The McCloud remedy explained

The McCloud remedy puts right age discrimination that happened in 2015, when younger armed forces members were moved into AFPS 15 while older members were left in their legacy scheme. If you were serving on 31 March 2012 and still serving on or after 1 April 2015, it gives you a choice of benefits for the seven years from 1 April 2015 to 31 March 2022. This guide explains what went wrong, who is affected, how to read your Remediable Service Statement, and how to think about the legacy versus AFPS 15 decision without rushing it.

Key takeaways

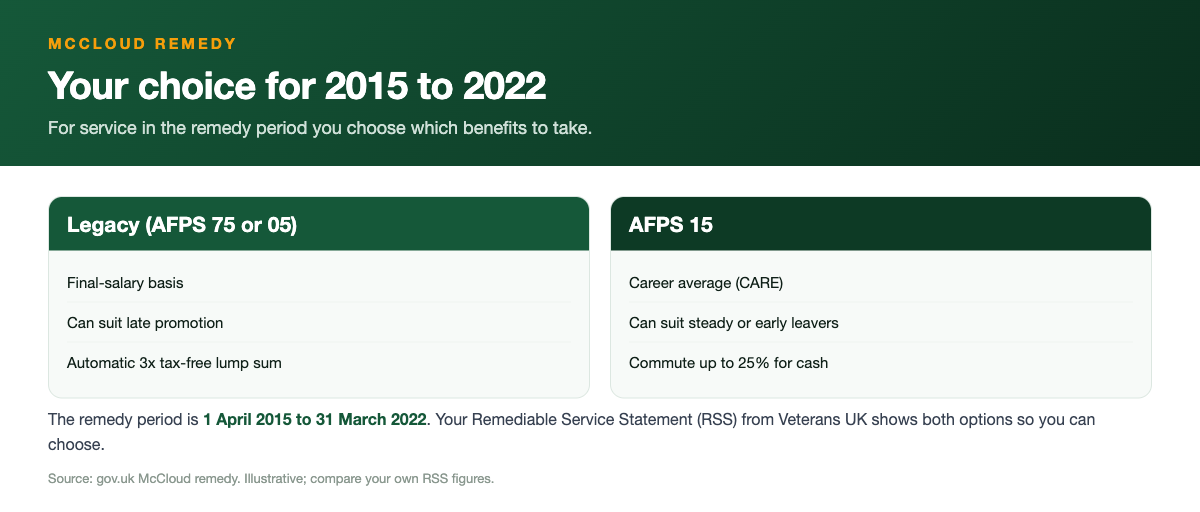

- The remedy period is 1 April 2015 to 31 March 2022, and only that seven-year slice is affected.

- You choose legacy benefits (AFPS 75 or AFPS 05) or AFPS 15 benefits for those years, informed by a Remediable Service Statement.

- Most people make a deferred choice at the point they take the pension; those already retired or near retirement get an immediate choice.

- From 1 April 2022 everyone serving builds new pension in AFPS 15, so the remedy does not touch service after that date.

- Late promotion tends to favour the final-salary legacy schemes; your leaving age and your tax position can tip it the other way.

- If the remedy creates an Annual Allowance charge, the deadline to elect Scheme Pays is 6 July 2027, now confirmed in the 2026 tax regulations.

- The binding figures come from your official RSS and Veterans UK, and for the choice and any tax question regulated advice is worth taking.

What McCloud and Sargeant were

In 2015 the government reformed public service pensions and moved most members onto new career-average schemes. For the armed forces that meant AFPS 15. To soften the change, anyone within ten years of their normal pension age was given transitional protection and allowed to stay in their old final-salary scheme, AFPS 75 or AFPS 05. Younger members got no such protection and were moved across straight away.

Two groups of public servants challenged this. The judges in the McCloud case (judges' pension scheme) and the Sargeant case (firefighters' pension scheme) found that protecting only older members was unlawful age discrimination. The ruling applied across all the reformed public service schemes, the armed forces included, which is why the fix is often just called McCloud.

The point of the remedy is simple, even if the admin behind it is not. Nobody should be worse off, or better off, purely because of how old they happened to be in 2015. So the remedy rewinds the affected years and lets each member decide, on the facts of their own career, which set of benefits they want for that period.

The remedy period: 2015 to 2022

The remedy period runs from 1 April 2015 to 31 March 2022. These are the years where the discrimination took place, because that is the window in which some members were protected in a legacy scheme and others were not. Only this seven-year slice of your service is in scope for the choice.

Service before 1 April 2015 stays exactly where it was. If you built up final-salary pension in AFPS 75 or AFPS 05 before the reforms, that is protected and paid under those rules, linked to your pay and rank when you leave, not frozen at the 2015 transition. Service from 1 April 2022 onward is in AFPS 15 for everyone serving, and the remedy does not change that.

It helps to picture your pension as three blocks. The early block is your original legacy scheme. The middle block is the remedy period, 2015 to 2022, where you get the choice. The later block is AFPS 15 from April 2022. The remedy only asks a question about the middle block.

