What the Early Departure Payment actually is

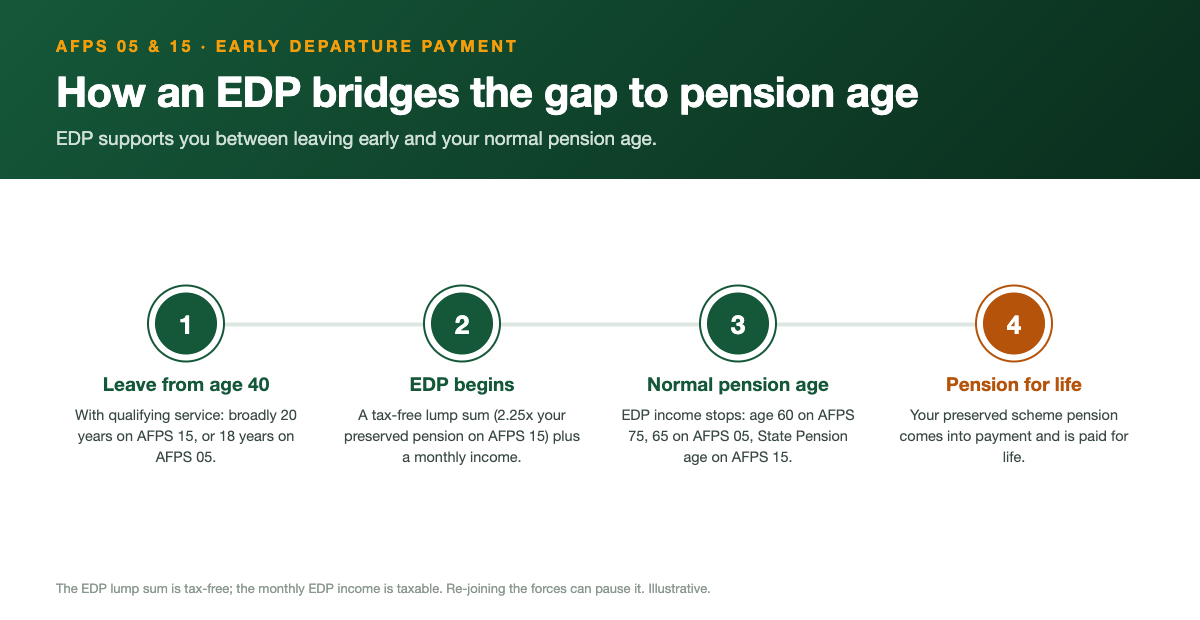

The Early Departure Payment, almost everyone just calls it the EDP, is the bridge that carries you from the day you walk out the gate to the day your pension is due to start. It is not your pension. It is a separate benefit that sits on top of it, paid only to people who leave Regular Service early but who have put in enough years to have earned it. The whole point of it is to soften the gap between leaving and reaching pension age, because for most people that gap is a long stretch of years with no scheme income at all.

An EDP award comes in two parts. There is a tax-free lump sum paid as a single payment when you leave, and there is a monthly income that runs from your leaving date until your preserved or deferred pension comes into payment. When that pension finally starts, the EDP monthly income stops, because its job is done. Your preserved pension and its own lump sum are untouched and waiting for you, calculated separately from anything the EDP pays out.

There are two flavours: EDP 05 for people in the 2005 scheme, and EDP 15 for the 2015 scheme. They share the same basic idea but the eligibility rules and the maths differ, so it pays to know which one applies to you before you read a single figure. One important point up front: the 1975 scheme, AFPS 75, has no EDP at all. Its early route is the Immediate Pension, which is a different animal, so if you are an AFPS 75 member this calculator will not show you an EDP line.

Who qualifies, and the points you have to reach

EDP eligibility is built around two thresholds you have to clear at the same time: a minimum age and a minimum length of Regular Service. Miss either one and there is no EDP, even if you are close. On EDP 05 you need to be at least age 40 when you leave and to have served at least 18 years. On EDP 15 the bar is a little higher: at least age 40 and at least 20 years of continuous or aggregated Regular service, the combination people call the 20/40 point.

Both schemes also have an upper limit. You have to be leaving before your normal pension age for the EDP to make sense, because the EDP exists to bridge to that age. For EDP 05 that means leaving before 65. For EDP 15 it means leaving before 60. If you serve all the way to pension age you do not get an EDP, you get your full pension straight away, which is the better outcome anyway.

The age and service tests are hard lines, not sliding scales. Being 39 and 11 months with 21 years in does not earn you an EDP, and neither does being 42 with 17 years on AFPS 05. The calculator applies these thresholds exactly as the engine does, so if you enter a leaving age or a length of service below the limit, the EDP rows will simply not appear. That is the calculator telling you that, on the figures entered, you have not yet reached the qualifying point.

The tax-free lump sum

The headline figure most people latch onto is the EDP lump sum, and for good reason: it is a single tax-free payment that lands when you leave. On EDP 15 the lump sum is 2.25 times your deferred annual pension. On EDP 05 it is larger as a multiple, at 3 times your preserved annual pension, which reflects the different design of the older scheme. In both cases it is based on the pension you have actually built up, so the bigger your preserved or deferred pension, the bigger the lump sum.

Because the lump sum is a multiple of your pension, a small change in your final or pensionable pay, or an extra year or two of service, ripples straight through to the cash you receive. That is worth keeping in mind if you are weighing up a leaving date. An extra year of accrual raises the pension figure, and the EDP lump sum is then 2.25 or 3 times that slightly larger number.

