Army Pension Calculator

Work out your British Army pension and lump sum across AFPS 75, 05 and 15. Pick the scheme that matches when you joined.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Army estimate is worked out

Your Army pension follows the Armed Forces Pension Scheme that applied while you served. Pick the scheme that matches when you joined, most careers touch more than one.

AFPS 75 is a final-salary scheme. Your pension is a share of representative pay for your rank, building to a maximum of 48.5% over a full career, 34 years for officers, 37 for other ranks, with an automatic tax-free lump sum of three times the annual pension.

AFPS 05 is also final-salary, building 1/70th of your final pensionable pay for each year served, up to about 57% of pay. It pays an automatic tax-free lump sum of three times your pension and can include an Early Departure Payment if you leave early with enough service.

AFPS 15 is a Career Average Revalued Earnings (CARE) scheme. It adds 1/47th of your current pensionable pay each year, revalued for inflation, rather than using a final salary. There is no automatic lump sum, so you can commute up to 25% of your pension for tax-free cash at a fixed rate of £12 per £1 of yearly pension given up.

How your Army pension actually works

The British Army does not run a single pension scheme. It runs three, and which one or which mix you sit in comes down to when you joined and when you served. The three schemes are AFPS 75, the original 1975 final-salary scheme, AFPS 05, the 2005 final-salary scheme, and AFPS 15, the career average scheme that every serving soldier now builds. This calculator lets you model each of them, because most soldiers with a full career touch more than one. Pick the scheme that matches your service and the tool does the sums on the same rules the Ministry of Defence uses.

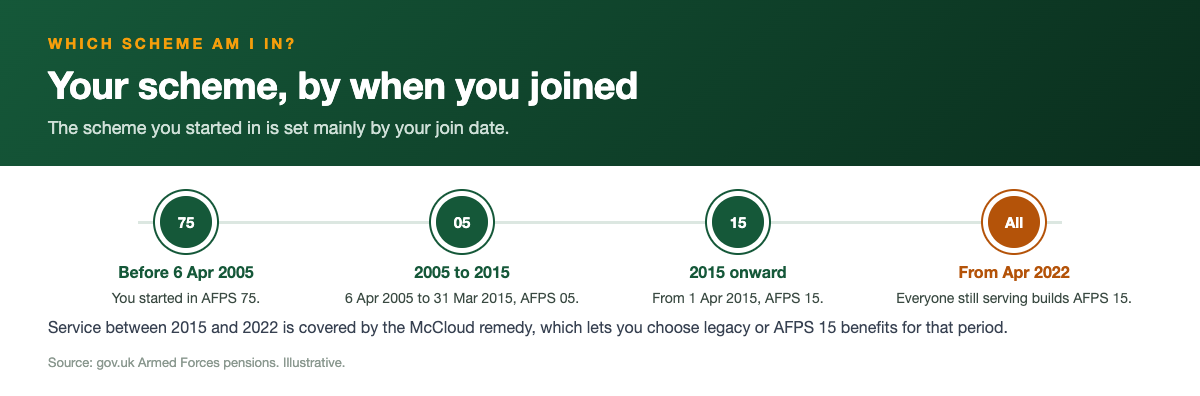

If you joined the Army between 1 April 1975 and 5 April 2005 you were enrolled in AFPS 75. If you joined between 6 April 2005 and 31 March 2015 you were in AFPS 05. Anyone who joined from 1 April 2015 went straight into AFPS 15. That sounds tidy, but very few long-serving soldiers stayed in one scheme for their whole career. The McCloud remedy moved affected legacy members into AFPS 15 on 1 April 2022, so a Warrant Officer who enlisted in 2002 could have built AFPS 05 benefits, then AFPS 15 benefits, with a choice over the years in between. The calculator handles each block on its own rules so you can add them up.

The headline difference is how the pension is worked out. AFPS 75 and AFPS 05 are final-salary schemes, so your pension is driven by your pay and rank near the end of your service. AFPS 15 is a CARE scheme, short for Career Average Revalued Earnings, which banks a slice of each year's pay and revalues it for inflation rather than relying on your final salary. That distinction changes everything about who comes out ahead, which is why a quick rank and length-of-service estimate is worth running before you make any decision about staying in, signing off, or commuting for cash.

Picking your scheme by join date

Start with the date you attested or were commissioned. A join date of 1 April 1975 to 5 April 2005 puts you in AFPS 75. A join date of 6 April 2005 to 31 March 2015 puts you in AFPS 05. A join date from 1 April 2015 onward puts you in AFPS 15 from day one. These windows are not a matter of choice; they were set by the rules in force when you signed on, and the calculator uses them as the default starting point for each service.