Who is affected

You are in scope if you were in pensionable service on 31 March 2012 and were still serving on or after 1 April 2015. That captures the members who were already in a legacy scheme before the reforms and who carried on serving into the discrimination window. If you joined on or after 1 April 2015 you were always in AFPS 15, so there is no legacy choice to make.

As a rough sort, members who had transitional protection were kept in AFPS 75 or AFPS 05 until they all moved into AFPS 15 on 1 April 2022. Members without protection were moved into AFPS 15 back in 2015. The remedy rolls the unprotected group back into their legacy scheme for the remedy years on paper, so that everyone is offered the same choice on the same footing.

You can be in more than one scheme as a result. It is common for a veteran to hold AFPS 75 or AFPS 05 for early service, a remedy-period choice for 2015 to 2022, and AFPS 15 from 2022. Remember you also need at least two years of qualifying service before most benefits vest at all.

Your Remediable Service Statement (RSS) and how to read it

The Remediable Service Statement is a personal statement, issued through Veterans UK, that sets out your remedy-period benefits calculated both ways: once as legacy benefits under AFPS 75 or AFPS 05, and once as AFPS 15 benefits. It exists so you can compare like with like before you choose, rather than guessing.

When you read it, look at the headline annual pension under each option first, because that is the income you keep for life. Then look at the lump sum. The legacy schemes pay an automatic tax-free lump sum of three times the annual pension, while AFPS 15 has no automatic lump sum and instead lets you commute up to 25% of your pension for cash at a fixed rate of twelve pounds for every one pound of yearly pension you give up. Finally, note the different pension ages: AFPS 75 and AFPS 05 both have a normal pension age of 55 and AFPS 15 has one of 60, but if you left earlier a preserved AFPS 75 pension is paid at 60 for service before 6 April 2006 and at 65 for service after that, a preserved AFPS 05 pension at 65, and a deferred AFPS 15 pension at your State Pension age, with an Early Departure Payment route from age 40.

Check the figures against your own record while you have it in front of you: your reckonable service dates, your pay, and your rank history. The RSS is the binding document for your numbers. If something looks wrong, query it with Veterans UK rather than relying on an estimate from a calculator, including this one.

Immediate choice versus deferred choice

There are two ways the choice reaches you. Most serving members make a deferred choice, which means you do not decide now. You decide at the point your pension becomes payable, when you can see your final pay, your final rank, your actual leaving age, and the real numbers on your RSS. Deferring is sensible because the better option often only becomes clear once those facts are settled.

Members who are already retired, or very close to it, get an immediate choice instead, because their pension is in payment or about to be. For this group the remedy includes a process to work out which option they should have had and to correct anything already paid on the wrong basis, including putting right tax that was owed or overpaid for the remedy years.

Either way the choice is a one-off and it is irreversible once made, so it is worth treating with the same care as any other big financial decision. You do not lose the choice by waiting if you are in the deferred group; you simply make it later with better information, and immediate choice or deferred choice works through which group you fall into and what each route means.

How to weigh legacy against AFPS 15

There is no single right answer, because the schemes work in genuinely different ways. AFPS 75 and AFPS 05 are final-salary: the pension for the remedy years is tied to your pensionable pay near the end of your career. AFPS 15 is career average: it banks a slice of each year's pay, 1/47th, and revalues it for inflation as you go, so it does not depend on a high final salary, a difference set out scheme by scheme in AFPS 75 vs 05 vs 15.

The usual rule of thumb is that late promotion favours the final-salary legacy schemes. If you went up a rank or two in your last few years, a final-salary calculation lifts the value of all your remedy-period service to that higher pay, whereas the career-average pot only ever captured the lower pay you were actually earning at the time. If your pay was fairly flat across your career, that final-salary advantage shrinks and AFPS 15 can look competitive.

Two other levers matter. The first is leaving age, because the schemes pay at different points: serve to the normal pension age and that is 55 on AFPS 75 and AFPS 05 and 60 on AFPS 15, while leaving earlier means waiting for a preserved pension at 60 or 65 on AFPS 75, 65 on AFPS 05, and your State Pension age on AFPS 15, with an Early Departure Payment available from 40. The second is the shape of the cash: legacy gives an automatic three-times lump sum, while AFPS 15 makes you commute for any lump sum and only at twelve to one. Weigh the guaranteed, index-linked income you keep against the cash you would get on day one.

The tax and Annual Allowance angle

Moving your remedy-period benefits between schemes can change how much pension you are treated as having built up in those years, and that feeds into the Annual Allowance, which is the cap on tax-advantaged pension growth in a tax year. Because the remedy recalculates the 2015 to 2022 years, your Annual Allowance position for those years can move, sometimes creating a charge and sometimes removing one you already paid.

The remedy includes a formal process to put this right. Where extra tax is due for the remedy years it is collected, and where you overpaid it can be refunded or compensated. You do not report this through your normal Self Assessment return; you use HMRC's Calculate your public service pension adjustment service instead. You do not have to reverse-engineer this yourself, but you should be aware it exists, especially if you had a promotion, a pay spike, or a large amount of service in the remedy window, as those are the cases where Annual Allowance is most likely to bite.

