Preserved & Deferred Pension Calculator

Calculate a preserved (deferred) armed forces pension built up before you left service, and the index-linked value you can claim later.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Preserved Pension estimate is worked out

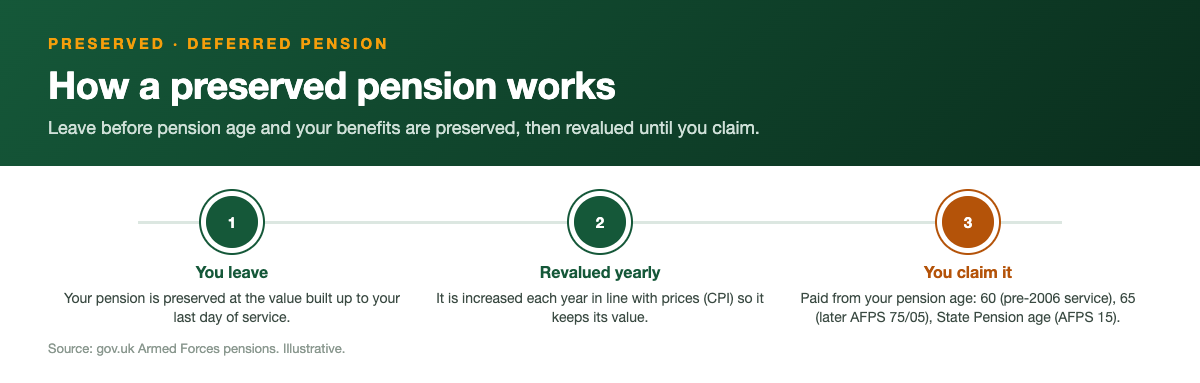

A preserved (deferred) pension is the benefit you leave behind when you go before pension age without taking an immediate pension. It is worked out from your scheme and service at the date you left.

The preserved value is revalued each year in line with inflation until you claim it, at 60 for service before April 2006, and at 65 for later AFPS 75 and 05 service.

What a preserved (deferred) pension is

A preserved pension, sometimes called a deferred pension, is the pension you have already earned but cannot draw yet. If you leave the Armed Forces before your scheme's normal pension age and you have served long enough to qualify for a pension, the benefits you have built up do not vanish. They are locked in, parked in the scheme, and paid to you in full when you reach the right age. The word preserved is the official term used in AFPS 75 and AFPS 05; the word deferred is the equivalent used in AFPS 15. They describe the same idea: pension earned now, paid later.

The key thing to understand is that a preserved pension is not lost money and it is not frozen money. It is yours, it is protected against inflation while you wait, and it cannot be taken away. The only catch is timing. You give up early access in exchange for keeping the benefit, and in the meantime the scheme uprates it each year so its buying power holds up. This calculator estimates the size of that preserved pension and shows you the age at which you can claim it.

To earn any pension at all you need at least two years of qualifying service. Serve less than that and there is no preserved pension, and no refund either, because the armed forces schemes are non-contributory. On AFPS 15 you can instead transfer the value out if you apply within six months of leaving. Once you cross the two-year line, a preserved pension is created automatically when you leave, and it sits in the background until your claim age arrives. Most people who serve a meaningful length of time and leave before pension age end up with exactly this: a preserved pension waiting for them. For what that is actually worth after a short engagement, see how much is an army pension after 6 years.

When your preserved pension is payable

The age at which a preserved pension becomes payable depends on which scheme the service sits in, and in the case of AFPS 75 it even depends on when within that scheme you served. This trips a lot of people up, so it is worth being precise. AFPS 75 service earned before 6 April 2006 has a preserved pension age of 60. AFPS 75 and AFPS 05 service from 6 April 2006 onwards has a preserved pension age of 65. AFPS 15 deferred benefits are payable at your State Pension age.

So a single person can have more than one claim age. Somebody with a long AFPS 75 career spanning the 2006 line could have part of their preserved pension payable at 60 and part at 65. Somebody who served in AFPS 05 has a clean preserved pension age of 65. Somebody whose later service is in AFPS 15 has those deferred benefits linked to whatever their State Pension age turns out to be, which for most people serving today is 67 or 68. The calculator lets you pick the scheme so the right age is applied.

There is one extra route worth knowing for AFPS 15. A deferred AFPS 15 pension can be drawn early, from age 55, but only with a permanent actuarial reduction, because you would be taking it for longer than the scheme planned. That is a personal decision and not the default, so treat the State Pension age as the headline claim age for AFPS 15 and the age-55 option as a reduced alternative. For AFPS 75 and AFPS 05 preserved pensions, the relevant ages are 60 and 65 as set out above.

