Early Departure Payment (EDP) explained

The Early Departure Payment, or EDP, supports people who leave the forces before their normal pension age but with enough qualifying service behind them. It pays a tax-free lump sum on the way out, plus a monthly income that runs until your scheme pension comes into payment at pension age. It exists on AFPS 05 and AFPS 15 only, and it is paid on top of, and separately from, the pension you have already built. Think of it as a bridge across the years between leaving and your pension age, not a replacement for the pension itself.

Key takeaways

- EDP is for early leavers who have qualifying service but have not yet reached their scheme pension age.

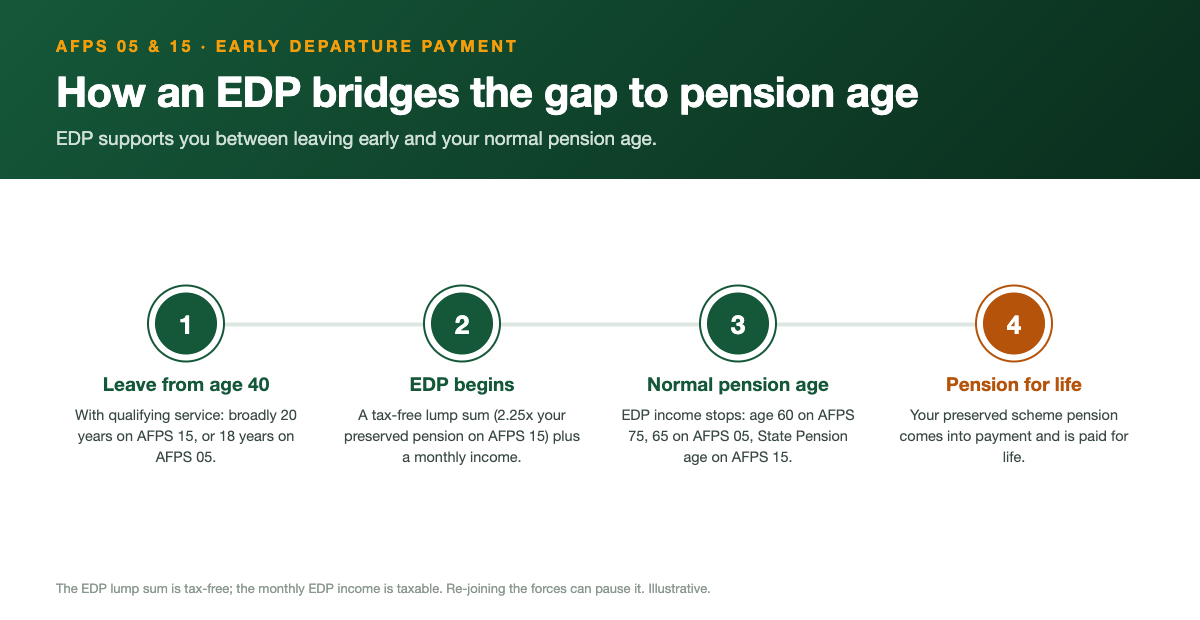

- AFPS 05: broadly 18 years' service and at least age 40. AFPS 15: broadly 20 years' service and at least age 40.

- It pays a tax-free lump sum plus a monthly income that bridges the gap to pension age.

- On AFPS 15 the EDP lump sum is 2.25 times your preserved pension, and the monthly income is a percentage of it.

- The lump sum is tax-free, but the monthly EDP income is taxable as earned income.

- If you just miss the EDP test you usually get a preserved pension instead, payable later at your scheme's preserved pension age.

What the EDP is and why it exists

Armed Forces careers often end well before the age at which a normal pension would start to pay. Someone might leave in their early forties after a full and demanding career, yet their scheme pension age could still be years, sometimes decades, away. The Early Departure Payment was designed to deal with exactly that gap. It recognises long service and gives leavers something to live on, and a capital sum to resettle with, during the stretch between handing in their kit and the day their pension finally comes into payment.

The EDP is not a reward for leaving early in itself. It is there to acknowledge that a service career has a shorter natural span than most civilian working lives, and that the people who serve a long time should not be left with nothing until a distant pension age. So it combines two things: a one-off tax-free lump sum paid when you leave, and a monthly income paid from then until your pension age. When you reach pension age the EDP income stops and your scheme pension takes over.

It is worth being clear from the outset that the EDP exists on AFPS 05 and AFPS 15 only. AFPS 75 does not have an EDP. The older 1975 scheme handles early leaving through its own Immediate Pension and resettlement arrangements instead, so if you are an AFPS 75 member the rules described here do not apply to you, and AFPS 75 vs 05 vs 15 sets out how the three schemes differ. The rest of this guide concentrates on EDP 05 and EDP 15, which are the two versions you will meet in practice.

