Royal Navy Pension Calculator

Calculate your Royal Navy pension and lump sum under AFPS 75, 05 and 15, for ratings and officers.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Royal Navy estimate is worked out

Your Royal Navy pension follows the Armed Forces Pension Scheme that applied while you served. Pick the scheme that matches when you joined, most careers touch more than one.

AFPS 75 is a final-salary scheme. Your pension is a share of representative pay for your rank, building to a maximum of 48.5% over a full career, 34 years for officers, 37 for other ranks, with an automatic tax-free lump sum of three times the annual pension.

AFPS 05 is also final-salary, building 1/70th of your final pensionable pay for each year served, up to about 57% of pay. It pays an automatic tax-free lump sum of three times your pension and can include an Early Departure Payment if you leave early with enough service.

AFPS 15 is a Career Average Revalued Earnings (CARE) scheme. It adds 1/47th of your current pensionable pay each year, revalued for inflation, rather than using a final salary. There is no automatic lump sum, so you can commute up to 25% of your pension for tax-free cash at a fixed rate of £12 per £1 of yearly pension given up.

How a Royal Navy pension is built

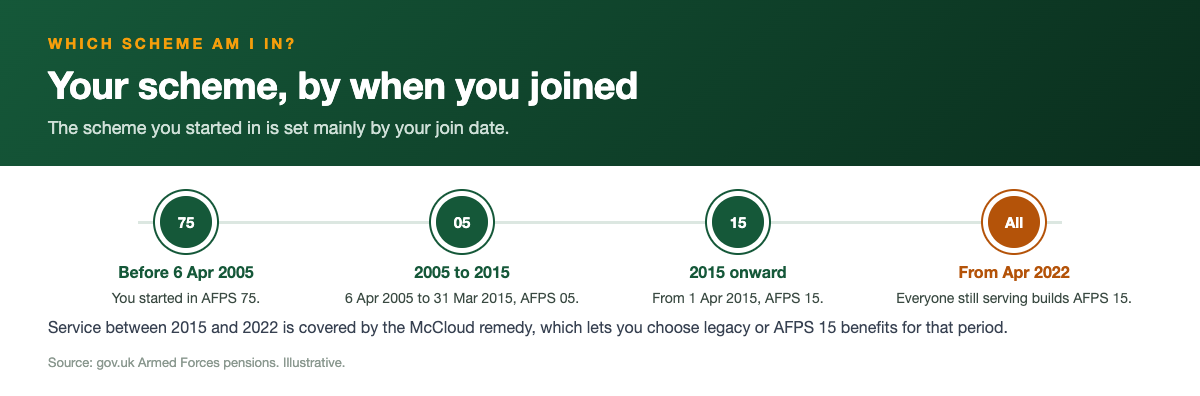

Your Royal Navy pension does not sit in a separate Navy scheme. Ratings, warrant officers and commissioned officers in the Senior Service are all members of the same Armed Forces Pension Scheme (AFPS) as the Army and the RAF. Which version of that scheme you are in comes down to one thing: when you joined or transferred. There are three to know about, AFPS 75, AFPS 05 and AFPS 15, and the calculator on this page lets you model each one using the pay and service figures you put in.

The dividing lines are simple. If you joined between 1 April 1975 and 5 April 2005 you started in AFPS 75. If you joined between 6 April 2005 and 31 March 2015 you started in AFPS 05. Anyone who joined from 1 April 2015 went straight into AFPS 15, and from 1 April 2022 every serving member of the Royal Navy builds AFPS 15 going forward, whatever they joined on. Service before that transition is protected and paid as originally promised.

The two older schemes (75 and 05) are final-salary, which means your pension is worked out from your pay near the end of your career and your length of service. AFPS 15 is a Career Average Revalued Earnings (CARE) scheme, which builds up a pot from a slice of your pay every single year and revalues it for inflation. They reward service differently, so it pays to model the scheme that actually applies to you rather than assume they all work the same way.

