Is it worth commuting your pension?

Commuting gives you a bigger tax-free lump sum now in exchange for less guaranteed income for the rest of your life. Whether that is a good deal comes down to three things: the commutation factor on offer, what you actually plan to do with the cash, and how long you expect to draw your pension. This guide is about the judgement call, the is it worth it question, rather than the mechanics. If you want the nuts and bolts of how the sums are worked out, the commutation guide covers that in detail; here we focus on the trade-off so you can decide with your eyes open.

Key takeaways

- You are swapping guaranteed, index-linked income for life for a one-off tax-free lump sum now, and the choice is irreversible.

- The higher the commutation factor (lump sum per £1 of pension given up), the better the deal; above roughly 20:1 is generally good value.

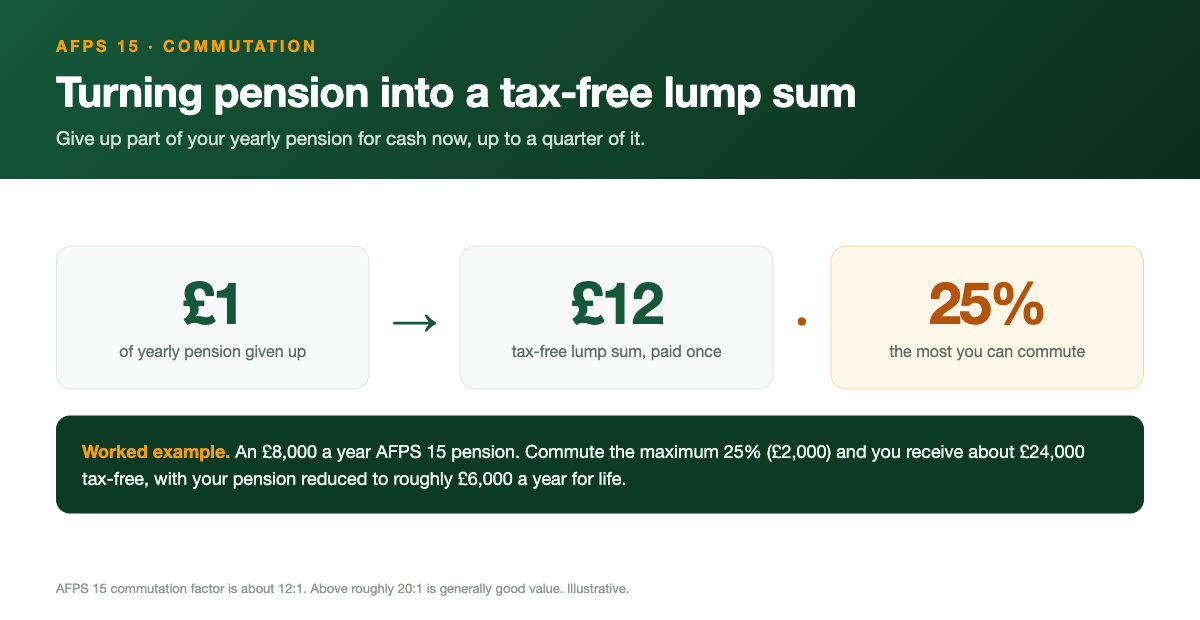

- The AFPS 15 factor is fixed at about 12:1, which is on the less generous side, so on that scheme commute only what you genuinely need.

- Commuting can make real sense to clear a mortgage or expensive debt, fund resettlement or a business, or where life expectancy is shorter.

- If you do not need the cash and expect a long retirement, keeping the income is usually the stronger choice, because the lost income can total far more than the lump sum.

- This is a one-way door on a YMYL decision, so an official forecast from Veterans UK and regulated advice are both worth having before you commit.

The core trade-off: income for life versus cash now

Strip everything else away and commutation is one swap. You give up a slice of guaranteed annual pension, paid for the rest of your life, and in return you take a fixed tax-free lump sum today. The income you surrender is not just any income. It is backed by the scheme, it does not run out however long you live, and it rises broadly with inflation every year. As a marker of how much that matters, pensions in payment go up by 3.8% from April 2026 in line with CPI. A pound of that pension is worth more next year, and more again the year after.

The lump sum, by contrast, is a known quantity that does not grow on its own. Once it is in your account it is yours to spend, invest or save, but it will not climb with prices unless you do something with it, and any growth then carries the usual investment risk. So the real comparison is not cash against cash. It is a fixed sum today against a rising stream of guaranteed payments you would otherwise have collected for decades.

Because that income would have grown year on year, the longer you live the more you give up by commuting. Over a long retirement the total income surrendered can add up to far more than the lump sum you received, which is exactly why commuting is never an automatic win. The lump sum is real money in your hand, and that has genuine value, but you are paying for it with something that quietly compounds in the background for the rest of your life.

