Which armed forces pension scheme am I in?

Your scheme is set mainly by when you first joined the Regular forces. There are three of them, AFPS 75, AFPS 05 and AFPS 15, and they pay out in genuinely different ways. Most people who served between 2015 and 2022 also carry a McCloud remedy choice on top, so it is common to have benefits in more than one place. This guide walks you through how the dates fall, what each scheme means for your eventual pension, and how to check your own record so you are not relying on the mess hall version.

Key takeaways

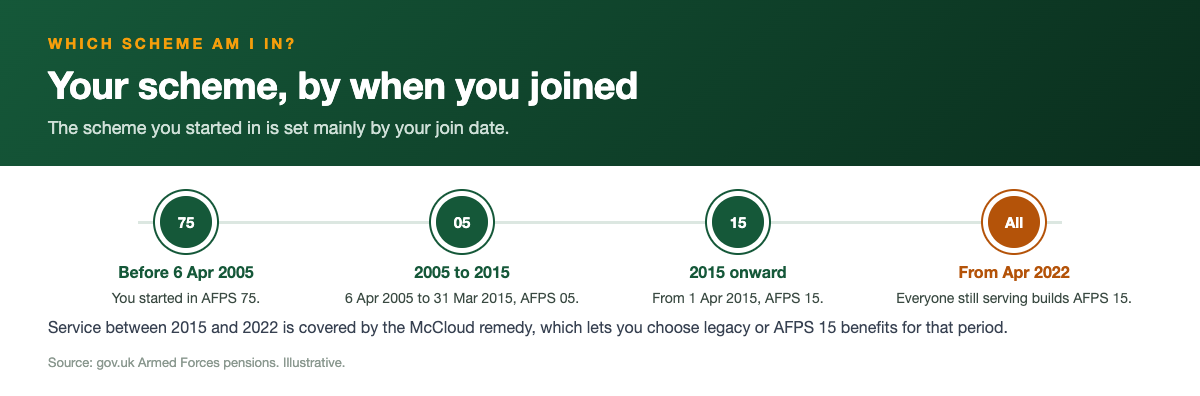

- Joined before 6 April 2005, you started in AFPS 75; joined 6 April 2005 to 31 March 2015, you started in AFPS 05; joined on or after 1 April 2015, you started in AFPS 15.

- From 1 April 2022 everyone still serving builds new pension in AFPS 15, whatever scheme they began in.

- AFPS 75 and AFPS 05 are final-salary; AFPS 15 is career average (CARE), banking 1/47th of your pay each year.

- If you served any part of 1 April 2015 to 31 March 2022, the McCloud remedy lets you choose legacy or AFPS 15 benefits for that window.

- You need 2 years' qualifying service to earn a pension at all, and pensions in payment rise 3.8% from April 2026.

- Your annual benefit statement and a Veterans UK forecast (form 12 serving, form 14 preserved) are the only ways to confirm your scheme for certain.

Your join date sets your starting scheme

The simplest way to think about it is that the date you signed on decides which scheme caught you first. Join before 6 April 2005 and you went straight into AFPS 75. Join between 6 April 2005 and 31 March 2015 and you started in AFPS 05. Join on or after 1 April 2015 and you began in AFPS 15. Those dates are not arbitrary; each scheme closed to new entrants on the day the next one opened.

This matters because the scheme you started in shapes the part of your pension built up before April 2022, and the rules for that older service are protected. Someone who enlisted in 1998, for example, holds AFPS 75 rights for the years up to the point they moved across, and those are worked out on final-salary rules even though the person is now banking AFPS 15 each year.

Plenty of careers do not run in a tidy straight line, so the join-date rule is the starting point rather than the whole answer. Breaks in service, a discharge and re-enlistment, or a transfer in from another public-sector scheme can all change which scheme applies to which slice of service. If any of that describes you, treat the dates above as a strong steer and confirm it against your own statement.