AFPS 75 for ratings and officers

AFPS 75 is the oldest scheme and the most generous in some respects, but also the most rank-based. Your pension is not worked out from the exact salary you were paid. Instead it uses a representative rate of pay for your final rank, so two senior rates who leave on the same rank with the same reckonable service will normally get the same pension. Accrual starts from age 18 for ratings and Royal Marines other ranks, and from age 21 for officers.

The pension builds up to a maximum of 48.5% of representative pay over a full career. A full career here means 37 years for ratings and other ranks, and 34 years for officers, and the calculator builds the percentage up in a straight line to that 48.5% ceiling. On top of the annual pension, AFPS 75 pays an automatic tax-free lump sum equal to three times that pension, with no need to give anything up to get it.

AFPS 75 has its own early-payment route called the Immediate Pension, rather than the EDP used by the later schemes. A rating reaches the Immediate Pension point after 22 years from age 18, and an officer after 16 years from age 21. The pension is then paid flat until age 55, when all the inflation that has built up is applied and CPI uprating continues each year after that. If you leave before the Immediate Pension point, your pension is preserved and paid at age 60.

Because we do not hold the Ministry of Defence's rank-by-rank representative pay tables, the calculator uses the pay figure you enter as a stand-in and tells you so on screen. That makes the AFPS 75 result an illustration rather than a quote. For a precise figure tied to your representative rate, you need an official forecast from Veterans UK.

AFPS 05, the 1/70th scheme

AFPS 05 is also final-salary, but it works on a cleaner formula than AFPS 75. For every year of reckonable service you bank one seventieth (1/70th) of your final pensionable pay. Serve ten years on a final pay of, say, a senior rate's salary and you have built ten seventieths of that pay as an annual pension. The accrual keeps building to a maximum of about 57% of final pay, reached at 40 years' service.

Like AFPS 75, AFPS 05 pays an automatic tax-free lump sum of three times your annual pension, so you do not have to surrender any income to receive it. The normal pension age under AFPS 05 is 55, so serving to 55 means an immediate pension, while a member who leaves before that has a preserved pension waiting for them at 65 unless they qualify for the Early Departure Payment described below.

The trade-off between 75 and 05 is real. AFPS 75 can reach a higher proportion of pay faster for a long full-career servant on a single rank, while AFPS 05 rewards each year cleanly at 1/70th and carries a later preserved pension age. The calculator lets you switch the scheme and compare the annual pension and lump sum side by side, which is the quickest way to see which formula treats your own service better.

AFPS 15, the CARE scheme everyone now builds

AFPS 15 is the scheme every serving sailor and Royal Marine is building today. It is a Career Average Revalued Earnings scheme, so instead of leaning on your final pay it banks one forty-seventh (1/47th) of your pensionable earnings every scheme year, from 1 April to 31 March, into a running pension pot. Each past year's slice is then revalued for inflation so it keeps its value, which is why a long career still builds a substantial pension even though no single year of pay dominates the sum.

There is no automatic lump sum under AFPS 15. If you want tax-free cash you create it by commuting, which means giving up some annual pension in exchange for a one-off payment. The rate is fixed at about 12 to 1, so every £1 of annual pension you surrender buys about £12 of lump sum, and HMRC caps the amount you can commute at 25% of your benefits. That reduction to your pension is permanent, so it is a decision to weigh carefully rather than a free top-up.

Because the in-service revaluation keeps each past year broadly in line with current earnings, the calculator can give a sound AFPS 15 estimate from your current pensionable pay using pay times years divided by 47. That is the same simplification scheme explainers use, and it saves you from having to reconstruct a true career average you could never easily provide. You need at least two years of qualifying service to earn a pension at all under AFPS 15.

EDP, leaving before pension age

Most people leave the Royal Navy long before any normal pension age, and the Early Departure Payment (EDP) is the scheme's answer to that. EDP is not your pension paid early. It is a separate package, a tax-free lump sum plus a taxable monthly income, that bridges the gap from your exit until your preserved pension comes into payment at pension age. It only exists in AFPS 05 and AFPS 15. AFPS 75 uses its Immediate Pension instead.