How annual revaluation protects the value

A preserved pension does not stand still while you wait for it. It is index-linked, which means it is uprated each year so that inflation does not quietly eat away its worth. The increase is tied to the Consumer Prices Index, measured to the September before each April uprating, and it is applied every April. For the year from April 2026 the increase is 3.8%, reflecting CPI to September 2025. So a preserved pension earned years ago is worth more in cash terms today than the figure first put on it, because each year's CPI rise has been layered on top.

The mechanics differ slightly by scheme, and this is where AFPS 75 and AFPS 05 have a quirk worth flagging. Preserved pensions in those two schemes are held flat until age 55, and then at 55 the whole accumulated inflation since you left is applied in one go, after which the pension rises by CPI every year. So if you left at 40 and your preserved pension is payable at 60, the buying power is still protected; the catch-up simply happens at 55 rather than year by year before then. The end result at your claim age is an inflation-protected pension.

AFPS 15 works on a similar inflation principle once benefits are deferred, rising with CPI, although while you are still serving the AFPS 15 pot is revalued in line with earnings rather than prices. The practical takeaway is the same across all three schemes: a preserved pension keeps pace with inflation between leaving and claiming, so the number you see today is a fair present-value estimate. This calculator shows the current-rate estimate and does not try to project future years of CPI growth, because nobody can know those rates in advance.

Who ends up with a preserved pension

Most people who leave the Armed Forces before pension age, with at least two years of qualifying service and without qualifying for an immediate pension, end up holding a preserved pension. That covers a very large slice of veterans. If you served a decent length of time, left to start a civilian career, and were too young or too short of service to draw your pension straight away, this is almost certainly what you have. It is the default outcome of leaving early once you have passed the two-year qualifying line. How much is an army pension after 12 years works through exactly that case, where the service is real but still short of every early-payment route.

Early Departure Payment cases are a particular group to understand here, because EDP and a preserved pension go hand in hand rather than being alternatives. If you left at age 40 or over with enough service to qualify for EDP, broadly 18 years on AFPS 05 or 20 years on AFPS 15, you receive an EDP lump sum and a monthly EDP income that bridges the gap until pension age. Behind that bridge sits your preserved pension, untouched, which then comes into payment in full when you reach your claim age. The EDP income stops and the preserved pension takes over.

Because of the McCloud changes, many people now hold a mixed record, and that affects what their preserved pension looks like. From 1 April 2022 all serving members build AFPS 15, while service in the remedy period from 1 April 2015 to 31 March 2022 can be taken as legacy benefits (75 or 05) or as AFPS 15 through a Remediable Service Statement. A typical modern leaver therefore has a preserved final-salary chunk and a deferred AFPS 15 chunk, each with its own claim age. Work out each part separately and add them together for the full picture.

How to claim with form 14

A preserved pension is not paid automatically the moment you reach your claim age. You have to claim it. The scheme does not always know your current address or bank details years after you left, so the responsibility sits with you to put your claim in as your pension age approaches. The form to use for a preserved pension is AFPS form 14. Submit it to Veterans UK a few months before your claim age so the payment is set up and ready to start on time.

It pays to plan ahead rather than leaving it to the last minute. Aim to send form 14 roughly three to six months before you reach the relevant age, which is 60 or 65 for an AFPS 75 or AFPS 05 preserved pension, or your State Pension age for AFPS 15 deferred benefits. Keep your scheme paperwork from when you left, including any preserved pension award letter, because it makes the claim quicker and helps Veterans UK match you to your record. If you cannot find your paperwork, Veterans UK can still trace your service, but it may take longer.

Form 14 is also the route to an official forecast of a preserved pension. If you are still serving and want a forecast of future benefits you would use form 12, but once you hold a preserved pension as a former member, form 14 is the one that applies to you. The forecast and the eventual claim both rely on your actual recorded service and pay, which is why the official figure is the one to trust for real decisions. This calculator gives you a sound estimate to work with in the meantime.

A worked example (illustrative)

Here is an illustrative example using round figures so the maths is easy to follow. It is not a quote and your own numbers will differ. Take someone who served in AFPS 05, left at age 45 with a preserved pension already worked out at 9,000 pounds a year, payable at 65. Their preserved pension is locked in at that point. Because AFPS 05 holds preserved pensions flat until 55 and then applies the accumulated inflation, the buying power is protected even though the cash figure stays level for the first stretch after leaving.

