Armed Forces Pension Increase Calculator

See how the annual CPI increase changes your armed forces pension. The 2026 increase is 3.8%, applied from April on pensions in payment and preserved.

Your details

Scheme, pay & service

Your estimate

Pension, lump sum & EDP

EDP 05 (rises to 75% at 55)

How this is worked out

AFPS 05 accrues 1/70th of final pensionable pay per year, capped at 40 years of reckonable service. An EDP 05 income steps up to 75% of the preserved pension from age 55. Figures use published AFPS rates. See our methodology. Estimate only, not financial advice.

How the Pension Increase estimate is worked out

Armed forces pensions are uprated each April in line with the Consumer Prices Index (CPI). The 2026 increase is 3.8%, applied to pensions in payment and to preserved pensions still waiting to be drawn.

This tool applies the latest uprating so your estimate reflects the value you would actually receive after the annual increase.

What the annual pension increase actually is

The annual pension increase, often called the Pensions Increase or PI, is the yearly uprating that keeps your armed forces pension in line with the cost of living. It applies to every armed forces pension scheme, AFPS 75, AFPS 05 and AFPS 15, and it is set by the Treasury through the Pensions Increase (Review) Order rather than by the MOD or Veterans UK. In plain terms, once your pension is in payment or has been preserved, it does not sit still. It is index-linked, so it grows each year to protect what your service is worth in real money.

The measure used is the Consumer Prices Index, the CPI. The increase that lands each April is based on the CPI figure for the September of the previous year. So the rise applied from April 2026 reflects inflation measured to September 2025, not the inflation rate on the day the money hits your account. This September-to-April lag is normal and applies to most public service pensions, not just the forces, which is why your increase can feel out of step with the headline inflation number you hear on the news.

This is one of the genuine strengths of the armed forces schemes. A pension that rose by a flat amount each year, or not at all, would quietly lose value as prices climbed. CPI uprating means a pension worth a certain amount in real terms today should still be worth broadly the same in real terms in twenty years. The calculator on this page lets you see, in pounds, what a given year's increase does to a pension figure you enter, so the abstract percentage becomes a concrete number you can plan around.

The 3.8% increase from April 2026

For April 2026 the increase is 3.8%. That figure comes from the CPI measured to September 2025 and is confirmed in the Pensions Increase (Review) Order for the year. It applies across the board to armed forces pensions that qualify for the increase, whether you are an AFPS 75 pensioner drawing your immediate pension, an AFPS 05 member with a preserved pension waiting for age 65, or an AFPS 15 member with deferred benefits.

To put 3.8% into everyday terms, every 1,000 pounds of qualifying annual pension rises by 38 pounds. A pension of 10,000 pounds a year goes up by 380 pounds to 10,380 pounds. A pension of 18,000 pounds a year rises by 684 pounds to 18,684 pounds. The percentage is the same for everyone; only the cash amount changes with the size of your pension. That is the simplest way to sense-check any figure this calculator gives you.

One detail catches people out every year. The increase is applied from the first Monday after the start of the new tax year, so the uprated rate runs for most, but not the whole, of the year in which it is announced. If you have been in payment for a full year you get the full increase. If your pension only came into payment partway through the previous year, you may receive a pro-rated slice of the increase for that first year, after which you pick up the full amount. The calculator shows the full-year effect, which is the right figure for planning once you are past your first year in payment.

How it applies to pensions in payment and preserved pensions

A pension in payment is one you are already drawing. Each April the increase is added to your gross annual pension and your monthly payments rise from that point. You do nothing to claim it; Veterans UK applies it automatically and your payslip reflects the new rate. The same applies to Early Departure Payment income once it starts to be uprated, and to survivor and dependant pensions in payment.

A preserved pension is one you have earned but are not yet drawing, typically because you left service before pension age. Crucially, a preserved armed forces pension does not lose its inflation protection while it waits. The increases are stored up and applied so that when you finally claim it, at age 60 for AFPS 75, age 65 for AFPS 05, or State Pension age for a deferred AFPS 15 pension, the amount reflects all the cumulative uprating since you left. A pension preserved ten years ago is worth considerably more in cash terms today than the figure on your discharge paperwork, purely because of these annual increases.

There is one quirk specific to the older schemes that trips people up. Under AFPS 75 and AFPS 05, an immediate or early pension is held flat until you reach age 55. At 55 the entire accumulated inflation from your date of leaving is applied in one go, and from then on the pension rises by CPI each year. So if you are drawing an AFPS 75 immediate pension at, say, 42, do not be alarmed that the figure looks static. The catch-up at 55 restores the lost value, and the calculator estimates the current-rate position rather than projecting that year-by-year path.