Under AFPS 05 the EDP point is broadly 18 years' service and age 40. The lump sum is three times your preserved pension, and the monthly income is around 50% of that preserved pension, rising with longer service and uprated by CPI from age 55. Under AFPS 15 the bar is broadly 20 years and age 40, the so-called 20/40 point. The AFPS 15 EDP lump sum is 2.25 times your preserved pension, and the income starts at 34% of the preserved pension with an extra 0.85% added for every year you served beyond 20.

For a Royal Navy career that ends in the late thirties or forties, EDP is often the single biggest number in the calculation, so it is worth modelling properly. Set your scheme, your years of service and your leaving age in the calculator and it will show the EDP lump sum and the monthly income separately. Remember the monthly EDP income is taxable as earnings, even though the lump sum is tax-free, which matters for the year you leave.

A worked example (illustrative)

Here is an illustrative example using only the scheme rates already described, not a real person. Picture a rating in AFPS 05 who leaves at age 41 after 22 years of reckonable service, on a final pensionable pay we will call P. The 1/70th accrual gives an annual pension of 22 divided by 70 times P, which is 22/70 of P, or just under a third of final pay. The automatic tax-free lump sum is three times that pension.

Because this sailor is over 40 and has more than 18 years in, they qualify for EDP 05. The EDP lump sum is three times the preserved pension, and the monthly EDP income works out at roughly 50% of the preserved pension divided by twelve, paid until the AFPS 05 preserved pension age of 65, when the preserved pension itself begins. The lump sums are tax-free; the monthly EDP income is taxable.

Now run the same 22 years through AFPS 15 instead and the shape changes. The pension is built from 1/47th of pay per year rather than a single final-salary calculation, there is no automatic lump sum unless they commute, and the EDP needs the 20/40 point, which they meet, paying a 2.25 times lump sum and a 34% income with the year-over-20 additions. The point of the example is not the exact pounds, which depend on your own pay, but to show how differently the two schemes treat the same length of service. Treat every figure here as illustrative and confirm your own with an official forecast.

McCloud and your remedy choice

If you served across the 2015 changeover you will have heard the name McCloud. In short, the courts found that moving older members onto AFPS 15 while protecting those closer to retirement was unlawful age discrimination. The fix, called the remedy, covers the period from 1 April 2015 to 31 March 2022. For those years, affected Royal Navy members can choose whether to take legacy benefits (AFPS 75 or 05) or AFPS 15, rather than having AFPS 15 imposed.

You do not make that choice now in the dark. When your pension becomes payable, Veterans UK issues a Remediable Service Statement setting out both options in pounds so you can pick whichever is worth more to you. From 1 April 2022 onwards there is no choice to make, because everyone simply builds AFPS 15 going forward. The years before 1 April 2015 stay in whichever legacy scheme you were in.

For the calculator this means a member caught by McCloud is really two calculations stitched together: a legacy-scheme result and an AFPS 15 result for the remedy years. Model both schemes here to get a feel for which way your remedy choice is likely to lean, then treat the Remediable Service Statement as the document that actually decides it. Do not act on a remedy choice on the strength of an estimate alone.

Tax treatment and how to check your figure

The tax picture is straightforward in outline. Your automatic lump sums under AFPS 75 and AFPS 05, and your EDP lump sums under AFPS 05 and AFPS 15, are paid tax-free. Your annual pension, once in payment, is taxable as income in the normal way, and the monthly EDP income that bridges you to pension age is taxable as earnings too. Pensions already in payment rise each year with CPI, and the increase from April 2026 is 3.8%.

This calculator gives an estimate, not regulated financial advice, and this is an independent education site that is not affiliated with the Ministry of Defence, Veterans UK or JPAC. The figures it produces are good enough to plan and compare with, but they cannot reproduce every rank-based pay table, age-banded factor or McCloud nuance. For a number you can rely on for a real decision, you need an official forecast.

To get that, request a forecast from Veterans UK using form 12 if you are still serving, or form 14 if you have left and hold a preserved pension. Have your service record and current pensionable pay to hand so your input here is as accurate as possible. Use this page to understand how your Royal Navy pension is built and to compare the schemes, then let the official forecast confirm the exact amount before you commit to anything.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Not sure which scheme you're in?

Find out whether you're on AFPS 75, 05 or 15 and how each builds up.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.