The three schemes and how they differ

AFPS 75 is a final-salary scheme. It builds towards a maximum of 48.5% of your final pensionable pay over a full career, which is 34 years for officers and 37 years for other ranks, and it pays an automatic tax-free lump sum of three times your annual pension. Its normal pension age is 55, and a preserved AFPS 75 pension is paid from 60 for service before 6 April 2006 and from 65 for service after that. Because it is built on a representative rate for your final rank rather than your exact salary, two people leaving at the same rank with the same service usually end up with much the same pension.

AFPS 05 is also final-salary but works on a cleaner formula. You earn 1/70th of your final pensionable pay for every year served, building up to around 57% at 40 years, again with an automatic tax-free lump sum of three times your pension. It shares the normal pension age of 55 with AFPS 75, but the difference shows if you leave early, because an AFPS 05 preserved pension is paid at 65 rather than the 60 that applies to AFPS 75 service before 6 April 2006.

AFPS 15 is a different animal. It is a career average (CARE) scheme: each year the MOD banks 1/47th of that year's pensionable pay into a pot, and that pot is revalued each year so it keeps its value against inflation. There is no automatic lump sum, but you can commute up to 25% of your pension for tax-free cash at a fixed rate of £12 for every £1 of yearly pension you give up. Its normal pension age is 60, and a deferred AFPS 15 pension is paid at your State Pension age, with an Early Departure Payment available from age 40 if you qualify.

Everyone serving moved to AFPS 15 in 2022

From 1 April 2022, every member still serving builds their new pension in AFPS 15, no matter which scheme they originally joined. This was the final step in closing the older schemes to ongoing build-up, and it applies whether you are an officer or other rank, Regular or Reserve. If you joined in 2002 on AFPS 75, you stopped adding final-salary service in 2022 and have been banking 1/47ths in AFPS 15 ever since.

The good news is that nothing you already earned is lost. Any pension you built in AFPS 75 or AFPS 05 before the move is an accrued right: it is protected and paid under its own scheme's rules, and it stays linked to your pay and rank at the point you actually leave, not frozen at the 2022 changeover. So a long-serving member typically ends up with two pots, an older final-salary slice and a newer CARE slice, each paid on its own terms.

In practice this means your eventual pension statement can read like two schemes stitched together, because that is exactly what it is. It is worth getting your head around which part is which, since the older slice and the newer slice have different pension ages and different lump-sum rules, and that affects when and how you can draw each one.

The McCloud remedy and the remedy period

When AFPS 15 came in during 2015, the government moved younger members across but let those closer to retirement stay in their legacy scheme for a while longer. The courts ruled in the McCloud and Sargeant cases that protecting people by age in this way was unlawful age discrimination, and the fix is what everyone now calls the McCloud remedy.

The remedy period runs from 1 April 2015 to 31 March 2022. If you were serving and affected during any of that window, you get a choice for those years: take the benefits you would have had under your legacy scheme (AFPS 75 or 05), or take AFPS 15 benefits instead. You do not have to decide blind, because Veterans UK provides a Remediable Service Statement (RSS) that sets out your figures calculated both ways so you can compare like for like.

For most people the choice is deferred, which means you make it at the point you actually draw your pension rather than now, when your final pay and circumstances are known and the comparison is sharper. Those already retired or very close to it get an earlier choice. There is no single right answer: final-salary terms often suit people promoted late in their career, while the CARE basis can suit others, and tax can come into it too, so it is a genuine decision to weigh rather than a formality.

Exceptions: breaks, rejoiners and transfers in

The clean join-date rule bends in a few common situations, and these are exactly the cases where people guess wrong. If you left and rejoined after a break in service, the scheme that applies to your later spell can differ from your first, and a long enough gap can mean you come back into AFPS 15 even though your original service was on an older scheme. The break's length and timing both matter.

Transfers in are another wrinkle. If you brought pension rights across from a previous employer or another public-sector scheme, those transferred-in benefits are usually held within whichever AFPS scheme you were in when the transfer landed, and they do not always behave like service you earned directly. The same goes for moves between Regular and Reserve service, which can affect how your service is aggregated.

