Royal Marines Pension Calculator

Estimate your Royal Marines pension, lump sum and EDP under the Armed Forces Pension Scheme (AFPS 75, 05 and 15).

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Royal Marines estimate is worked out

Your Royal Marines pension follows the Armed Forces Pension Scheme that applied while you served. Pick the scheme that matches when you joined, most careers touch more than one.

AFPS 75 is a final-salary scheme. Your pension is a share of representative pay for your rank, building to a maximum of 48.5% over a full career, 34 years for officers, 37 for other ranks, with an automatic tax-free lump sum of three times the annual pension.

AFPS 05 is also final-salary, building 1/70th of your final pensionable pay for each year served, up to about 57% of pay. It pays an automatic tax-free lump sum of three times your pension and can include an Early Departure Payment if you leave early with enough service.

AFPS 15 is a Career Average Revalued Earnings (CARE) scheme. It adds 1/47th of your current pensionable pay each year, revalued for inflation, rather than using a final salary. There is no automatic lump sum, so you can commute up to 25% of your pension for tax-free cash at a fixed rate of £12 per £1 of yearly pension given up.

How a Royal Marines pension builds across the three schemes

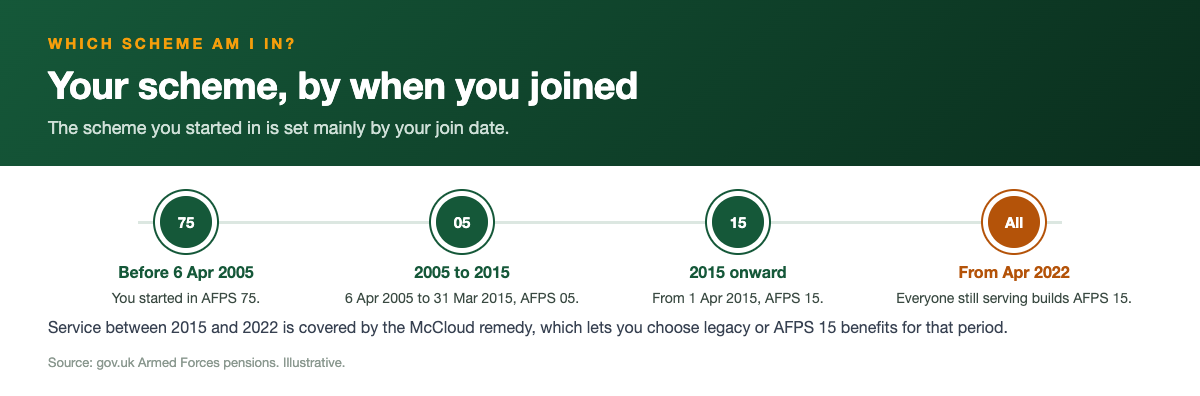

A Royal Marines pension is paid under the Armed Forces Pension Scheme, the same arrangement that covers the rest of the Naval Service and the wider forces. Which rules apply to you depends on when you served. If you joined between 1 April 1975 and 5 April 2005 you started in AFPS 75. If you joined between 6 April 2005 and 31 March 2015 you started in AFPS 05. Anyone joining from 1 April 2015 went straight into AFPS 15, and from 1 April 2022 every serving Marine builds AFPS 15 going forward, whatever scheme they started in.

AFPS 75 and AFPS 05 are both final salary schemes, so your pension is worked out from your pay at the point you leave rather than an average over your career. AFPS 15 is a Career Average Revalued Earnings, or CARE, scheme. Each year it banks a slice of that year's pensionable pay into a pot and revalues the whole pot for inflation, so the early years of your service are not left behind. The calculator on this page lets you model each scheme so you can see how the same length of Royal Marines service produces a different figure under each.

For Royal Marines as other ranks, accrual in the final salary schemes runs from age 18, the same starting point as ratings across the forces. Because the schemes reward length of service heavily, two Marines on the same rank and pay can end up with very different pensions purely because one served longer, so the reckonable years you enter matter as much as the pay figure.