The one feature that should be front of mind throughout is that this is irreversible. You cannot change your mind in five years if your circumstances shift or if you simply wish you had kept the income. That is what raises the stakes and what makes it worth slowing down before you sign.

A worked example: what you give up versus what you get

Here is an illustrative example to show how the decision works. The figures are round numbers chosen to make the maths clear, not a quote for your pension. Picture a member on AFPS 15 with a yearly pension of about £20,000. AFPS 15 lets you commute up to 25% of the pension at a fixed factor of about 12:1. Commute the full 25% and you give up around £5,000 a year of pension. At 12:1 that buys a tax-free lump sum of about £60,000 (£5,000 multiplied by 12).

Now look at the other side of the swap. That £5,000 a year does not stop. If you draw your pension for, say, 30 years, the bare income given up is around £150,000 before you count a single inflation rise (£5,000 multiplied by 30). And it would have risen each year, so the true figure you forgo is higher still. Against that, the lump sum was £60,000. In plain terms you handed back roughly two and a half times the lump sum in lost basic income alone over a long retirement, and more once the yearly increases are added.

That does not make commuting wrong. The £60,000 might clear a mortgage and remove a monthly payment, or fund a business that earns its keep, and £60,000 in hand at the point of leaving can be worth more to you than a larger sum dribbled out over thirty years. The example is not there to scare you off. It is there to show that a big lump sum and a poor long-term deal can be the same transaction, and that you only see the full cost when you lay the surrendered income out across the years.

Treat this example as illustrative only, and put your own pension into the commutation calculator to see the trade-off on your figures. Your pension, the exact factor that applies to you, and your likely number of years in payment will all differ, which is why an official forecast and your own figures matter so much more than any round number on a page.

When commuting can make sense

There are sound reasons to take the cash, and they usually share a common thread: the lump sum does a specific job that is worth more to you than the income you give up. Clearing a mortgage is the classic case. Wiping out the remaining balance removes a monthly outgoing, takes a worry off the table, and can change how the rest of your retirement budget feels. Clearing expensive debt, the sort charging high interest, works on the same logic, because the interest you stop paying can outweigh the pension you surrender.

Resettlement is another genuine driver. Leaving the forces often comes with real one-off costs: retraining, kit and qualifications for a new trade, setting up a home, or getting a business off the ground. If a lump sum lets you start your civilian life on the front foot rather than borrowing to do it, that has a value the bare maths does not always capture. The same goes for a clear, specific capital need, a deposit, an adaptation to a home, a known bill on the horizon, where the cash solves something concrete.

Health and life expectancy belong in this column too, handled honestly. The whole value of a pension for life depends on living to collect it. If your own health or family history points to a shorter than average retirement, the long stream of income that makes commuting look expensive may not run as long in practice, and that can tilt the maths toward taking cash now while you can use it. This is a personal and sometimes difficult judgement, but it is a legitimate part of the decision rather than something to brush aside.

When commuting usually does not make sense

The simplest case against commuting is also the most common: you do not actually need the cash. If there is no mortgage to clear, no expensive debt, no business to fund and no specific capital need, then commuting trades a secure rising income for a lump sum that sits in the bank doing less for you than the pension would have done. Taking cash just because it is offered, or because a large number is tempting, is the weakest reason of all.

A long expected retirement points the same way. The younger and healthier you are when you start drawing your pension, the more years of income you stand to give up, and the more those annual inflation rises stack up over time. For someone with a long horizon, the guaranteed, index-linked income is doing exactly what a pension is meant to do, paying you reliably for as long as you live, and giving up a chunk of it for a fixed sum is rarely the stronger play.

It is also worth being honest about what the lump sum tends to do once it lands. Cash in hand is easy to spend, and a sum that was meant to clear a mortgage can quietly drift into a car, a holiday and general life. The pension, by contrast, keeps paying whatever happens. If you are not confident the lump sum will go on something that genuinely justifies losing the income, that uncertainty is itself a reason to lean toward keeping the pension.

None of this means a lump sum is bad. It means that with no specific job for the money and a long life ahead, the default position is to keep the guaranteed income, and the burden of proof sits with commuting to show it earns its place. On AFPS 75 and AFPS 05, where the lump sum is automatic, inverse commutation runs the trade the other way and buys extra income with cash you do not need.

How the commutation factor changes the answer

The commutation factor is the exchange rate of the whole decision, and it can flip a poor deal into a reasonable one. The factor is simply how much lump sum you receive for each £1 of yearly pension you give up. A higher factor means more cash for the same income surrendered, so the rule of thumb is straightforward: the higher the factor, the better the deal for you. As a rough guide, a factor above about 20:1 is generally considered good value, because you are getting a healthy amount of capital for each pound of pension.

