AFPS 05 Pension Calculator

Calculate your AFPS 05 pension using the 1/70th final-salary accrual, plus your automatic 3× lump sum, up to 57% of final pensionable pay.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the AFPS 05 estimate is worked out

AFPS 05 is also final-salary, building 1/70th of your final pensionable pay for each year served, up to about 57% of pay. It pays an automatic tax-free lump sum of three times your pension and can include an Early Departure Payment if you leave early with enough service.

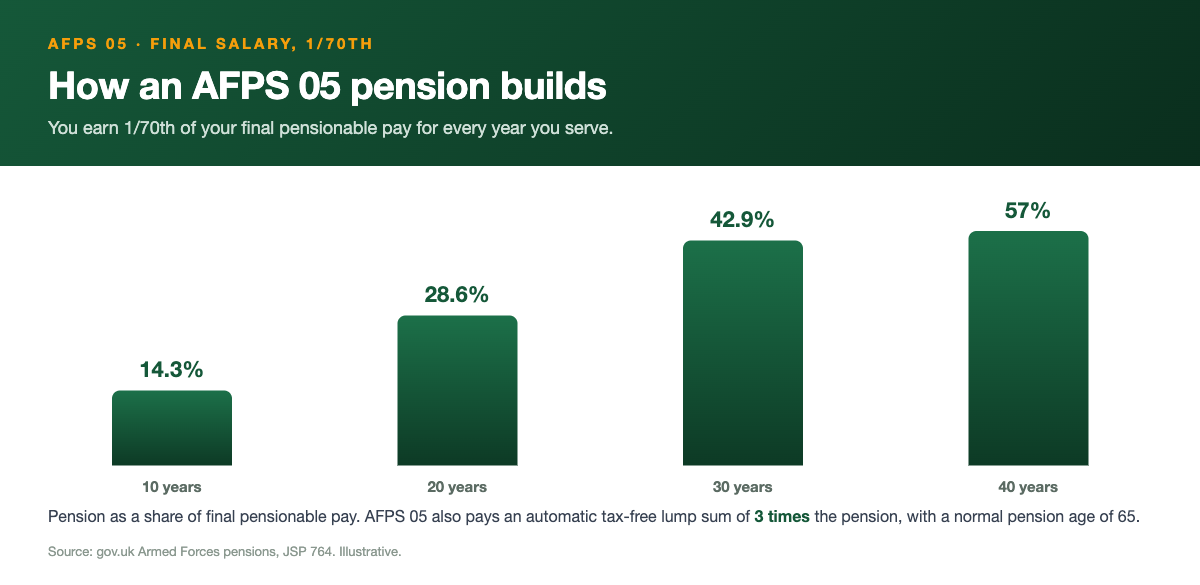

How the AFPS 05 pension is built

AFPS 05 is a final-salary scheme, which means your pension is worked out from your pay at the end of your career, not an average of what you earned along the way. For every year of reckonable service you bank one seventieth (1/70th) of your final pensionable pay. So the longer you serve, the bigger the slice of your final salary that your pension represents. It is a simple sum once you know the two ingredients: your final pensionable pay and your reckonable service.

The headline formula the calculator uses is final pay multiplied by years of service, divided by 70. The pension keeps growing on that basis until it reaches the scheme ceiling of 57% of your final pensionable pay, which you hit at 40 years of reckonable service. Beyond that point extra service does not increase the annual pension, because the scheme caps it. Most people leave well before 40 years, so for the majority the 1/70th accrual is what matters day to day.

Final pensionable pay is the pay used to value your pension, not necessarily your gross take-home figure, and it does not normally include allowances such as Longer Separation Allowance or accommodation. The calculator treats the pay you enter as your final pensionable pay, so put in the best figure you have for that. If you are still serving, you can use your current pensionable pay as a reasonable stand-in and refine it as you get closer to your exit date.

Your automatic tax-free lump sum

On top of the annual pension, AFPS 05 pays an automatic tax-free lump sum worth three times your annual pension. You do not have to ask for it, give anything up, or make a decision to receive it. It is built into the scheme and paid as a single tax-free amount when your pension comes into payment. This is one of the most valuable features of AFPS 05 and a big reason the scheme is well regarded.

Because the lump sum is a fixed multiple of the pension, anything that increases your annual pension increases the lump sum in the same proportion. A higher final pensionable pay or more years of service lifts both figures together. The calculator shows the lump sum on its own row so you can see the cash alongside the income. Treat both as estimates until Veterans UK confirms the official numbers.

It is worth being clear about what the 3x lump sum is and is not. It is the standard automatic lump sum that comes with the AFPS 05 pension. It is separate from any commutation arrangement and separate from the EDP lump sum that early leavers may receive. Keep those buckets distinct in your head, because mixing them up is one of the most common sources of confusion when people compare their options.

Normal pension age and leaving early

AFPS 05 has a normal pension age of 55, so serving to 55 means your full pension and automatic lump sum come into payment straight away, without any reduction. Leave before that and the benefits you have earned are preserved instead, and paid in full from 65. Until then a preserved pension sits index-linked in the background, rising each year so its buying power is protected. If the date you go matters more to you than the years you have served, the military pension calculator runs the same figures on your own pay, rank and scheme.

Leaving early does not mean you lose your pension. It becomes a preserved (deferred) pension, payable in full at 65, and it is uprated by the annual CPI increase in the meantime. For context, pensions in payment and preserved pensions rise by 3.8% from April 2026. The scheme also offers an Early Departure Payment for those who leave at age 40 or over with enough service, which bridges the gap between leaving and 65, and we cover that next.

If you are weighing up a move now versus serving longer, the age-65 point is central to the maths. An early exit means a smaller pension built on fewer years, paid (in full) later, with EDP potentially filling the income gap in between. Serving longer means more 1/70ths banked and a larger final-salary figure to multiply against. The calculator lets you test both by changing the years and the leaving age.