Who qualifies on AFPS 05 vs AFPS 15

Both versions of the EDP set a service test and an age test, and you have to clear both. On AFPS 05 you typically need at least 18 years' qualifying service and to be at least age 40 when you leave. On AFPS 15 the bar is broadly 20 years' service and again at least age 40, which the scheme often describes as the twenty forty point. The exact wording of each scheme matters, but the headline shape is the same: a long career, and you are at least forty. How much an army pension is worth after 20 years shows where that mark leaves you under each scheme.

These two tests sit alongside each other, so meeting only one of them is not enough. You can be well past forty but short on years, or you can have served a long time but still be under forty, and in either case you would not yet meet the EDP test. Service that counts is your qualifying Regular service, and there are detailed rules about how breaks, rejoining and aggregated service are treated, which is why your own record is the thing that decides it rather than a rough mental tally.

Because AFPS 05 and AFPS 15 set the threshold differently, a member's eligibility can depend on which scheme their service falls under, and many people now have service in both, which is why EDP 05 vs EDP 15 compares the two versions side by side. If you are close to either threshold it is well worth getting your exact qualifying service confirmed before you make any decision about your leaving date, because being a few months short can change the outcome completely.

What it pays: the tax-free lump sum and monthly income

The EDP has two parts. The first is a tax-free lump sum paid once, when you leave. On AFPS 15 that lump sum is 2.25 times your preserved pension, so the size of your lump sum follows directly from the size of the pension you have built. The bigger the preserved pension, the bigger the lump sum. It is paid as a single capital amount, which is why so many leavers use it to clear a mortgage, fund retraining or simply give themselves a financial cushion while they settle into civilian work. On AFPS 15 you can also give up part or all of that lump sum through inverse commutation to lift the monthly income instead.

The second part is a monthly income. This is calculated as a percentage of your preserved pension, and on AFPS 15 that percentage starts from a base figure and steps up the longer you served beyond the qualifying point. In other words, more service means a slightly higher monthly income as well as a larger lump sum. The income runs from the point you leave until your scheme pension age, at which point it stops and your actual pension begins.

The income can also change shape at certain points along the way rather than staying flat for the whole period. The detail of how and when it steps up varies by scheme, so treat the monthly figure as something that can move at defined points rather than a single fixed number for the entire bridge. The principle to hold on to is simple: lump sum now, monthly income until pension age, both driven by the preserved pension you have earned.

A worked example (illustrative)

Here is an illustrative example to show how the AFPS 15 figures fit together. The numbers are made up to demonstrate the method, not a quote for any individual. Suppose a member leaves having served 25 years and has a preserved pension of 25,000 pounds a year. They are over 40 and have more than 20 years' service, so they meet the EDP 15 test.

The EDP lump sum on AFPS 15 is 2.25 times the preserved pension. So 25,000 pounds multiplied by 2.25 gives a tax-free lump sum of 56,250 pounds, paid once on leaving. That is the capital part of the award.

The monthly EDP income is a percentage of the preserved pension that rises with extra service beyond the qualifying point. With 25 years served, this member is five years past the 20 year point, which lifts the income fraction above the base rate to roughly 38 percent of the preserved pension. On a 25,000 pound preserved pension that works out at about 9,563 pounds a year, or around 797 pounds a month, paid until their pension age. At pension age the EDP income stops and the scheme pension of 25,000 pounds a year (before any later increases) comes into payment instead. Your own figures will differ with your service, your pay and your scheme, so use this only to see how the pieces connect.

How the EDP differs from your actual pension

The single most common confusion about the EDP is treating it as if it were the pension. It is not. The EDP is a separate, time-limited benefit that bridges the years between leaving and pension age. Your scheme pension is still calculated in its own right, sits waiting in the background, and comes into payment at your scheme's preserved pension age regardless of the EDP. The EDP fills the gap before that day arrives; it does not reduce or replace the pension that follows.

That distinction has a few practical consequences. The EDP income is only ever paid up to your pension age and then stops, whereas the scheme pension is paid for the rest of your life from pension age onward. The EDP income is a percentage of the preserved pension, so it is normally smaller than the full pension will eventually be. And because the two are separate, you should always look at both when you plan: the bridge income for the years before pension age, and the full pension for the years after.

