Preserved and deferred armed forces pension explained

If you leave the forces before your normal pension age without qualifying for an immediate pension or an Early Departure Payment, the pension you have earned is not lost; it is preserved. A preserved, or deferred, pension sits waiting for you, rising with inflation each year, until you reach the age at which you can claim it. This guide explains who gets one, when it becomes payable, how it keeps its value, and the one thing many veterans forget, that you usually have to claim it rather than wait for it to arrive.

Key takeaways

- Leave before pension age without an immediate pension or EDP and your benefits are preserved (deferred).

- You need at least two years' qualifying service for a preserved pension to exist.

- Service before 6 April 2006 is normally payable at 60; later AFPS 75 and 05 service at 65; AFPS 15 at State Pension age.

- The preserved pension is revalued each year in line with prices, so it keeps its buying power while you wait.

- On AFPS 75 and 05 a preserved tax-free lump sum (three times the pension) is paid alongside it.

- It is not paid automatically; you usually have to claim it from Veterans UK, so do not let it go unclaimed.

What a preserved pension is

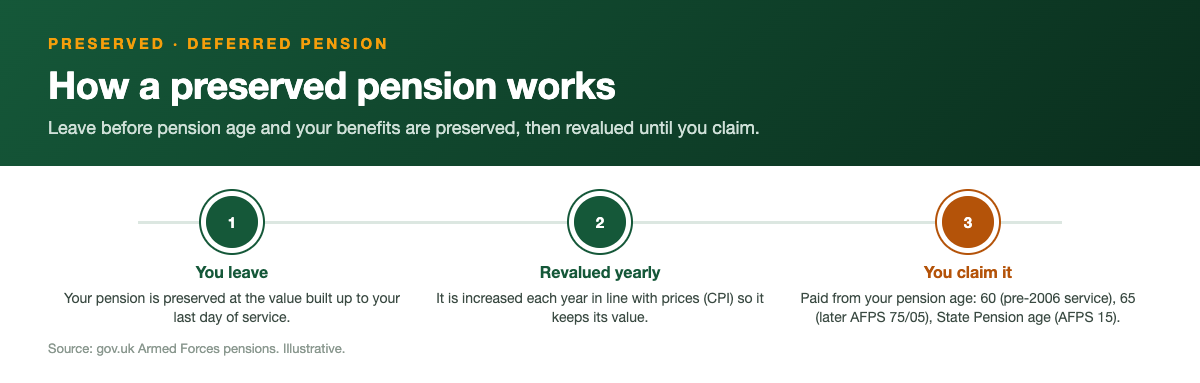

A preserved pension is the pension you leave behind when you go before your normal pension age, having served long enough to earn one but not long enough, or not at the right age, to draw it straight away. It is worked out from your scheme and your service at the date you left, and then set aside in your name until you can claim it.

You need at least two years of qualifying service for a preserved pension to exist at all. Below that you generally would not have a pension preserved, though other small leaving payments can apply, so two years is the threshold that turns service into a lasting benefit. We have worked the maths through just past that line, with the figures for three years' service and four years' service.

Think of it as service you have banked rather than money you have lost. You stop adding to it the day you leave, but what you accrued stays yours, calculated under the rules of whichever scheme the service sat in, and held in your name until the scheme's pension age for that service arrives.

Who ends up with a preserved pension

You typically end up with a preserved pension when you leave before your normal pension age and do not qualify for an immediate pension or an Early Departure Payment. That covers a great many people who serve a useful number of years and then move on to a civilian career well before 60.

The two-year qualifying threshold is the gateway. Serve at least two years and your benefits are preserved; leave with less and you would not have a preserved pension. There is no refund of contributions in that situation, because AFPS 75, 05 and 15 are all non-contributory and you paid nothing in to refund. AFPS 15 alone offers a route: if you have at least three months' service you can transfer the value out, provided you apply within six months of leaving.

It is common to hold a preserved pension at the same time as other benefits, for example an EDP from a later spell of service, or preserved slices from more than one scheme. Each slice keeps its own rules, so it is worth knowing exactly what you are holding rather than treating it as one lump.

When you can claim it

The age you can draw a preserved pension depends on when the service was built up. Service before 6 April 2006 is normally payable at age 60. AFPS 75 and AFPS 05 service from 6 April 2006 onward is normally payable at 65. AFPS 15 preserved benefits are payable at your State Pension age.

Because many careers straddle these dates, it is common to have one slice of preserved pension payable at 60 and another at 65, drawn at different times. That split matters for planning, so it is worth knowing which part of your service falls on which side of the 2006 line.

The practical upshot is that you may not be able to take everything at once. If part of your service is payable at 60 and part at 65, you can draw the earlier slice first and the later slice when you reach its age, so your preserved pension can arrive in stages rather than all on one birthday.

How it keeps its value

A preserved pension does not sit frozen. It is revalued every year in line with prices, broadly the same inflation measure used to uprate pensions already in payment, so its buying power is protected across what can be a very long wait. A pension preserved in your forties and drawn in your sixties will be a much larger cash figure by the time you claim it.

On the final-salary schemes, AFPS 75 and 05, a preserved tax-free lump sum of three times the annual pension is paid alongside the pension when it comes into payment. AFPS 15 has no automatic lump sum, so if you want tax-free cash you would commute part of the pension at the point you draw it.

Because the revaluation compounds year after year, the longer the wait the bigger the gap between the figure on your leaving statement and the figure you eventually draw. It is a mistake to plan using the old number; the preserved pension you left with at 45 will be a noticeably larger amount by the time you claim it at 65.

Tax and what you actually receive

A preserved pension is taxed as income once it comes into payment, like any other pension, so the figure on your forecast is gross. The lump sum that comes with AFPS 75 and 05 service is tax-free, and on AFPS 15 any cash you take by commuting part of the pension is tax-free as well.

Drawing a preserved pension does not stop you working or claiming your State Pension when the time comes; the AFPS benefit sits alongside both. For people drawing slices at different ages, it is worth thinking about how each one stacks with other income in that tax year.

None of this is tax advice. Where a preserved pension is large or you are drawing several income sources at once, a quick check with a regulated adviser can save more than it costs, particularly around the timing of when you take each slice.

Claiming it, and what to do

The single biggest risk with a preserved pension is forgetting it exists. It is usually not paid automatically when you reach the right age; you have to claim it, normally using form 14 to Veterans UK, ideally several months before you want it to start. Pensions do go unclaimed simply because people lose track of them over twenty or thirty years.

Keep a note of your scheme, your leaving date and your expected pension ages, and keep your contact details current with Veterans UK so they can reach you. Use the preserved pension calculator here to estimate the revalued value, then request an official forecast on form 14 before you rely on a figure. This site is independent and provides estimates, not regulated financial advice.

If you have lost track of an old preserved pension, you are not stuck; Veterans UK can trace it from your service details, and it is well worth the effort given how much a revalued pension can be worth after twenty or thirty years. The earlier you reconnect with the scheme and update your contact details, the less chance there is of the pension going unpaid simply because nobody could find you.

See your own numbers

Get your pension, lump sum and EDP in seconds.

Frequently asked questions

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk · GAD factors · Veterans UK · Forces Pension Society · MoneyHelper.