AFPS 75: the older final salary scheme

AFPS 75 is the scheme most long serving Marines who joined before April 2005 will recognise. It does not use your actual salary. Instead it pays a pension based on the representative rate of pay for your final rank and your length of reckonable service, so two people leaving on the same rank with the same service normally get the same pension. The pension builds towards a maximum of 48.5 per cent of that representative pay, reached at 37 years of reckonable service for other ranks and 34 years for officers.

The calculator cannot hold the Ministry of Defence's rank by rank representative pay tables, so it uses the pay figure you enter as a stand in and tells you so on screen. That keeps the maths honest while still giving you a usable estimate. AFPS 75 also pays an automatic tax free lump sum equal to three times your annual pension, which arrives at the same time as the pension itself.

One feature that catches people out is timing. AFPS 75 has no Early Departure Payment. Its early payment route is the Immediate Pension, which an other rank can draw after 22 years' service from age 18, or an officer after 16 years from age 21. If you leave before that point you hold a deferred pension that becomes payable at age 60. The pension is broadly flat until age 55, then it is increased for inflation with all the past Consumer Prices Index rises applied at that point.

AFPS 05: 1/70th of final pay

If you joined the Royal Marines between April 2005 and March 2015 you started in AFPS 05. It is simpler to picture than AFPS 75 because it works on your own final pensionable pay rather than a representative rate. For every year of reckonable service you earn 1/70th of your final pay, and the pension can build to around 57 per cent of final pay over a full career. As with AFPS 75, there is an automatic tax free lump sum worth three times the annual pension.

The worked example below shows how quickly this adds up. The key levers are your final pensionable pay and your years of service, both of which you control on the calculator. Increasing either one raises the pension in a straight line until you reach the scheme maximum, at which point extra service no longer adds to the percentage.

AFPS 05 has a normal pension age of 55, so serving to 55 means an immediate pension. Leave before that and your pension is preserved and paid from 65. That long wait is one of the main reasons the Early Departure Payment scheme matters so much to Marines who leave in their forties, because it bridges the gap between leaving and the pension becoming payable. We cover that next.

Early Departure Payment for Marines who leave early

Plenty of Royal Marines leave well before normal pension age, and the Early Departure Payment, or EDP, is designed for exactly that. It is not the pension itself. It is a tax free lump sum plus a taxable monthly income that runs from the day you leave until your pension comes into payment, at which point the preserved pension takes over. It rewards people who have given a long service but are not yet old enough to draw the pension.

Under AFPS 05 the EDP is available if you leave at age 40 or over with at least 18 years' service. It pays a lump sum of three times your preserved pension and a monthly income of around 50 per cent of that preserved pension, which is the scheme's published headline rate and is held flat until age 55 before being uprated for inflation. Under AFPS 15 the qualifying point is broadly 20 years' service and age 40, often called the 20/40 point. The AFPS 15 EDP lump sum is 2.25 times the deferred pension, and the monthly income starts at 34 per cent of the deferred pension, with an extra 0.85 per cent of that pension added for every whole year served beyond 20.

Because most current Marines now have a mix of legacy service and AFPS 15 service, your actual EDP picture can combine elements of both. The calculator lets you model the EDP under each scheme so you can see the lump sum and the monthly income side by side. Treat these as estimates: the precise award depends on your exact service and exit age, and only Veterans UK can confirm it.

AFPS 15: the CARE scheme everyone now builds

Since 1 April 2022 every serving Royal Marine builds AFPS 15, so this is the scheme that will make up a growing share of most members' final pension. Each scheme year it banks 1/47th of that year's pensionable pay into your pot and revalues the running total for inflation, so a year you served early in your career is not frozen at its original cash value. There is no maximum number of years, and you need at least two years of qualifying service to have earned a pension at all.

Unlike the two older schemes, AFPS 15 pays no automatic lump sum. If you want tax free cash you create it by commuting, which means giving up some annual pension in exchange for a one off sum. The rate is fixed at about 12 to 1, so every 1 pound of annual pension you surrender produces about 12 pounds of lump sum, up to the HMRC limit of 25 per cent of your benefits. The reduction to your pension is permanent, so this is a genuine trade off rather than free money, and it is worth modelling carefully before you commit.