The age a preserved pension is paid differs by scheme, which is part of why the bridge can be long. A preserved AFPS 75 pension is paid at 60 for service before 6 April 2006 and at 65 for service after that, a preserved AFPS 05 pension at 65, and a deferred AFPS 15 pension at your State Pension age, even though the normal pension age if you serve on is 55 in the two older schemes and 60 in AFPS 15. For an AFPS 15 leaver in their early forties, the EDP could therefore be bridging a gap of twenty years or more before the scheme pension starts, which is exactly why getting the bridge income right matters so much.

Tax treatment of the lump sum and income

The two parts of the EDP are taxed differently, and it is important not to mix them up. The EDP lump sum is paid tax-free. You receive the full capital amount without income tax taken off, which is one of the reasons it is so useful for resettlement, clearing debt or building a reserve as you move into civilian life.

The monthly EDP income is different. It is taxable as earned income, in the same way as a salary or a pension in payment, and it counts toward your total income for the tax year. If you start a civilian job and also draw EDP income, the two stack up and are taxed together, which can push you into a higher tax band than you might expect. It is worth checking your tax code and thinking about your combined income, rather than assuming the EDP income arrives untouched.

Because everyone's wider income, allowances and circumstances are different, the actual tax you pay on the EDP income depends on your full picture for the year. The general rule to remember is straightforward: lump sum tax-free, monthly income taxable. If your situation is at all complicated, that is the point at which speaking to a regulated adviser earns its keep.

The effect of re-employment

What you do after you leave can affect your EDP income. If you re-join the forces, or take certain public-sector roles, your EDP income can be paused or reduced while you are in that employment. The lump sum you have already received is not clawed back in the normal course of things, but the ongoing monthly income is the part that can be affected, because it is meant to support you during a gap that re-employment in those roles partly fills.

This catches some people out, particularly those who leave, take the EDP, and then return to a uniformed or related public-sector post without realising the income may stop or be cut for that period. The rules are there to prevent the EDP being paid in full at the same time as a return to the kind of service it was designed to bridge away from. Ordinary civilian employment outside those categories is treated differently, so it is the specific type of role that matters.

If you are thinking about re-joining or moving into a public-sector role after leaving, it is well worth checking how that would interact with your EDP before you commit, so there are no surprises in your monthly income. The exact treatment depends on the role and the rules in force, which is another reason to confirm your own position rather than rely on what a colleague tells you happened to them.

What happens if you just miss the EDP test

Not everyone who leaves early will clear the EDP thresholds, and being just short is more common than you might think. If you do not meet the service and age test, you usually do not walk away with nothing. Instead you normally keep a preserved and deferred pension: the pension you have built so far is held for you and becomes payable later, at your scheme's preserved pension age, rather than being paid as a bridge in the meantime.

The key difference is timing. With the EDP you get a lump sum and a monthly income now, plus your pension later. With a preserved pension and no EDP, there is no bridging income in the gap years; you wait until pension age and then draw the preserved pension. That is a real difference to your cash flow in the years immediately after leaving, which is exactly why the EDP thresholds are worth taking seriously when you choose a leaving date.

Those preserved pension ages again are age 60 for AFPS 75 service before 6 April 2006 and age 65 for AFPS 75 service after that, age 65 for AFPS 05, and State Pension age for AFPS 15, and pensions already in payment rise by 3.8 percent from April 2026 in line with CPI. If you are close to an EDP threshold, the difference between qualifying and just missing it can be substantial, so it is worth getting your exact service confirmed before you fix your exit date.

How to check your figures

Everything in this guide is general. Your own EDP depends on your exact qualifying service, your age at leaving, your preserved pension and which scheme your service falls under, so the only way to know your real numbers is to have them worked out against your record. Our EDP calculator gives you a quick, free estimate to show roughly what a lump sum and monthly income might look like and how the pieces fit together, which is a sensible starting point before any decision.

For a figure you can rely on, get an official forecast. That comes from Veterans UK: serving members use form 12 and those with a preserved pension use form 14. An official forecast reflects your real service history, including any breaks, transfers and McCloud remedy effects, which a public calculator cannot fully reproduce. Treat the calculator as a guide and the official forecast as the figure you plan around.

This site is independent and is not affiliated with the MOD or Veterans UK. Anything here is an estimate to help you understand how the EDP works, not regulated financial advice. For a decision as significant as when to leave and what it means for your finances, an official forecast plus, where needed, advice from a regulated adviser who knows the Armed Forces schemes is money and time well spent.

See your own numbers

Get your pension, lump sum and EDP in seconds.

Frequently asked questions

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk · GAD factors · Veterans UK · Forces Pension Society · MoneyHelper.