Early Departure Payment (EDP 05)

EDP 05 is the scheme's reward for committing a good chunk of a career without serving all the way to 65. To qualify you must leave at age 40 or over with at least 18 years of reckonable service. Meet both tests and you receive two things: a tax-free lump sum worth three times your preserved pension, and a monthly income paid from the day you leave until your pension proper starts at 65. It is designed to ease the transition into civilian life after a long service.

The EDP monthly income is commonly quoted at around 50% of your preserved pension, and that is the headline rate the calculator applies. The exact award rises with the length of your service and is uprated by CPI from age 55, so treat the 50% figure as a solid estimate rather than a precise promise. The EDP lump sum, at three times the preserved pension, mirrors the 3x structure of the main scheme lump sum, which makes it easier to picture.

Two points trip people up. First, the EDP income is a bridge, not your final pension: at 65 the EDP stops and your full preserved pension and automatic lump sum take over. Second, both the 18-year service test and the age-40 test must be met, so leaving at 39 with 18 years, or at 42 with 16 years, does not unlock EDP 05. The calculator only shows an EDP figure when both conditions are satisfied.

Who is in AFPS 05

AFPS 05 covers regulars who joined between 6 April 2005 and 31 March 2015. If you signed up in that window you started your service in the 2005 scheme rather than the older AFPS 75 or the newer AFPS 15. It was the standard scheme for a decade and a very large number of serving personnel and veterans have at least some service in it.

From 1 April 2022 everyone still serving moved into AFPS 15 for future service under the McCloud changes, so AFPS 05 service for most current members is a closed, historic chunk rather than something still growing. That earlier AFPS 05 service is preserved and still counts; it simply stopped adding new 1/70ths from that date. The McCloud remedy period runs from 1 April 2015 to 31 March 2022, and affected members get to choose legacy benefits (75 or 05) or AFPS 15 for that window through a Remediable Service Statement.

Because of this, a lot of people have a mixed record: a block of AFPS 05 final-salary pension, plus AFPS 15 CARE benefits for later service, and a McCloud choice sitting over the 2015 to 2022 period. This calculator focuses on the AFPS 05 part. If your situation spans more than one scheme, work out each part and then add the results together to see your full picture.

A worked example (illustrative)

Here is an illustrative example using only round figures so the maths is easy to follow; it is not a quote and your own numbers will differ. Take a service leaver with 30 years of reckonable service and a final pensionable pay of 35,000 pounds. The annual pension is final pay times years divided by 70, so 35,000 times 30 divided by 70, which comes to 15,000 pounds a year. That is the income figure before any tax on the pension itself.

The automatic tax-free lump sum is three times the annual pension, so three times 15,000 pounds gives 45,000 pounds, paid tax-free as a single amount when the pension starts. With 30 years of service the pension sits at roughly 43% of final pay, comfortably below the 57% ceiling, so no cap applies in this example. If the same person had served the full 40 years, the pension would be limited to 57% of final pay, which is the scheme maximum.

Now suppose this person instead left at age 45 with 18 years of service rather than serving on. They would meet the EDP 05 tests (age 40 or over, at least 18 years). They would receive an EDP lump sum of three times the preserved pension and a monthly EDP income of roughly 50% of that preserved pension until 65, when the full preserved pension and the automatic 3x lump sum come into payment. Swap in your own pay, service and leaving age above to see your version of these figures.

How AFPS 05 benefits are taxed

The automatic lump sum is paid tax-free, within HMRC limits, which is a major advantage of the scheme. The annual pension, by contrast, is taxable income. It is added to any other income you have in retirement, such as the State Pension or a civilian salary, and taxed under the normal Income Tax rules for the year. The calculator shows the gross pension, so remember that the income figure is before tax even though the lump sum is not.

If you take EDP 05 as an early leaver, the same split applies: the EDP lump sum is tax-free, while the monthly EDP income is taxable. People who leave the forces and start a civilian job sometimes find the EDP income pushes them into a higher tax band for a few years, simply because it stacks on top of new earnings. It is worth modelling that with your expected civilian salary so there are no surprises in your first tax year out.

This page gives general information, not tax advice, and it is not regulated financial advice. AFPS 05 is governed by the scheme rules and by HMRC limits that can change. If your benefits are large, or you have other pensions in play, it is sensible to take regulated advice before making irreversible decisions. We are an independent education site and not affiliated with the MOD, Veterans UK or JPAC.

How to check your own figure

This calculator is built to give you a quick, honest estimate from three inputs: your final pensionable pay, your reckonable service and your leaving age. It applies the published 1/70th accrual, the 57% ceiling, the automatic 3x lump sum and the EDP 05 tests exactly as the scheme sets them out. It is ideal for sanity-checking a decision or seeing how an extra few years would change things, but it cannot see your individual service record.

The only official forecast of your AFPS 05 benefits comes from Veterans UK. If you are still serving, request a pension forecast using form 12; if you have already left and hold a preserved pension, use form 14. Those forecasts use your actual recorded service, your exact final pensionable pay and any scheme detail this tool cannot reproduce, so they are the figures to rely on for real decisions.

Before you ask for an official forecast, it pays to get your own facts straight: confirm your reckonable service to the day, check your final pensionable pay rather than your gross pay, and note your intended leaving age. If you have mixed AFPS 05 and AFPS 15 service, or a McCloud choice over the 2015 to 2022 remedy period, factor that in too. With those details to hand, the estimate here and the official forecast should line up closely, and you will know exactly where you stand.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Not sure which scheme you're in?

Find out whether you're on AFPS 75, 05 or 15 and how each builds up.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.