The complication is the McCloud remedy period, which runs from 1 April 2015 to 31 March 2022. During those seven years the courts found that moving older members onto AFPS 15 while protecting those closer to retirement was age discrimination. The fix is that affected members, which includes most soldiers who were serving across that period, get to choose legacy benefits or AFPS 15 benefits for the remedy years, and they make that choice when the pension is actually paid, not now. From 1 April 2022 everyone builds AFPS 15, full stop, regardless of which scheme they started in.

So a realistic Army career might look like this. You join in 2009, build AFPS 05 to 31 March 2022, then build AFPS 15 from 1 April 2022 to discharge, with a remedy choice for the 2015 to 2022 slice. Your AFPS 05 service is a protected accrued right, linked to your final pay and rank when you leave, and your AFPS 15 service sits alongside it. To model your whole position, run the scheme that covers the bulk of your service first, then run the others to see the separate blocks. Each pension is paid under its own rules and at its own pension age.

Representative pay, rank and why the figure depends on it

On the final-salary schemes, rank and pay are the engine of your pension, but the two older schemes treat them differently. Under AFPS 75 the pension is based on the representative rate of pay for your final rank, not your actual salary, for ranks up to and including OF-6 and for all other ranks. Two soldiers who leave at the same rank with the same reckonable service normally get the same pension, because the scheme uses a standard pay rate for that rank rather than your individual pay slip. The calculator cannot hold the MOD's rank-by-rank representative pay tables, so it uses the pay you enter as a sensible proxy and tells you so on screen. To read the published figure for your own rank instead of an estimate, see the army pension chart by rank and years served.

AFPS 75 builds towards a maximum of 48.5% of representative pay at full reckonable service. Full service is 34 years for officers and 37 years for other ranks, and accrual is treated as building steadily towards that 48.5% ceiling across the maximum service window. Accrual starts from age 21 for officers and age 18 for other ranks. AFPS 05 works differently again: it accrues 1/70th of your final pensionable pay for each year of reckonable service, up to a maximum of about 57% of final pay reached at 40 years. Here your actual final pay does the work, so entering an accurate figure matters more.

AFPS 15 does not lean on your final salary at all. Each scheme year, which runs 1 April to 31 March, the MOD adds 1/47th of that year's pensionable earnings to a pension pot, and the pot is revalued each year so it keeps its real value. Because the in-service revaluation tracks earnings, entering your current pensionable pay gives a sound estimate of the whole pot when you multiply pay by years and divide by 47. That is why the AFPS 15 calculator asks for current pay rather than a true career average, which most soldiers could not work out from memory anyway.

Worked examples by length of service

These examples are illustrative only and use round figures to show the mechanics, not a promise of your actual award. They use the rates already set out: 48.5% over a full career for AFPS 75, 1/70th per year for AFPS 05, and 1/47th per year for AFPS 15. For an official figure you must go to Veterans UK, but these show how the numbers move with service length.

Take an AFPS 05 soldier leaving with 22 years of reckonable service on a final pensionable pay of 47,000 pounds a year. The annual pension is final pay multiplied by years and divided by 70, so 47,000 times 22 divided by 70, which is about 14,771 pounds a year. AFPS 05 then adds an automatic tax-free lump sum of three times the annual pension, so roughly 44,314 pounds of tax-free cash on top. Note that is well short of the 57% ceiling, which only arrives at 40 years of service, so staying longer keeps building the pension at the same 1/70th rate each year. The same 22-year point is set out under all three schemes on how much is an army pension after 22 years.

Now take an AFPS 15 soldier with 20 years of service on current pensionable pay of 47,000 pounds. The pot is broadly pay times years divided by 47, so 47,000 times 20 divided by 47, which is 20,000 pounds a year. AFPS 15 pays no automatic lump sum, but you can commute up to 25% of your pension for tax-free cash at a fixed rate of about 12 pounds of lump sum for every 1 pound of yearly pension given up. Commuting the full 25% of that 20,000 pound pension would surrender 5,000 pounds a year to raise roughly 60,000 pounds of tax-free cash, with the income reduction being permanent. Run your own pay and years through the calculator to see how the two schemes compare for your situation.

EDP, the Immediate Pension and resettlement

If you leave before pension age, what you get depends on the scheme. AFPS 75 has no Early Departure Payment. Instead it pays an Immediate Pension when you leave Regular Service at the right point: officers after 16 years from age 21, other ranks after 22 years from age 18. That pension is paid straight away with its 3 times lump sum, runs flat until age 55, then rises with CPI each year with all past inflation applied at 55. Miss the Immediate Pension point and your AFPS 75 pension is preserved, payable from 60 for service before 6 April 2006 and from 65 for service after that. A short career lands squarely in that preserved category: how much is an army pension after 6 years works the figures through under each scheme.

