AFPS 75 Pension Calculator

Work out your AFPS 75 pension and automatic tax-free lump sum (three times your pension). AFPS 75 is final-salary, building up to 48.5% of your final pay.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

How this is worked out

AFPS 75 uses representative pay for your final rank, so we use the pay you enter as a proxy. Builds to a maximum of 48.5%. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the AFPS 75 estimate is worked out

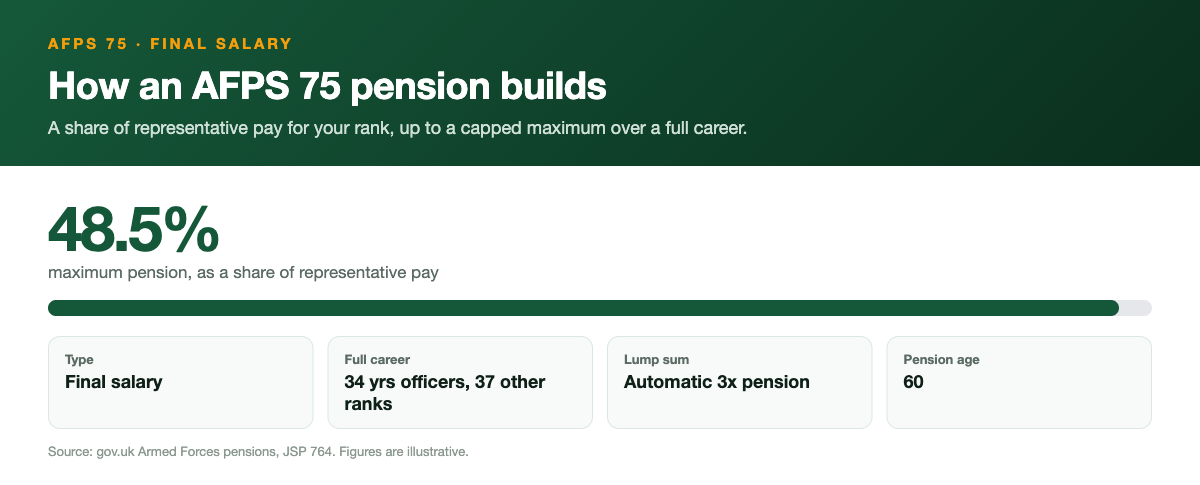

AFPS 75 is a final-salary scheme. Your pension is a share of representative pay for your rank, building to a maximum of 48.5% over a full career, 34 years for officers, 37 for other ranks, with an automatic tax-free lump sum of three times the annual pension.

How AFPS 75 builds your pension

AFPS 75 is a final salary scheme, which is the old fashioned and generous type of pension that newer schemes have moved away from. Your pension is worked out from your final pensionable rank and your length of reckonable service, not from contributions sitting in a pot. That means two people who finish at the same rank with the same number of years normally walk away with the same pension, regardless of what they were actually paid month to month.

The number that does the heavy lifting here is representative pay. For officers up to OF-6 and for all other ranks, the Ministry of Defence holds a table of representative pay rates for each rank, and your pension is calculated from that figure rather than your personal salary. Only very senior officers at OF-7 and above are pensioned on their final pensionable earnings instead. The calculator on this page does not hold the MOD rank by rank tables, so it uses the pay figure you enter as a stand in for your representative rate. Treat the result as a guide and check the real rate for your rank when you want a firm number. The army pension chart by rank and years served sets out the published amounts if you want to read your own rank straight off the table.

Accrual starts from a set age, not the day you attest. For officers the clock starts at age 21 and for other ranks, ratings and marines it starts at age 18. Service before that age still counts towards qualifying for benefits, but it does not build the final salary fraction. This is one of the most common points where a quick mental sum goes wrong, so it is worth being clear about it from the start.

The 48.5% maximum and the accrual rate

AFPS 75 caps the pension you can earn at 48.5% of your representative pay. You reach that ceiling at full reckonable service, which is 34 years for officers and 37 years for other ranks, ratings and marines. Serving beyond the cap does not push the pension higher, so the last few years before the maximum are worth knowing about when you plan your exit.

Because the maximum is fixed, the build up works out to a steady accrual each year. For an officer, 48.5% spread over 34 years is just under 1.43% of representative pay for every year served. For an other ranks member, 48.5% spread over 37 years is roughly 1.31% a year. The calculator models this as a straight line to the 48.5% ceiling, which is a clean way to estimate a part career figure even though the real scheme tables are stepped by rank and service.

One thing this maximum does not do is reward you for staying past the cap purely for pension. Once you hit 34 or 37 years you are at 48.5% and that is the most the final salary calculation will give you. If you are weighing up a final tour, the pension question is usually settled well before that point, and the decision becomes about pay, role and resettlement rather than a bigger pension.

The automatic 3x tax-free lump sum

AFPS 75 pays an automatic tax-free lump sum on top of your annual pension, and you do not have to give up any income to get it. The lump sum is three times your annual pension. So if your AFPS 75 pension works out at £10,000 a year, the automatic lump sum is £30,000, paid tax free. This is a genuine extra, built into the scheme, and it is one of the features that makes AFPS 75 stand out against later schemes.

This is very different from how AFPS 15 handles cash. Under AFPS 15 there is no automatic lump sum at all, and any tax-free cash has to be created by commuting, which means trading future pension income for a one off payment. AFPS 75 hands you the three times lump sum for free, and you can then choose whether to commute further on top through resettlement commutation if you qualify. Understanding that distinction stops people from double counting or expecting cash that the scheme does not actually provide.

Because the lump sum is a straight multiple of the pension, anything that changes your pension changes the lump sum by three times as much. A small difference in reckonable service or representative pay ripples through both numbers. That is a good reason to get your service dates and final rank right before you lean on any estimate, including the one this calculator produces.