AFPS 15 has a normal pension age of 60, with the deferred pension paid at your State Pension age. You can leave earlier and hold a deferred pension, or draw it from age 55 with a permanent actuarial reduction, or qualify for the EDP if you hit the 20/40 point. The calculator shows the AFPS 15 figure so you can weigh it against your legacy entitlement.

A worked example for a Royal Marine

This example is illustrative only and uses round figures to show the method, not a quote for any real person. Imagine a Marine in AFPS 05 leaving with a final pensionable pay of 35,000 pounds and 24 years of reckonable service. The annual pension is 35,000 multiplied by 24 and divided by 70, which comes to 12,000 pounds a year. The automatic tax free lump sum is three times that pension, so 36,000 pounds.

Now suppose the same Marine leaves at age 41 rather than waiting for the preserved pension at 65. With more than 18 years' service and over age 40 they qualify for the AFPS 05 Early Departure Payment. The EDP lump sum is three times the preserved pension, so 36,000 pounds, and the EDP monthly income is around 50 per cent of the preserved pension, roughly 6,000 pounds a year or about 500 pounds a month, held flat until age 55 and then uprated for inflation. At pension age the preserved pension of 12,000 pounds a year comes into payment in its own right.

The same service modelled under AFPS 15 would build differently, banking 1/47th of pay each year into a revalued pot, with no automatic lump sum unless the member chooses to commute at the fixed rate of about 12 to 1. Swap in your own pay and years on the calculator above to see your figures, and treat any single output as an estimate of how each scheme works out rather than a guaranteed amount.

The McCloud remedy and your remediable service

The McCloud remedy is the single biggest reason a Royal Marines pension can look more complicated than the simple scheme rules suggest. The courts found that the way members were moved into AFPS 15 in 2015 unlawfully discriminated by age. The fix covers the remedy period of 1 April 2015 to 31 March 2022. If you were serving across that window you will be given a choice between your legacy benefits, AFPS 75 or AFPS 05, and AFPS 15 benefits for those years.

You do not have to decide blind. The Ministry of Defence issues a Remediable Service Statement that sets out both options so you can compare them at the point your pension becomes payable, when it is clearest which choice pays more. From 1 April 2022 onwards everyone builds AFPS 15 regardless, so the choice only ever applies to that seven year remedy period, not to your whole career.

For most Marines the practical upshot is that your final pension is a blend: legacy service up to 2015, a remedy period you can elect over, and AFPS 15 from 2022 onwards. The benefits you built in AFPS 75 or AFPS 05 before transition are protected as accrued rights and are paid when originally expected, linked to your pay and rank at the point you leave. Running the legacy and AFPS 15 figures on this calculator gives you a feel for which way your remedy choice is likely to lean, but the Remediable Service Statement is the document that decides it.

Tax, checking your figure and next steps

The tax treatment is worth getting straight. Across all three schemes the automatic or commuted lump sum is tax free within the normal limits, which is why the lump sum can look so generous. The annual pension itself is taxable as income when it comes into payment, and the EDP monthly income is also taxable, although the EDP lump sum is tax free. Pensions already in payment are protected against inflation: they rise by 3.8 per cent from April 2026 in line with the Consumer Prices Index.

This calculator is an independent educational tool. It is not affiliated with the Ministry of Defence, Veterans UK or JPAC, and it provides estimates, not regulated financial advice. The only official forecast comes from Veterans UK. If you are still serving, request a forecast using form 12. If you have left and hold a preserved pension, use form 14. Your annual benefit statement and your Remediable Service Statement are also reliable reference points to sense check the numbers here.

To get the most out of the tool, enter your honest reckonable service and your current or final pensionable pay, then compare the schemes that actually apply to your service dates. Look at the pension, the lump sum and, if you might leave before pension age, the EDP. If a major decision turns on the figure, such as commuting a large slice of your AFPS 15 pension or timing your exit around the 20/40 point, get the official forecast from Veterans UK and consider speaking to a suitably qualified independent adviser before you act.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Not sure which scheme you're in?

Find out whether you're on AFPS 75, 05 or 15 and how each builds up.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.