In-service revaluation under AFPS 15

AFPS 15 works differently while you are still serving, and it is worth understanding because it is genuinely good news for active members. AFPS 15 is a Career Average scheme, so each year you bank 1/47th of that year's pensionable pay into a pension pot. To stop those banked amounts being eroded before you retire, the pot is revalued every year. The label CARE actually stands for Career Average Revalued Earnings, and the word revalued is the important one.

While you are still serving, the revaluation tracks earnings, specifically the Average Weekly Earnings index, not CPI. Earnings have historically grown a little faster than prices, so an active member's banked pension tends to keep pace with what people are being paid now rather than just with the cost of living. This is the mechanism that lets a public calculator approximate your pot as your current pay multiplied by your years of service, divided by 47, because each past year is kept roughly in line with today's earnings.

The switch to CPI happens at the point your AFPS 15 benefits become deferred or come into payment. From that moment the earnings link ends and the standard CPI uprating, the 3.8% for 2026, takes over. So a serving member benefits from earnings revaluation; a leaver or a pensioner benefits from CPI increases. Both are forms of protection, but they are not the same index, and mixing them up is one of the most common misunderstandings about how AFPS 15 grows. The annual pay settlement drives the serving side of that, and our news post on the 2026 armed forces pay award covers the 3.6% rise and which elements of pay actually count as pensionable.

Recent increases in context

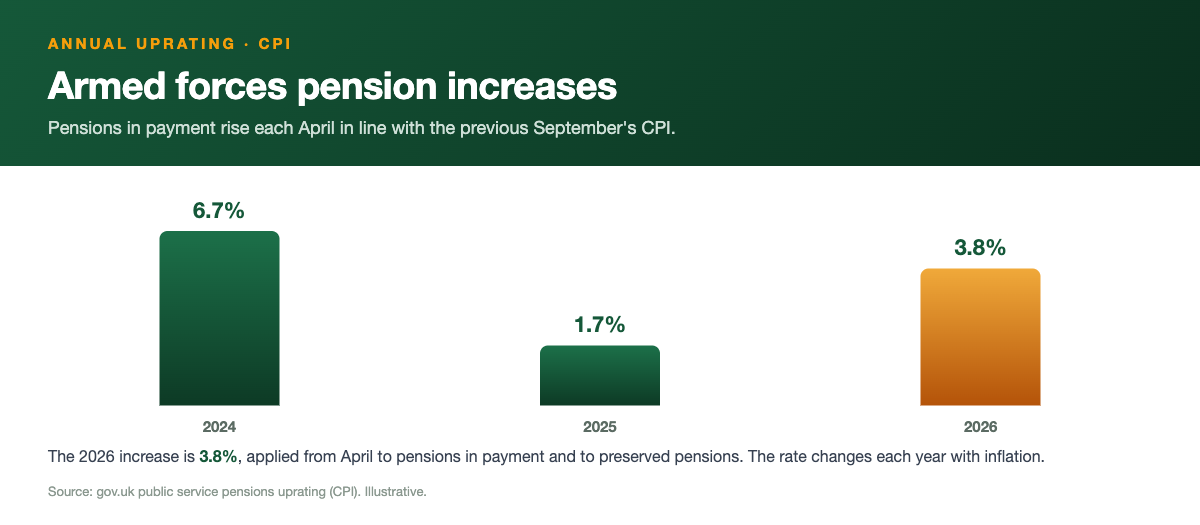

The CPI link cuts both ways, and recent years have shown its full range. When inflation spiked, the pension increase rose sharply too, because the September CPI figure that drives the uprating was high. In calmer years the increase is more modest. The 3.8% for April 2026 sits in the middle of that picture: well above the very low increases of the late 2010s, but below the unusually large rises seen when inflation peaked. The two years either side make the point: the 2024 armed forces pension increase was 6.7%, and the 2025 armed forces pension increase fell back to 1.7%.

The lesson for planning is not to assume any single year is typical. A run of high-inflation years lifts a pension faster, which is welcome, but it tells you nothing about what next year's figure will be, because that depends entirely on the CPI reading the following September. This is why this calculator deliberately applies one confirmed year's rate rather than projecting a compounded forecast across decades. Stacking guessed future increases on top of each other produces impressive but unreliable numbers, and on a YMYL subject like your pension that is the wrong kind of confidence.