AFPS 05 and AFPS 15 use Early Departure Payments instead. On AFPS 05 you qualify for EDP if you leave at age 40 or over with at least 18 years of service. You get a tax-free lump sum of three times your preserved pension and a monthly income of around 50% of that preserved pension, flat until 55 then CPI-uprated. On AFPS 15 the EDP point is the 20/40 rule: leave on or after age 40 and before 60 with at least 20 years of Regular service. The AFPS 15 EDP pays a tax-free lump sum of 2.25 times your preserved pension, plus a monthly income of 34% of the deferred pension with an extra 0.85% of that pension for every year you served beyond 20.

These early-leaver benefits are separate from the State Pension and from any preserved pension that becomes payable later. EDP income is a bridge to pension age, not the pension itself, so when you reach the scheme's pension age your underlying pension still comes into payment. Resettlement Grants are a different, one-off payment for some leavers who do not qualify for an Immediate Pension or EDP, and they are not modelled in this calculator. The point to take away is that signing off a year or two short of an EDP or Immediate Pension trigger can cost a great deal, so it is always worth checking the exact dates before you commit.

The McCloud remedy and your Army pension

If you were serving across the remedy period of 1 April 2015 to 31 March 2022, McCloud almost certainly affects you. The remedy gives affected members a choice between their legacy scheme, AFPS 75 or AFPS 05, and AFPS 15 for those seven years, and you make that choice when your pension is paid rather than now. The MOD sets out your two options in a Remediable Service Statement, which compares the benefits each way so you can see which is worth more for your circumstances. You do not have to decide today, and you should not guess.

For most soldiers the practical effect is that your service splits into blocks. Anything before the remedy period stays in your original scheme as a protected accrued right. The remedy years become a choice. From 1 April 2022 everyone, with no exceptions, builds AFPS 15. Benefits built up in AFPS 75 or AFPS 05 before transition are protected and paid when they were always going to be paid, linked to your final pay and rank at the point you leave, not frozen at the 2015 or 2022 transition dates.

This calculator does not make the McCloud choice for you, because that decision needs your Remediable Service Statement and often a conversation with a regulated adviser. What it does do is let you model each scheme separately so you can get a feel for the scale of the difference. Run the legacy scheme for the remedy years, then run AFPS 15 for the same years, and you will see roughly how the two stack up. Treat that as orientation, then check it against your official statement before you choose.

How your pension is taxed and paid

The pension income itself is taxable as earned income through PAYE, the same as a salary, once it comes into payment. The lump sums are different. The automatic 3 times lump sum on AFPS 75 and AFPS 05, the tax-free cash you create by commuting on AFPS 15, and the EDP lump sums on both AFPS 05 and AFPS 15 are paid free of income tax under the rules for armed forces pensions. That tax-free status is one of the strongest features of the schemes, which is why the commutation decision on AFPS 15 deserves real thought rather than a snap choice.

Pensions in payment and preserved pensions are protected against inflation. They rise each year in line with the Consumer Prices Index, and the increase for April 2026 is 3.8%. AFPS 75 is the odd one out on timing: its Immediate Pension is held flat until age 55, then all the inflation that built up in the meantime is applied in one go, and CPI increases follow each year after that. AFPS 15 pots are revalued while you serve and then rise with CPI once deferred or in payment, so the real value is broadly protected throughout.

You need at least 2 years of qualifying service to earn any AFPS pension at all. Below that you get nothing, and no refund either, because the scheme is non-contributory, so the 2 year mark is an important early milestone. Beyond tax, remember that commuting pension for cash on AFPS 15 is a permanent reduction to your yearly income, and EDP income stops being topped up in the way the underlying pension is, so think about the long game, not just the cash you can see today.

How to check your own figure and what to do next

This is an independent education site. We are not affiliated with the MOD, Veterans UK or JPAC, and the numbers here are estimates to help you plan, not regulated financial advice or an official forecast. The calculator uses published scheme rates and a few documented simplifications, such as using the pay you enter as a proxy for AFPS 75 representative pay, so treat the output as a well-grounded ballpark rather than the final word. For anything that drives a real decision, get the official figure.

The official forecast comes from Veterans UK. Serving members request a pension forecast using form Pen Form 1, and members with a preserved pension use the preserved-pension forecast route; if you are affected by McCloud, your Remediable Service Statement sets out the legacy and AFPS 15 comparison for the remedy years. These statements use your actual service record, your real pensionable pay history and the correct representative pay tables, so they will be more precise than any public calculator can be. Keep them safe, because they are the basis for the choices you will make later.

A sensible order of play is to run this calculator first to understand how your pension is built up and the levers you control, then request your official forecast to confirm the figures, then, if you are weighing up commutation, an EDP exit or your McCloud choice, speak to a regulated financial adviser or the Forces Pension Society. Use our scheme-specific calculators for AFPS 75, AFPS 05 and AFPS 15, plus the EDP and commutation tools, to drill into each part of your award. The more of your own service you model, the fewer surprises you will have when the official paperwork lands.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Not sure which scheme you're in?

Find out whether you're on AFPS 75, 05 or 15 and how each builds up.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.