This is where the scheme you are in matters. AFPS 15 uses a fixed factor of about 12:1, which sits well below that good-value marker, so on AFPS 15 you are getting comparatively little lump sum for each pound of income you give up. That does not rule commuting out, but it does mean the bar is higher: you want a clear, worthwhile use for the cash before you accept a less generous rate, and it is a strong argument for commuting only what you genuinely need rather than the full 25% by default.

The legacy schemes work differently. AFPS 75 and AFPS 05 already pay an automatic tax-free lump sum of three times the pension, with resettlement commutation available on top for more, as the armed forces pension lump sum guide explains. Those resettlement and other one-off commutation options use age-banded factors published by the Government Actuary's Department, which vary with your exact age, so there is no single number to quote. The principle holds across all of them: ask what factor actually applies to you, compare it against the rough 20:1 marker, and let a weak factor make you cautious and a strong one make you more comfortable.

The break-even idea in plain terms

There is a simple way to sense-check any commutation offer without heavy maths: think about break-even. The lump sum is paid up front, but the income you gave up to get it keeps disappearing year after year. At some point the income you have forgone adds up to the same as the lump sum you took. That moment is the break-even point. Live beyond it and, in pure income terms, you have given up more than you received. Fall short of it and the lump sum came out ahead.

You can get a rough feel for it by dividing the lump sum by the yearly pension you give up. In the illustrative example above, a £60,000 lump sum against £5,000 of pension surrendered breaks even at around twelve years of income, before any inflation rises are counted. Add the yearly increases and the income catches up sooner than that, so the true break-even is a little earlier. The point is not the precise figure; it is that for anyone expecting a normal length retirement, that crossover usually arrives well within their lifetime.

Used sensibly, break-even keeps you grounded. If the crossover point is far longer than you can realistically expect to live, the cash may well be the better call. If it is comfortably inside a normal retirement, you are likely giving up more income than the lump sum is worth, and you should be clear about why the cash is still worth it to you. It is a back-of-the-envelope check, not a precise valuation, but it cuts through the appeal of the headline number and shows the deal for what it is.

The pull of a big number versus the maths

A large tax-free lump sum is genuinely exciting, and it is easy to see why. It arrives all at once, it is tangible, and at the point of leaving the forces it can feel like the reward for a long career. A rising income, paid quietly into your account every month for decades, simply does not light up the same way, even when it is worth far more over time. That gap between how the two options feel and what they are actually worth is where people most often trip up.

The honest way through it is to separate the two questions. First, what is the better financial deal, judged on the factor, your likely years in payment and a rough break-even? Second, and separately, is there a specific reason the cash is worth taking even if it is not the better deal on paper, such as clearing a mortgage or a health picture that shortens the horizon? Keeping those questions apart stops a tempting number from doing the deciding for you, and it stops a good emotional reason from being dismissed just because the spreadsheet frowns.

Be wary, in particular, of commuting the maximum simply because it is available, or of letting the size of the lump sum talk you out of running the numbers at all. The lump sum is real and it matters, but on an irreversible choice it deserves a cool head rather than a warm feeling. If the cash has a clear job to do, take it for that reason. If it does not, the excitement on its own is not a plan.

A sensible decision process

Work through it in order rather than reaching for a figure straight away. Start by getting your real numbers: request an official forecast from Veterans UK so you know your actual pension and what an official commutation lump sum would be, and find out the exact factor that applies to you, which the published commutation factors tables set out by age. Round examples are useful for understanding the broad decision, but you should never commit on the back of one.

Next, give the cash a job. Write down exactly what the lump sum would be for, and be specific: a named debt, a mortgage balance, a resettlement cost, a business plan. If you cannot name the job, that is a strong signal to keep the income. Then weigh the factor and the break-even against your honest view of your likely retirement length and your health, so you can see both the deal and the timeline in the same picture.

Then take advice. This is an irreversible decision about long-term income, and a regulated financial adviser, ideally one who knows the armed forces schemes, can model commutation against your wider finances, your tax position, your partner's situation and your plans. Independent regulated advice is genuinely worth taking here, and this site cannot replace it: the calculator and these guides give estimates to help you think, not regulated advice and not an official forecast.

A final word on this site. We are an independent resource and not affiliated with the MOD or Veterans UK, and the figures here are estimates to help you understand the trade-off, not a substitute for your forecast or for advice. Use the commutation guide and calculator to get a feel for the numbers, then let your official forecast and a regulated adviser carry you over the line.

See your own numbers

Get your pension, lump sum and EDP in seconds.

Frequently asked questions

James Hartley

James Hartley spent 22 years in the British Army, including unit personnel administration and pensions and records duties, and now writes the scheme guides and scenario pages on this site. He is not a regulated financial adviser, so the content is general information rather than personal advice.

Sources: gov.uk · GAD factors · Veterans UK · Forces Pension Society · MoneyHelper.