone.

How to check your own position and common mistakes

Start by working out which scheme or schemes your benefits sit in, because that decides whether a lump sum is automatic, how enhancement feeds through, and when the pension is paid. If you were serving before April 2015 you will have a legacy element, and the McCloud remedy means the 1 April 2015 to 31 March 2022 period is dealt with through a Remediable Service Statement that lets eligible members choose legacy or AFPS 15 benefits for those years. Get that statement and read it, because it changes the figures.

Then look hard at the tier, because the tier is where the money is decided. Make sure the medical evidence in front of the assessors is complete and current, since the assessment turns on your future capacity for work. If the tier looks wrong, challenge the tier first; the arithmetic that follows is only as good as that decision.

The common mistakes are predictable. People confuse the ill-health pension with the AFCS award and double-count or expect the wrong total. They assume AFPS 15 pays an automatic lump sum, which it does not. They commute AFPS 15 pension for cash without realising the income loss is permanent. They forget that the ongoing pension is taxable while the lump sums are tax-free. And they treat an online estimate, including this one, as a firm figure rather than a guide. To avoid all of that, get an official forecast from Veterans UK, requested on form 12 if you are still serving or form 14 if your pension is preserved, and remember the Forces Pension Society can help you understand a tiering decision and decide whether to challenge it.

Tax treatment and your next steps

The tax treatment is simple to state and easy to get wrong. The tax-free lump sums under these schemes, whether the automatic three-times-pension lump sum from a final-salary scheme or a sum you create by commuting AFPS 15 pension, are paid free of income tax. The ongoing ill-health pension is taxable income and is taxed under PAYE like any other pension once it is in payment. Pensions already in payment also rise each year with inflation; from April 2026 the increase is 3.8 per cent in line with CPI.

Because the pension is taxable, the figure you can actually spend each month is lower than the gross pension this calculator shows. If you have other income, the pension stacks on top of it for tax purposes, which can push part of it into a higher band. That is worth modelling before you make any irreversible choice, especially commutation, because giving up taxable income to take a tax-free lump sum can be sensible or costly depending on your wider position.

Your next step is to get the binding numbers and proper guidance. Request an official forecast from Veterans UK, on form 12 while serving or form 14 once preserved, obtain your Remediable Service Statement so you know how the McCloud period is treated, and if you are also making an AFCS claim, keep it separate and track it on its own. This site is independent and provides estimates, not regulated financial advice, and it is not affiliated with the MOD, Veterans UK or JPAC. For a decision as significant as a medical discharge, use the calculator to understand how your benefits are worked out, then confirm the detail with Veterans UK and, if a large sum or a commutation choice is involved, take advice from a regulated financial adviser who knows the armed forces schemes.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Medical discharge & ill-health pensions

How the tiers work and what the enhancement adds to your award.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.