On EDP 15 there is a further option that is easy to miss. You can give up your EDP lump sum entirely to buy a higher monthly EDP income instead, a move known as inverse commutation. It is the mirror image of normal pension commutation: rather than swapping income for cash, you swap cash for income. Whether that suits you depends entirely on your circumstances, your other savings and how long the bridge to pension age is, so treat it as a decision to think hard about, not a default.

The monthly income and how it bridges to pension age

The second part of the EDP is a monthly income that runs from your leaving date until your pension comes into payment. On EDP 15 the income is 34% of your deferred pension at the 20/40 point, plus an extra 0.85% of that deferred pension for every whole year you served beyond 20. So someone who served exactly 20 years gets 34%, while someone who served 25 years gets 34% plus five lots of 0.85%, which is 38.25%. On EDP 05 the commonly published headline rate is around 50% of the preserved pension, used here as an estimate.

The income is paid flat at first. On EDP 15 it stays level until you reach age 55, and at 55 it is uplifted to catch up with the inflation that has built up since you left, then it rises with the Consumer Prices Index from there. EDP 05 follows a similar pattern, with CPI uprating from age 55. This is why two people with identical service can see different lifetime totals depending on how young they were when they left, because the flat early years and the catch-up at 55 interact with how long the bridge lasts.

The key thing to hold on to is that the EDP income is temporary by design. It is not a second pension for life. It stops the moment your preserved or deferred pension begins, which on AFPS 05 is age 65 and on AFPS 15 is your State Pension age for a deferred pension. From that point your scheme pension takes over and the EDP has done exactly what it was built to do.

How the EDP is taxed

The tax treatment of the two parts is different, and getting it straight saves nasty surprises. The EDP lump sum is tax-free, on both EDP 05 and EDP 15. It is paid gross and you keep all of it. That is one of the genuinely attractive features of the benefit and a big part of why the lump sum draws the eye.

The monthly EDP income is taxable. It is treated as income and taxed under PAYE in the normal way, which means it sits on top of any other taxable income you have, including pay from a new civilian job. If you leave the forces and walk straight into well-paid employment, your EDP income can push part of your total earnings into a higher tax band than you might expect. It is the combined figure that matters for your tax, not the EDP income in isolation.

Because of that interaction, the headline monthly EDP figure on any calculator, including this one, is a gross figure before tax. What actually reaches your bank account depends on your full tax position for the year. If your income is at all complicated, it is worth modelling the after-tax position properly rather than assuming the gross figure is what you will spend.

What happens if you are re-employed

A common worry is whether taking civilian work, or rejoining the forces, affects the EDP. For ordinary civilian employment outside the Ministry of Defence, the EDP income carries on as normal. You can leave, draw your EDP income and lump sum, and start a new career, and the scheme does not claw the EDP back simply because you are earning elsewhere. The only practical effect of new earnings is on your tax, as covered above, because the EDP income is taxable and stacks on top of your salary.

Where it gets more involved is if you return to a role linked to the Armed Forces pension arrangements, for example rejoining Regular Service. In that situation the picture can change, because you cannot generally be both an active accruing member and drawing an EDP for the same service at the same time. The rules here are detailed and depend on exactly what you rejoin and when, so this is a point to check with Veterans UK before you make a move rather than assume.

The honest answer is that re-employment effects are one of the areas where individual circumstances matter most. This calculator estimates the EDP for a clean early departure. It cannot model a return to service, a rejoin, or an abatement of benefits, so if any of that is on the cards, treat the figures here as the starting point and get your specific situation confirmed officially.

A worked example

Here is an illustrative example using only round figures to show the mechanics. It is not a forecast for any real person. Take someone on AFPS 15 who leaves at age 45 with 25 years of Regular service and a deferred pension worked out at 25,000 pounds a year. They have cleared the 20/40 point, so they qualify for EDP 15.

Start with the income. The base rate is 34%, and they served five years beyond 20, so they add five lots of 0.85%, which is 4.25%. That gives an income fraction of 38.25%. Applied to a 25,000 pound deferred pension, the annual EDP income is about 9,563 pounds, which is roughly 797 pounds a month before tax. That income is paid flat until age 55, then uplifted for inflation.

Now the lump sum. On EDP 15 it is 2.25 times the deferred pension, so 2.25 times 25,000 pounds gives a tax-free lump sum of 56,250 pounds, paid as a single payment on leaving. The deferred pension of 25,000 pounds itself is untouched by all of this and comes into payment later at State Pension age, with its own treatment. Change the service to exactly 20 years and the income fraction drops to the bare 34%, which shows how every year beyond 20 lifts the monthly figure.

How to check your own position and common mistakes

To use the calculator well, you need three things to hand: your scheme, AFPS 05 or AFPS 15, the length of Regular service you will have on your leaving date, and your age on that date. For AFPS 05 you also enter your final pensionable pay, and for AFPS 15 your current pensionable pay, because the engine uses that to estimate the pension the EDP is built on. Get those inputs honest and the estimate will be in the right ballpark.

The most common mistakes are worth flagging. People often confuse the two schemes and apply the 18-year EDP 05 test to AFPS 15, which actually needs 20 years. People forget that the EDP income is taxable while the lump sum is not. And people assume the EDP income lasts for life, when it stops the moment the pension starts. Another frequent slip is mixing up the deferred pension with the EDP itself; they are separate, and the deferred pension is still there waiting at pension age.

Finally, remember what this tool is and is not. This is an independent education site, not the Ministry of Defence, Veterans UK or JPAC, and the figures here are estimates to help you plan, not regulated financial advice. The only official forecast comes from Veterans UK, using form 12 if you are still serving or form 14 if your pension is already preserved. If you are making a real decision about a leaving date, run the numbers here to get your bearings, then ask Veterans UK for the official figures before you commit.