What does compound, reliably, is the protection itself. Year after year of CPI uprating, even at modest rates, adds up over a long retirement. A pension drawn at 60 and held into your eighties will have been uprated more than twenty times. That cumulative effect is the real reason an index-linked armed forces pension is worth so much more than a fixed annuity of the same starting amount, and it is worth keeping in mind whenever you compare your forces pension against a private alternative.

Worked example (illustrative)

Here is an illustrative example using only the 2026 rate. Treat it as a guide to the arithmetic, not a forecast of your own pension. Suppose a veteran is drawing an armed forces pension in payment of 14,000 pounds a year and has held it for a full year. The April 2026 increase of 3.8% applies. The rise is 14,000 multiplied by 0.038, which is 532 pounds. The new annual pension is 14,532 pounds, or about 1,211 pounds a month gross before tax, up from 1,167 pounds.

Now take a preserved pension as a second illustration. Imagine a leaver has a preserved AFPS 05 pension that, after the increases applied since they left, currently stands at 6,000 pounds a year, waiting to be paid at age 65. The 2026 increase adds 6,000 multiplied by 0.038, which is 228 pounds, lifting the preserved figure to 6,228 pounds before it is even claimed. This shows why the number on your old discharge paperwork understates what you will eventually receive. The pension has kept working in the background.

Both figures are illustrative and use only the confirmed 3.8% rate. Your real pension depends on your scheme, your rank and pensionable pay, your length of service, your age, and any commutation or EDP choices you have made. The calculator on this page does the same sums instantly for whatever starting pension you enter, but for a binding figure you should always rely on an official forecast rather than any estimate, including this one.

How to check your own position

The single most reliable way to confirm your numbers is an official forecast from Veterans UK. Serving members request a forecast using form 12, and those with a preserved pension use form 14. These come from the team that actually administers your pension, hold your real service record, and will reflect your correct scheme, pay and any McCloud remedy choice. This site is independent and gives estimates; it is not affiliated with the MOD, Veterans UK or JPAC, and nothing here is regulated financial advice.

If you are already drawing your pension, check your April payslip or annual statement. The gross annual figure should have risen by the year's increase, 3.8% for 2026, assuming you have been in payment for a full year. If it has not moved and you are under 55 on an AFPS 75 or AFPS 05 pension, that is expected behaviour because of the flat-rate period to 55, not an error. If you are over 55, in payment for a full year and the figure has not changed, that is worth querying with Veterans UK.

For McCloud-affected members, your Remediable Service Statement is the document that shows how your benefits for the remedy period, 1 April 2015 to 31 March 2022, are treated under your legacy scheme versus AFPS 15. Increases apply to whichever set of benefits you ultimately receive, so make sure you are reading the increase against the right figures. If your statement and your expectations do not line up, raise it before making any irreversible choice.

Tax treatment and next steps

The annual increase is added to your gross pension, and your pension is taxable income in the normal way. So when your pension rises by 3.8%, the gross figure goes up by the full amount, but the cash that reaches your bank account rises by a little less once income tax is taken into account, because the increase sits on top of your other taxable income. Any tax-free lump sum you have already received is separate and is not affected by the annual increase; the uprating applies to the ongoing pension income, not to a one-off lump sum already paid.

A practical point on tax bands. Because the increase lifts your gross pension every year, over a long retirement your total taxable income can drift upwards relative to frozen or slowly rising tax thresholds. That is not a reason to want a smaller increase, far from it, but it is worth being aware that a bigger gross pension and your tax position move together. If your pension plus any other income is near a tax threshold, the annual increase is one of the things that can nudge you across it.

As next steps, use the calculator above to see the cash effect of the 3.8% increase on your own starting pension, then sanity-check it against the per-thousand rule of thumb, 38 pounds for every 1,000 pounds of pension. After that, treat any estimate here as a starting point and request the official forecast from Veterans UK using form 12 or form 14. If you are weighing up commutation, EDP timing or a McCloud choice, the increase is only one part of the picture, and our other calculators and guides cover those pieces so you can see how they fit together before you commit.

Frequently asked questions

Estimate only. These figures use published AFPS rates and the 2026 increase (3.8% CPI) to give a guide, not a formal forecast. See how we calculate for the exact method and assumptions.

Not sure which scheme you're in?

Find out whether you're on AFPS 75, 05 or 15 and how each builds up.

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk Armed Forces pensions · GAD factors · Veterans UK · MoneyHelper.