If a charge does land, you may not have to pay it from your own savings. A mechanism called Scheme Pays lets you ask the scheme to settle the Annual Allowance charge and recover it later through a permanent reduction to your pension. Because Remediable Service Statements have been slow to reach members, the deadline for a mandatory Scheme Pays election was extended to 6 July 2027 for anyone who had not started taking their benefits by 1 October 2023, which covers most serving and deferred members. Members who were already drawing a pension on that date always had 6 July 2027, so everyone affected by the remedy now works to the same date.

Tax interacts with everything else, including how much you commute and when you take the pension, so it is one of the clearest reasons to take regulated financial advice before you choose. An adviser who knows the armed forces schemes can model the options against your wider finances, and the binding tax figures will come through your official RSS and Veterans UK.

What the 2026 tax regulations changed

In July 2026 the Public Service Pension Schemes (Rectification of Unlawful Discrimination) (Tax) Regulations 2026 were made and laid, and HMRC published a newsletter setting out what they do. The main effect is that the extended Scheme Pays deadline is now written into law rather than being an announcement that schemes had been told to work to, so you can plan around 6 July 2027 with confidence. The regulations also give members until 5 July 2032 to amend a Scheme Pays notice, which matters if your figures are corrected long after you first elected.

They also spell out what happens if you miss 6 July 2027. Your election does not simply fail: it becomes a voluntary Scheme Pays request instead, and the scheme still has to pay the charge. What you lose is the scheme's joint liability for it, which is the protection that keeps HMRC from coming to you if something goes wrong. That is a meaningful difference, so the date is still worth hitting, but missing it is not the cliff edge it is sometimes described as.

One practical point on how you elect. If you submit through HMRC's Calculate your public service pension adjustment service, HMRC passes the election to your scheme, and it counts as valid even though it did not come from you directly. Two dates then matter: the date you submitted, which decides whether it is a mandatory election or a voluntary request, and the date HMRC forwards it, which starts the clock for when the tax has to be paid. Keep your submission confirmation, because it is the date that protects you.

Two of the changes are specific to the armed forces rather than public service pensions in general. The first covers AFPS 75 members who elect for new scheme benefits for the remedy years. That election can leave the scheme paying benefits that match Early Departure Payment 15 benefits, and the regulations now treat those payments as though they came from EDP 15 so the tax treatment matches what an EDP 15 member would get.

The second covers re-joiners. If you served in AFPS 75, left, and then rejoined before the end of the remedy period as an AFPS 05 member, the re-joiner rules pull your earlier AFPS 75 service across into AFPS 05. A protected pension age is the right to draw a pension before the normal minimum pension age, which is 55, and it is specific to a scheme rather than to you personally. It is the reason armed forces benefits can be paid from around 40 in the first place. The open question was whether moving that service would cost you the protected pension age attached to it. The regulations confirm that it does not: a re-joiner who elects for new scheme benefits keeps the protected pension age for the AFPS 75 equivalent benefits paid from AFPS 05. If that describes your record, it is worth raising specifically with Veterans UK when your RSS arrives, because it changes when you can draw those benefits rather than just how much they are worth.

Common misconceptions

The first myth is that McCloud means you lost your pension or that you are owed a windfall. Neither is true. The remedy is about which scheme rules apply to seven years of service; it is a choice between two valid sets of benefits, not a payout. For many people the two options are closer than they expect.

The second is that you must act today. Unless you are in the immediate-choice group, you do not. Most members decide at retirement, and deferring is the default precisely because the right answer often depends on facts you do not have yet, such as your final rank and exact leaving date.

The third is that AFPS 15 is automatically worse because it has no automatic lump sum, or that the legacy schemes are automatically better because they are final-salary. The honest answer is that it depends on your career shape, your leaving age, and your tax position. Run the comparison on your own figures rather than on a general reputation, and do not assume what suited a colleague will suit you.

What to do now

Start by working out roughly where you sit. Confirm you were serving on 31 March 2012 and on or after 1 April 2015, so you know whether the choice applies to you at all. Then identify your three blocks: legacy service before 2015, the remedy period 2015 to 2022, and AFPS 15 from 2022. This guide and the calculators here can give you a feel for how the decision looks, and the McCloud remedy calculator compares legacy and AFPS 15 benefits for the remedy years.

When your Remediable Service Statement arrives, read it carefully and check it against your own service record, pay and rank history. Treat the RSS, not any estimate, as the source of truth for your numbers, and query anything that looks off with Veterans UK. Keep it safe alongside your annual benefit statements, and if you want a figure for your service outside the remedy years, request an official pension forecast.

Before you commit, take regulated financial advice if the figures are close or the tax position is complex, because the choice is one-off and irreversible. This is an independent education site, not affiliated with the MOD, Veterans UK or JPAC, and it provides estimates rather than regulated financial advice. The binding figures, and the final call on tax, come from your official RSS and Veterans UK.

See your own numbers

Get your pension, lump sum and EDP in seconds.

Frequently asked questions

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk · GAD factors · Veterans UK · Forces Pension Society · MoneyHelper.