To show how revaluation works, imagine a single year's CPI uprating of 3.8%, the figure that applies from April 2026, applied to that 9,000 pounds preserved pension. That one year's increase adds 342 pounds, lifting it to 9,342 pounds. Over many years between leaving and claiming, successive CPI increases compound in this way, which is why a preserved pension claimed at 65 is typically worth considerably more in cash than the figure first awarded. The point of revaluation is that the pension keeps pace with the cost of living rather than losing ground.

Now picture the same person, but with later service in AFPS 15. That deferred AFPS 15 chunk would be payable not at 65 but at their State Pension age, and it is uprated by CPI once deferred. So this one veteran has two preserved or deferred blocks with two different claim ages: the AFPS 05 part at 65 and the AFPS 15 part at State Pension age. They would claim each at the right time using the correct process. Swap your own scheme, pension figure and leaving age into the calculator above to see your version of these numbers.

Common mistakes to avoid

The most common and costly mistake is simply forgetting to claim. A preserved pension does not start paying itself; if you do not submit form 14, the money sits there unpaid. Backdating is possible in many cases, but it is far better to claim on time than to chase missed payments later. Put a reminder in place now for the year you turn your claim age, whether that is 60, 65 or your State Pension age, so the date does not slip past you in the busy years of civilian life.

The second mistake is assuming a preserved pension has lost its value because the cash figure looked the same for a while. As explained above, AFPS 75 and AFPS 05 preserved pensions are flat until 55 and then catch up all accumulated inflation in one step, so a quiet first stretch does not mean the value has been eroded. People sometimes write off a preserved pension as not worth bothering with, which can be a serious error given how much it grows once revaluation and the age-55 catch-up are taken into account.

The third mistake is mixing up the claim ages on a mixed record. With McCloud, plenty of people hold both a final-salary preserved pension and a deferred AFPS 15 pension, and these are payable at different ages. Treating them as one pot with one date can mean claiming the wrong thing at the wrong time, or missing one block entirely. Keep the schemes separate, note the claim age for each, and use the correct scheme setting in the calculator so the right age and method are applied to each part.

How a preserved pension is taxed

When a preserved pension comes into payment, the annual pension is taxable income. It is added to any other income you have at that point, such as the State Pension or earnings if you are still working, and taxed under the normal Income Tax rules for that year. The calculator shows the gross pension, so remember the income figure is before tax. Because a preserved pension often starts in the same window as the State Pension, it is worth checking how the two stack together so a higher tax band does not catch you by surprise.

Any tax-free lump sum that comes with the pension is paid tax-free within HMRC limits, in the same way as for a pension drawn at normal pension age. For AFPS 75 and AFPS 05 that includes the automatic lump sum built into those schemes; AFPS 15 pays no automatic lump sum but allows you to commute pension into a tax-free lump sum at the scheme's fixed rate. The income side is taxable and the lump sum side is tax-free, and keeping those two buckets clearly separate avoids a lot of confusion at claim time.

This page gives general information, not tax advice, and it is not regulated financial advice. The schemes are governed by their own rules and by HMRC limits that can change over time. If your preserved benefits are large, or you have several pensions arriving around the same age, it is sensible to take regulated advice before making any irreversible decision. We are an independent education site and are not affiliated with the MOD, Veterans UK or JPAC.

How to check your own position

This calculator gives you a quick, honest estimate of a preserved or deferred pension and tells you the age at which it becomes payable for the scheme you select. It applies the published claim ages, 60 or 65 for AFPS 75 and AFPS 05 service and State Pension age for AFPS 15, along with the annual CPI uprating, exactly as the schemes set them out. It is ideal for sanity-checking what you are owed and when, but it cannot see your individual service record or your exact pensionable pay.

To check your real position, get your own facts straight first. Confirm which scheme or schemes your service falls under, note your qualifying service to make sure you cleared the two-year line, and identify the claim age for each block of benefits. If your record spans the McCloud remedy period from 1 April 2015 to 31 March 2022, factor in your Remediable Service Statement choice, because it decides whether that window is legacy or AFPS 15 and therefore which claim age applies to it.

The only official forecast of a preserved pension comes from Veterans UK, and form 14 is the route for former members who hold one. That forecast uses your actual recorded service and pay, so it is the figure to rely on for real financial decisions, and it is also the document that sets up your claim when the time comes. Use the estimate here to plan and to understand the moving parts, then confirm the official numbers with Veterans UK as your claim age approaches.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Preserved & deferred pensions explained

When you can claim it, and how it is revalued while you wait.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.