Pension ages and the immediate pension point

AFPS 75's normal pension age is 55. If you leave before reaching an earlier payment trigger, your pension is preserved instead, and a preserved AFPS 75 pension is paid from 60 for service before 6 April 2006 and from 65 for service after that. A preserved AFPS 75 pension keeps its value over the years through inflation linking, so it is not frozen in cash terms even though you cannot draw it early.

AFPS 75 does not use the Early Departure Payment system that AFPS 05 and AFPS 15 use. Instead it has its own early payment mechanism called the Immediate Pension. Long servers get their pension and lump sum paid straight away on leaving, years before a preserved pension would be due, provided they have served long enough. For officers the Immediate Pension point is 16 years of service from age 21. For other ranks it is 22 years of service from age 18. Both points are worked through with real figures on how much is an army pension after 16 years and how much is an army pension after 22 years.

If you reach the Immediate Pension point, the pension is paid flat until age 55 and then increased each year in line with CPI inflation, with all the inflation that built up between leaving and age 55 applied in one go at 55. If you leave before reaching the Immediate Pension point, you get a preserved pension instead, payable from 60 or 65 depending on when that service was earned. Knowing which side of that line you fall on changes the whole shape of your finances in the years just after you leave.

Who is in AFPS 75

AFPS 75 covers regular members who joined between 1 April 1975 and 5 April 2005. If that is when you attested, you were enrolled automatically. The scheme closed to new entrants on 6 April 2005, when AFPS 05 took over for new joiners, so nobody has built fresh AFPS 75 service from a standing start since then.

Service does not all stay in AFPS 75 forever, though. Under the McCloud remedy, members who were affected moved into AFPS 15 from 1 April 2022, and they have a choice between their legacy benefits and AFPS 15 for the remedy period of 1 April 2015 to 31 March 2022. That choice is set out in a Remediable Service Statement. So a long serving member may have AFPS 75 service up to 2015, a remedy period to choose over, and AFPS 15 service after 2022, all sitting in the same pension picture.

If you are not sure whether AFPS 75 applies to you, your joining date is the first thing to check. Joined before 6 April 2005 and stayed regular, and AFPS 75 is almost certainly part of your record. This calculator is aimed squarely at that AFPS 75 final salary slice, so it is most useful for the part of your service that sits in the 75 scheme.

Resettlement commutation and the resettlement grant

On top of the automatic three times lump sum, AFPS 75 lets some leavers take extra tax-free cash through resettlement commutation. This means giving up a slice of your annual pension in exchange for a larger lump sum up front, to help with the move back to civilian life. It is a real trade, not free money, so the pension you keep for life is lower in return for the bigger cash sum on the day.

Whether resettlement commutation is the right call depends on what you need the money for and how long you expect to draw the pension. Clearing a mortgage or funding a business start can make the lump sum attractive, but giving up index linked income for decades is a serious decision. The amounts and the rate at which pension converts into cash are set by the scheme rules and Government Actuary factors, and this calculator does not model resettlement commutation, so treat any figure you see here as the position before that choice.

Separately, AFPS 75 pays a one off resettlement grant to members who leave with enough service but do not qualify for an Immediate Pension. Officers need at least 9 years of reckonable service from age 21 and other ranks at least 12 years from age 18, and the grant is a fixed sum rather than a percentage of pay. The resettlement grant is not modelled in this calculator either, so check the current fixed amounts with Veterans UK if it applies to you.

A worked example (illustrative)

Here is an illustrative example using only round figures, to show how the parts fit together. Take an other ranks member who leaves at the 22 year Immediate Pension point with a representative pay rate of £40,000. At roughly 1.31% a year, 22 years builds a fraction of about 28.84% of representative pay. That gives an annual pension of about £11,535, or around £961 a month before any tax on the income.

On top of that pension comes the automatic tax-free lump sum of three times the pension, which is about £34,605, paid tax free. Because this member has reached the Immediate Pension point, both the pension and the lump sum are paid straight away on leaving, not held until age 60. The pension would then stay flat until age 55 and rise with CPI from there.

Now contrast a full career officer. Take an officer who serves the full 34 years on a representative pay rate of £50,000. They reach the 48.5% maximum, giving an annual pension of £24,250 and a tax-free lump sum of £72,750. These figures are illustrative only and use the pay you would enter as a proxy for the real representative rate, so your own result will move once the correct rank rate is used.

How to check your own AFPS 75 position

The estimate on this page is a starting point, not an official forecast. The biggest reasons your real number will differ are that the MOD uses the published representative pay rate for your final rank rather than the pay you type in, and that your exact reckonable service dates may not match a rough years figure. For anything that matters financially, you want the scheme tables behind your specific rank and service.

For a proper forecast, ask Veterans UK. Serving members request a forecast using form 12, and those with a preserved pension use form 14. That forecast is the official figure and is the one to rely on for big decisions such as resettlement commutation, clearing a mortgage or planning a leaving date. This site is independent and not affiliated with the MOD, Veterans UK or JPAC, and it gives estimates rather than regulated financial advice.

Common mistakes worth avoiding are counting service before age 21 for officers or age 18 for other ranks towards the final salary fraction, forgetting that the pension is capped at 48.5%, and assuming the Immediate Pension is paid when you have not actually reached the 16 or 22 year point. If your record spans the McCloud remedy period, get your Remediable Service Statement out too, because part of your service may end up counting under AFPS 15 rather than AFPS 75. When in doubt, line your numbers up against an official forecast before you commit to anything.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Not sure which scheme you're in?

Find out whether you're on AFPS 75, 05 or 15 and how each builds up.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.