None of this changes the headline that all ongoing build-up is in AFPS 15 from April 2022. What it changes is the treatment of your earlier slices, and that is the bit worth pinning down. If your career included any break, rejoin, transfer in, or a switch between Regular and Reserve, do not assume; get it confirmed in writing rather than working from a date in your head.

How to check your own scheme for certain

Start with your annual benefit statement. Serving members get one each year, and it sets out the scheme or schemes you are in and the benefits built up so far. It is the quickest sense-check, and for most people it confirms the picture in a couple of minutes. If you cannot lay hands on a recent one, your unit HR or pay staff can point you at how to get it.

For anything you intend to make a real decision on, get an official forecast from Veterans UK. If you are still serving, that is form 12; if you have left with a preserved pension, it is form 14. A forecast is the authoritative figure: it reflects your actual service record, your accrued rights in the older schemes, and where relevant your McCloud remedy position, which a general calculator cannot fully reproduce.

This site is independent and is not affiliated with the MOD, Veterans UK or JPAC, and the numbers here are estimates rather than regulated financial advice. Use our tools to get a feel for how your pension is put together and to ask better questions, then confirm the specifics with an official forecast. For a genuinely complex choice, such as how to handle your remedy years, taking regulated advice as well is money well spent.

One thing your service does not change: the AFPS is tri-service, so the same rules apply whether you served with the Army, the Royal Navy, the Royal Marines or the RAF. We publish the calculator framed for each, at Army, RAF, Royal Navy and Royal Marines, plus a version for reserves and FTRS and one for officers. They run the same maths; pick whichever wording matches your record.

What each scheme means for your eventual pension

Which scheme your service sits in changes both how much you get and when you can take it. On AFPS 75, the maximum is up to 48.5% of final pensionable pay over a full career with an automatic three-times lump sum, and the normal pension age is 55, with a preserved pension paid at 60 for service before 6 April 2006 and at 65 for service after that. On AFPS 05 you build 1/70th a year up to around 57% with the same three-times lump sum, and the normal pension age is also 55, but a preserved AFPS 05 pension is not paid until 65, so the wait can be longer if you leave before then.

AFPS 15 rewards every year you serve rather than just your final rank, because it banks 1/47th of each year's pay and revalues it for inflation. There is no automatic lump sum, so if you want tax-free cash you commute some pension at the fixed £12 per £1 rate, up to 25%. Its normal pension age is 60, and a deferred AFPS 15 pension tracks your State Pension age instead, which for younger members is later than the older schemes, though an Early Departure Payment from age 40 can bridge the gap for those who qualify.

Early-leaver routes differ too, and they often matter more than the headline accrual. AFPS 05 offers EDP for those who reach broadly 18 years' service and age 40; AFPS 15 EDP needs broadly 20 years and age 40, and its EDP lump sum is 2.25 times your preserved pension. Whatever the scheme, you need at least 2 years' qualifying service to earn a pension, and once a pension is in payment it rises with inflation, by 3.8% from April 2026.

What to do next

First, fix your dates. Note when you joined, any break in service, and whether you have ever transferred pension in, because those three things between them explain almost every case where the simple rule does not hold. With that written down, the join-date guide above will tell you which scheme started you off and roughly how your service splits before and after April 2022.

Second, pull your most recent annual benefit statement and read off the scheme or schemes it lists. If you are weighing a real decision, leaving, drawing early, or comparing your McCloud options, request a Veterans UK forecast on form 12 if serving or form 14 if preserved, and wait for those figures before you commit to anything. An estimate is fine for planning; it is not the number to resign on.

Third, use the calculator here to model your pension and see how the older and newer slices stack up, then take the questions it raises to an official forecast and, for the bigger calls, a regulated adviser who knows the armed forces schemes. That order, dates first, then statement, then forecast, then advice, keeps you from making an irreversible choice on a half-remembered figure.

See your own numbers

Get your pension, lump sum and EDP in seconds.

Frequently asked questions

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk · GAD factors · Veterans UK · Forces Pension Society · MoneyHelper.